Starting a small business in Canada? Securing a small business loan is often one of the first steps to getting your business off the ground. Whether you’re opening a shop in Calgary or launching a startup in Vancouver, there are several loan options available to entrepreneurs, including government-backed loans like the Canada Small Business Financing Program (CSBFP), private lending, and alternative financing solutions. Each option offers different benefits and qualifications, so it’s important to understand which is right for your business needs. This article will guide you through the various small business loan options available in Canada and provide clear steps on how to apply for the funding you need.

Key Takeaways

- Loan Options: Small business loans in Canada include government-backed options, private lending, and alternative financing.

- Eligibility: Requirements vary by loan type; government-backed loans are typically easier to qualify for, but private lending might be faster.

- Application Process: Each type of loan has a different application process, and understanding the paperwork and approval times is key.

- Financial Planning: Consider future cash flow and business needs before applying to ensure you choose the best loan option for your situation.

Business Loan Options

When seeking traditional financing for your small business, you’ll need to decide between secured and unsecured loans. Secured loans require collateral—such as equipment or property—which the lender can claim if you’re unable to repay. Because these loans are less risky for lenders, they typically come with lower interest rates. Unsecured loans, on the other hand, don’t require collateral, making them a good option if you don’t have assets to pledge. However, they often come with higher interest rates due to the added risk for lenders.

In Canada, you have several loan options, depending on what works best for your business. Whether you’re working with a bank, an alternative lender, or considering a government-backed loan, each option has its own benefits. If you need quick access to cash without offering collateral, you might explore unsecured options like a business line of credit or business credit cards. If you have collateral to secure the loan and want lower interest rates, secured loans like term loans or equipment financing might be more suitable.

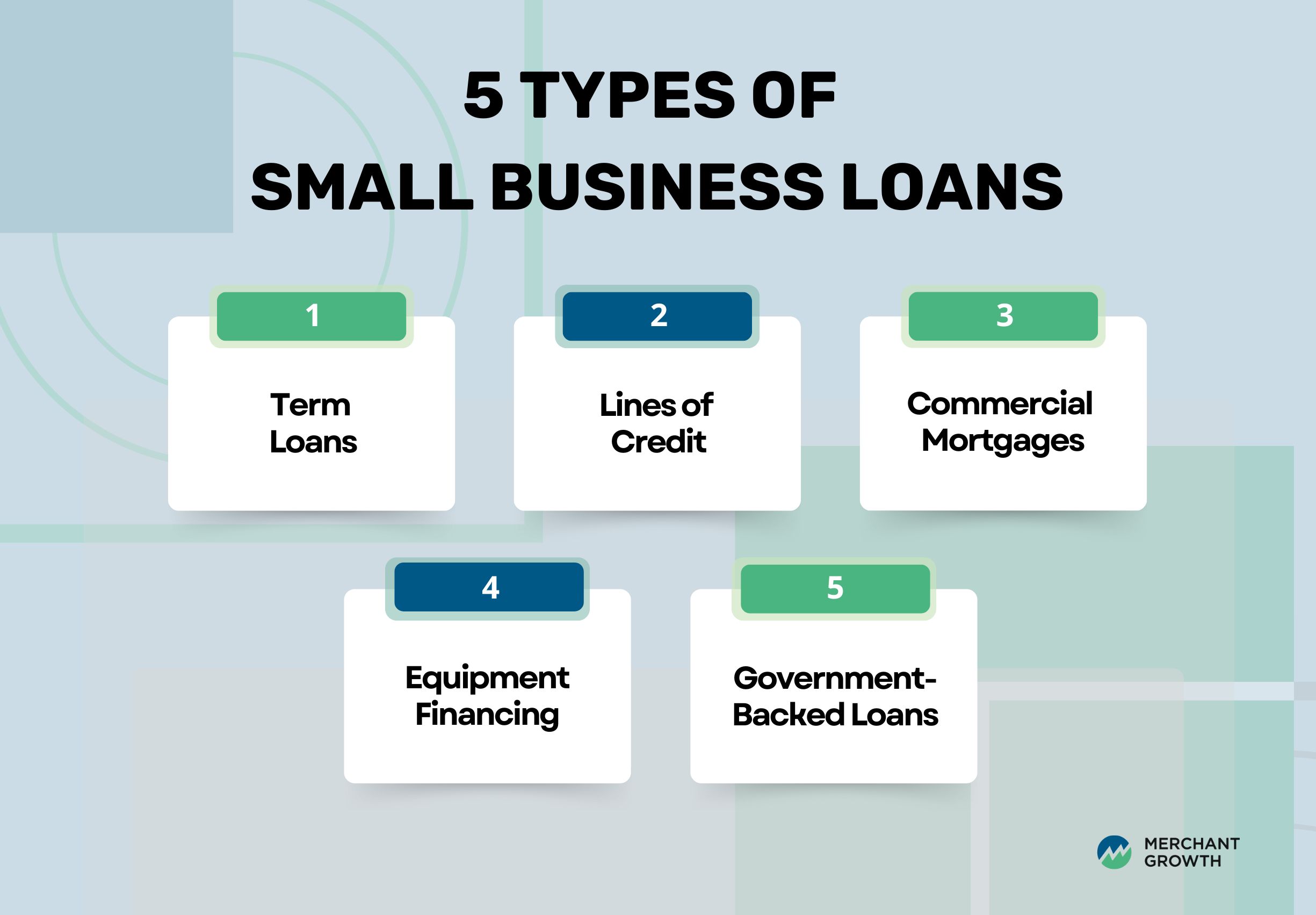

Here are some common types of loans available:

- Term Loans: These loans provide a lump sum of money upfront, which is repaid over a fixed period with interest. They’re often used for long-term investments, such as purchasing equipment or expanding your business.

- Lines of Credit: This revolving credit allows you to borrow as needed to cover short-term expenses like inventory or cash flow gaps, with interest only charged on the amount you use.

- Commercial Mortgages: These loans are used to purchase or refinance commercial real estate, secured by the property itself. They typically come with long-term repayment terms, either fixed or variable.

- Equipment Financing: Designed specifically to help businesses purchase machinery or equipment, these loans often use the equipment as collateral.

- Government-Backed Loans: These loans offer easier qualification criteria and lower interest rates for businesses looking to finance capital expenditures like real estate, equipment, or leasehold improvements.

Each of these options has unique terms and conditions, so it’s important to consider what works best for your business’s needs.

How the Canada Small Business Financing Program Works

Starting a small business can be tough, but getting financing shouldn’t have to be. That’s where the Canada Small Business Financing Program (CSBFP) comes in. It’s designed to make securing a loan a little easier for businesses that might not have all the assets banks typically require. If your business meets a few key criteria, you could be eligible for some much-needed funding.

To qualify for the CSBFP, your business must:

- Have annual revenue of less than $10 million.

- Be a for-profit business based in Canada.

The program offers a great way to access financing for capital expenditures, such as purchasing new equipment, acquiring real estate, or making improvements to your commercial space. Through the CSBFP, businesses can access up to $1 million for real estate and leasehold improvements or up to $350,000 for equipment.

How to Apply for a CSBFP Loan

Applying for a CSBFP loan is simple but does require you to go through participating financial institutions (like banks). You’ll need a few key documents, such as your business plan and financial statements, to show that your business has the potential to succeed and can repay the loan. It’s all about showing you’ve got a solid plan in place and are ready to take your business to the next level.

Government-Backed Small Business Loans: Benefits and Requirements

Government-backed loans, especially through the CSBFP, come with some seriously attractive perks. Because the government guarantees part of the loan, it reduces the risk for lenders, which makes it easier for you to qualify. Let’s break down what makes these loans so appealing:

First, you’ll benefit from lower interest rates—a big plus when it comes to saving money over time. Additionally, the repayment terms are often longer than traditional loans, which can be a relief for small business owners trying to balance growth with financial stability. Most importantly, the government guarantee reduces risk for lenders, so they’re more likely to say “yes” to your loan.

So, what do you need to qualify for a government-backed loan?

- Your business must be for-profit and based in Canada.

- Your annual revenue needs to be under $10 million—so this isn’t for the big corporations but rather small businesses just like yours.

These loans are typically meant for capital expenditures, such as:

- Purchasing equipment or machinery to help your business grow.

- Real estate purchases, whether it’s for buying new property or upgrading your current space.

- Leasehold improvements, so you can make those upgrades to a rented space without breaking the bank.

While these loans don’t cover operating expenses like payroll or inventory, they’re a great option if you need to make significant investments to support your business’s long-term growth.

Exploring Private Lending and Alternative Lenders in Canada

While government-backed loans are an excellent option for many small businesses, some entrepreneurs may find they need faster or more flexible solutions. That’s where alternative lending comes in. Unlike traditional bank loans, alternative lending offers non-traditional financing options that provide businesses with access to capital quickly and with less stringent requirements.

Alternative lending includes options like peer-to-peer (P2P) lending, online business loans, crowdfunding, merchant cash advances, and invoice financing. This type of financing began gaining traction in 2005 with the first peer-to-peer online loan, and in Canada, it has continued to grow in popularity over the past decade. As more businesses face challenges in securing funding from traditional banks, alternative lending has become a go-to solution for many, providing greater flexibility and faster access to funds.

At Merchant Growth, we’ve been part of this shift since 2009, helping Canadian businesses access quick, reliable funding when they need it most.

Advantages of Working with a Private Lender

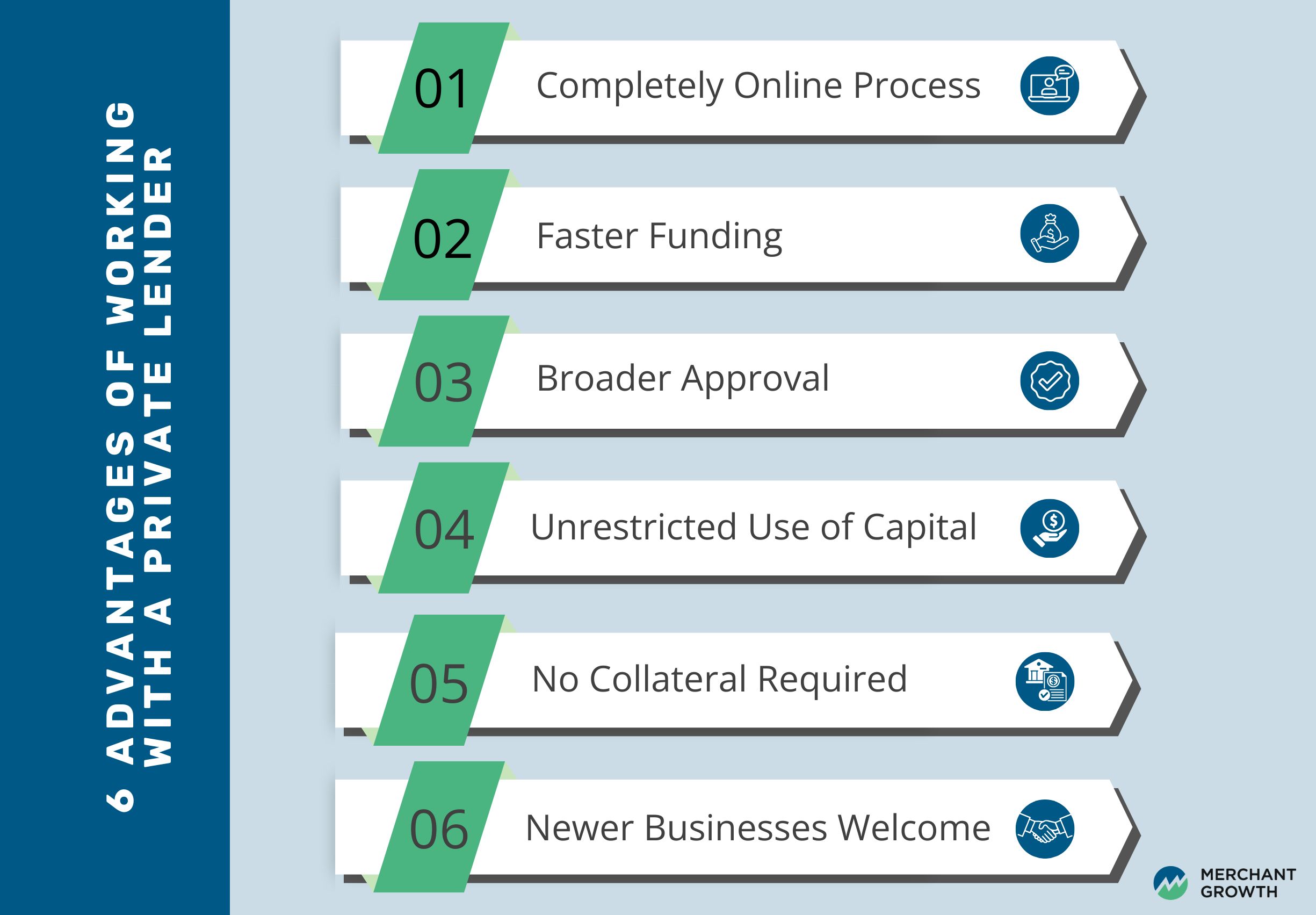

If you’re looking for a financing solution that’s fast, flexible, and tailored to your business needs, alternative lending could be the perfect fit. Here’s a look at the key benefits of working with alternative lenders:

- Completely Online Process: No more taking time away from your business, scheduling appointments, or waiting in line. With alternative lenders, you can apply whenever and wherever suits you—whether from the comfort of home or on the go via your mobile device.

- Faster Funding: Traditional banks can take weeks or even months to approve and disburse funds. In contrast, alternative lenders like Merchant Growth can provide funding in as little as 24 hours, with most businesses completing the entire process within a week.

- Broader Approval for Diverse Businesses: Banks often have stricter policies on the types of businesses they fund and may reject applications based on credit scores or industry risks. Private lenders work with a wider variety of industries, including those often overlooked by banks, offering greater flexibility in approval.

- Unrestricted Use of Capital: With no formal plan required, you have the freedom to use the funds however you need—whether it’s for inventory, hiring staff, expanding to a new location, or simply managing cash flow.

- No Collateral Required: Many private lenders, including Merchant Growth, offer unsecured loans, meaning you don’t need to provide collateral to secure funding.

- Newer Businesses Welcome: Unlike banks and government programs that often have stricter time-in-operation requirements, alternative lenders are more flexible. Merchant Growth, for example, requires just six months in business, making it accessible even for startups.

Key Considerations When Working with an Alternative Lender

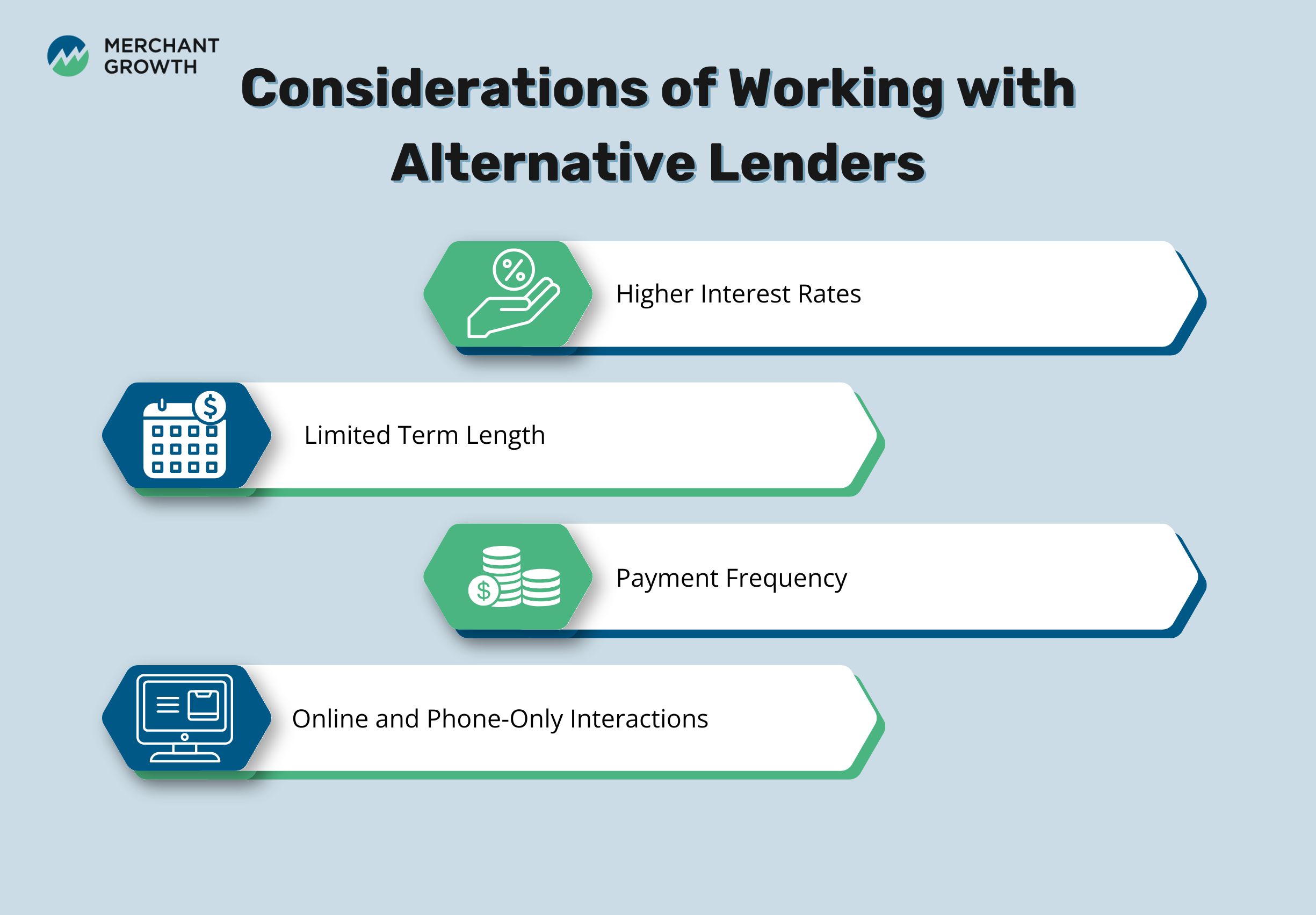

When exploring alternative lending, there are a few key factors that can impact your decision. While these options offer flexibility and speed, it’s important to understand how different terms may affect your business. Here’s what you need to know:

- Interest Rates: Private lenders often work with a wider variety of businesses and offer fast, convenient financing. However, this can mean higher interest rates compared to traditional banks.

- Term Length: Private lenders may not always offer the same loan term lengths as banks, which could limit your repayment options depending on the type of financing.

- Payment Frequency: Payment schedules may differ from those offered by banks. While some businesses find more frequent payments—like daily or weekly—manageable and beneficial, others may prefer a single, larger monthly payment, which may not always be available.

- Online-Only Interactions: For many, the convenience of an entirely online financing process is a major advantage. However, if face-to-face interactions are important to you, this may be a drawback. Although private lenders like Merchant Growth operate fully online or by phone, providing excellent customer service throughout the entire process remains a priority, ensuring that any questions or concerns are addressed promptly.

How to Apply for a Small Business Loan in Canada

Applying for a small business loan requires careful preparation to ensure your application stands out. While the process can vary depending on the type of loan and lender, following these steps will help increase your chances of success. Here’s a step-by-step guide on how to apply for a small business loan in Canada:

- Gather Your Financial Statements

Lenders want to understand your business’s financial health, so you’ll need to provide recent financial statements, including income statements, balance sheets, and monthly bank statements. These documents demonstrate your business’s ability to repay the loan and offer insights into cash flow, profits, and expenses. Be prepared to explain any financial trends that may raise questions. - Provide Proof of Business Ownership

You’ll need to prove that you own or have a legal stake in the business. This can be done by providing proof of business ownership, such as incorporation documents or partnership agreements. If you are a sole proprietor, a business registration certificate will suffice. - Submit Lease or Property Documents

Lenders will likely want to verify your physical location. This means you will need to provide documentation like a lease agreement for rented spaces or property deeds for owned spaces. This helps lenders understand the security of your business operations. - Prepare Tax Documentation

Tax returns offer a snapshot of your business’s financial status over the past few years. Be ready to submit tax documentation, including recent returns for your business. If you are a new business, you may be asked to provide personal tax returns to give a clearer picture of your financial history. - Craft Your Business Plan

A business plan is a key document that outlines your business’s vision, goals, strategies, and projections. A solid business plan helps lenders understand how you plan to grow your business and how the loan will help. It should include financial forecasts, marketing plans, and any other pertinent details that show your business’s potential for success.

Additional Tips for Increasing Your Chances of Approval

Once you’ve gathered all the necessary documents, there are a few more steps you can take to improve your chances of securing a loan. These tips can help you present a strong application and increase your likelihood of approval:

- Know the Lender’s Requirements: Different lenders may have varying requirements, so make sure to research and tailor your application to the specific lender you are applying to. Some lenders may focus more on cash flow, while others may prioritize your credit history or collateral.

- Be Transparent: If there are any issues in your financial history or projections, be transparent with the lender. They will appreciate your honesty and may work with you to find a solution.

- Check Provincial Variations: Keep in mind that loan requirements and the application process can vary by province. For example, some provinces may offer local grants or subsidies that can help with loan approval. Always check with local business development offices to see if there are specific programs that can assist your application.

By gathering the necessary documents, preparing your business plan, and understanding lender requirements, you’ll be in a stronger position to secure the financing you need.

Loan Rates for Small Businesses: What You Need to Know

When applying for a small business loan, understanding how loan rates are determined is crucial. Several factors impact the interest rate you’ll be offered, and knowing what to expect can help you plan your finances effectively. Here’s a breakdown of the key elements that influence loan rates for small businesses:

Factors That Impact Loan Rates

- Business Size: Generally, the larger and more established your business, the lower your interest rate may be. Lenders tend to see larger businesses as lower risk because they have more resources and a proven track record.

- Credit History: Your personal and business credit history plays a significant role in determining your loan rate. A strong credit score demonstrates to lenders that you’re reliable, which can help secure better terms. Conversely, poor credit may lead to higher rates due to increased risk.

- Type of Loan: The type of loan you choose will also affect the interest rate. Government-backed loans like the Canada Small Business Financing Program (CSBFP) typically come with lower rates because they’re guaranteed by the government. In contrast, loans from private lenders or alternative financing options may come with higher rates due to the increased risk they take on.

Typical Interest Rate Ranges

The interest rates you’ll face can vary significantly depending on the type of loan and the lender you work with. For government-backed loans, interest rates are typically lower, making them a more affordable option for businesses looking to borrow. On the other hand, private lenders and alternative financing options generally carry higher interest rates. The higher rates reflect the increased risk these lenders take on, especially if your business doesn’t have an established track record or solid collateral.

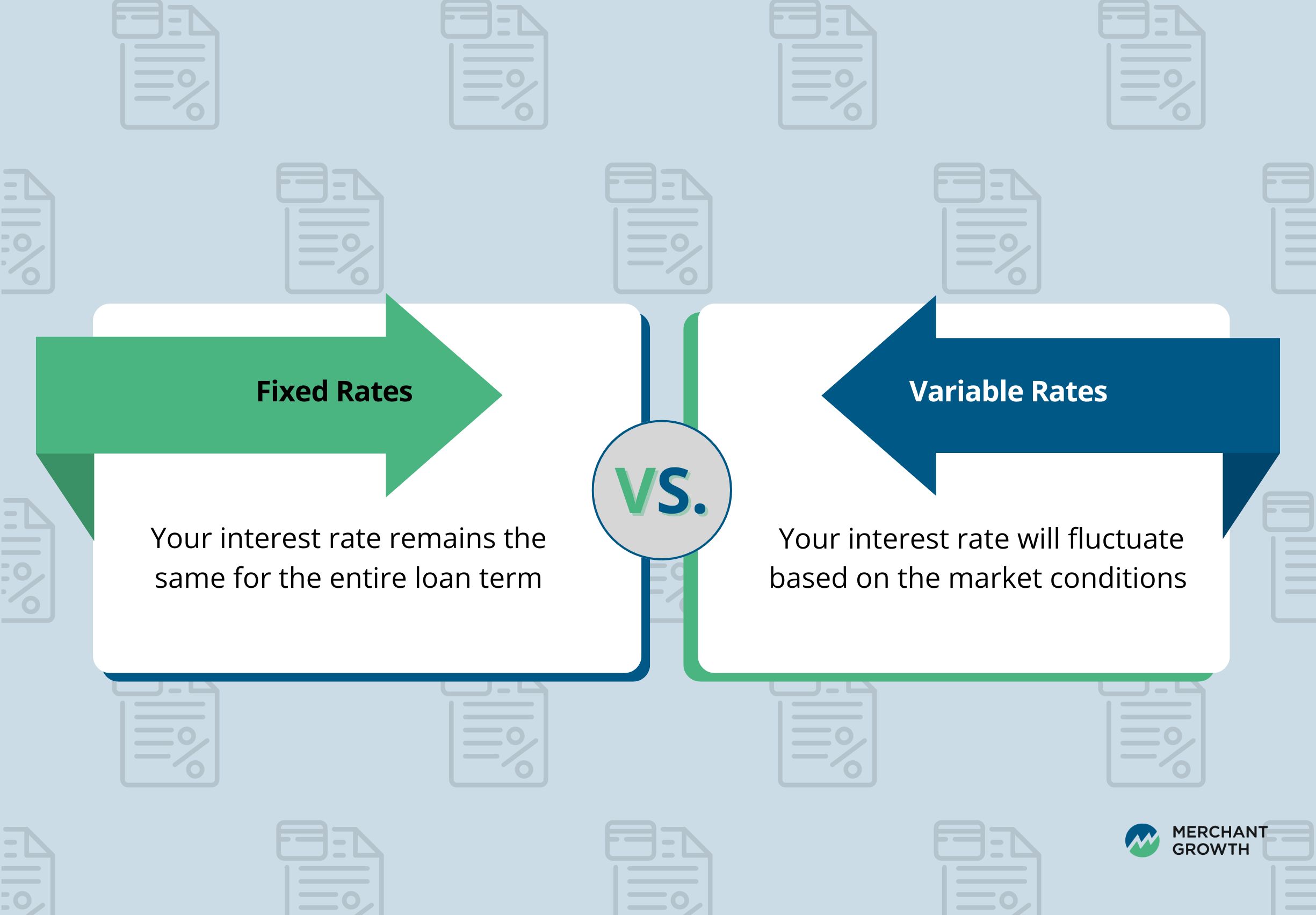

Fixed vs. Variable Rates

Loan interest rates can either be fixed or variable, and each comes with its own set of benefits. Understanding these factors and choosing the right loan type and rate structure for your business is key to maintaining healthy cash flow and avoiding financial stress.

Fixed Rates:

With a fixed-rate loan, your interest rate remains the same for the entire loan term, ensuring your payments are predictable. This is ideal for businesses that prefer stable monthly payments and want to avoid surprises. The downside is that fixed rates can sometimes be higher than variable rates, especially if market rates decrease over time.

Variable Rates:

A variable rate loan means your interest rate will fluctuate based on the market conditions or an index rate, such as the prime rate. While variable rates can start lower than fixed rates, they carry the risk of increasing if the market conditions change, leading to higher payments over time. This type of loan may be beneficial if you expect interest rates to decrease or if your business has the flexibility to handle occasional rate changes.

Understanding Loan Terms and Repayment: Avoiding Common Pitfalls

When taking out a loan for your small business, understanding the terms and repayment schedule is essential for avoiding financial stress down the road. Here’s what you need to know about loan terms and repayment:

Typical Loan Repayment Terms

Loan repayment terms can vary depending on whether you’re opting for a government-backed loan, a bank loan, or a private loan. For government-backed loans, repayment periods typically range from 5 to 10 years, depending on the type of loan and the purpose of the funds. Private loans, however, may have shorter terms, often between 1 to 5 years, especially for smaller loan amounts or working capital needs.

Repayment Schedules

Most loans follow a monthly repayment schedule, with fixed amounts due on the same day each month. However, some lenders may offer flexible repayment terms designed to accommodate seasonal cash flow fluctuations. For example, loans for businesses with irregular income, like those in retail or agriculture, may offer quarterly or annual payments to help ease financial pressure during off-seasons. Be sure to discuss these options with your lender when applying for a loan.

Common Pitfalls to Avoid

While taking out a loan can help your business grow, it’s important to be aware of common pitfalls that could strain your finances:

- Hidden Fees: Some loans come with additional fees such as origination fees, servicing fees, or penalties for early repayment. Always read the fine print to ensure you fully understand any fees associated with the loan.

- Prepayment Penalties: Some lenders charge a penalty for repaying your loan early, which can limit your flexibility. Make sure to ask about prepayment penalties and factor this into your decision-making.

- Strained Cash Flow: Ensure that the loan terms won’t create cash flow issues. Long repayment periods or high monthly payments may seem manageable at first but could become a burden if your business hits a slow patch. Always evaluate your ability to make the payments without affecting your day-to-day operations.

By thoroughly understanding your loan terms and being mindful of potential pitfalls, you’ll be better positioned to manage the loan effectively and avoid unnecessary stress.

When and How to Refinance Your Small Business Loan

Refinancing your small business loan can be a smart way to improve your financial situation, especially if your business’s needs have changed or interest rates have dropped. Here’s when and how to approach refinancing:

When Refinancing Might Be Beneficial

Refinancing can be a good option in the following situations:

- Interest Rates Decrease: If interest rates have dropped since you initially took out your loan, refinancing could help you lock in a lower rate and reduce monthly payments.

- Improved Credit: If your business’s credit has improved since you took out the original loan, you may qualify for better terms or lower interest rates.

- Shortening Loan Terms: If you want to pay off your loan faster and reduce the total interest paid over the life of the loan, refinancing to a shorter term with the same or lower interest rate may be beneficial.

The Refinancing Process

Refinancing a loan involves taking out a new loan to pay off your existing loan, ideally at better terms. Here’s how to go about it:

- Assess Current Loan Terms: Review your existing loan to understand the remaining balance, interest rate, and repayment schedule.

- Compare New Offers: Shop around and compare offers from different lenders. Look for lower interest rates, better repayment terms, or more flexible options that align with your current business needs.

- Prepare Your Documents: Just like applying for your original loan, you’ll need to provide financial documents such as recent financial statements, tax returns, and a business plan to demonstrate your business’s financial health and repayment ability.

Refinancing Costs to Watch Out For

Some loans come with refinancing fees or penalties for early repayment. These can add to the cost of refinancing, so it’s important to carefully review your current loan agreement to ensure these costs are factored into your decision. Always calculate whether the potential savings outweigh the refinancing costs before moving forward.

Making the Right Financing Choice for Your Business’s Future

Navigating small business financing involves understanding your loan options, rates, and terms to make the best choice for your company’s growth. From government-backed loans to private lending and alternative financing, each option has its own advantages and requirements. Loan repayment schedules, interest rates, and the structure of your loan play a significant role in how manageable your payments will be.

If you’re looking for financing solutions that work for your business, it’s essential to evaluate your specific needs and long-term goals carefully. By understanding the loan options available and their implications, you can make informed decisions that help set your business up for success.

At Merchant Growth, we understand that finding the right financing can be overwhelming. If traditional loans aren’t a good fit, we offer flexible funding solutions designed to meet your unique needs. Whether you need quick access to capital or a longer repayment term, we’re here to help you grow your business. Contact us today to explore how we can support your financing needs.