Is Your Business Failing? How to Recognize the Signs, Rebuild with Confidence, and Access Support in Canada

Running a small business comes with ups and downs, and if you’re feeling like the challenges are starting to outweigh the wins, you’re not alone. Many business owners experience periods of financial stress, declining momentum, or even full-blown burnout. The important thing is recognizing the warning signs early and knowing that there are proven strategies and support systems available to help you recover.

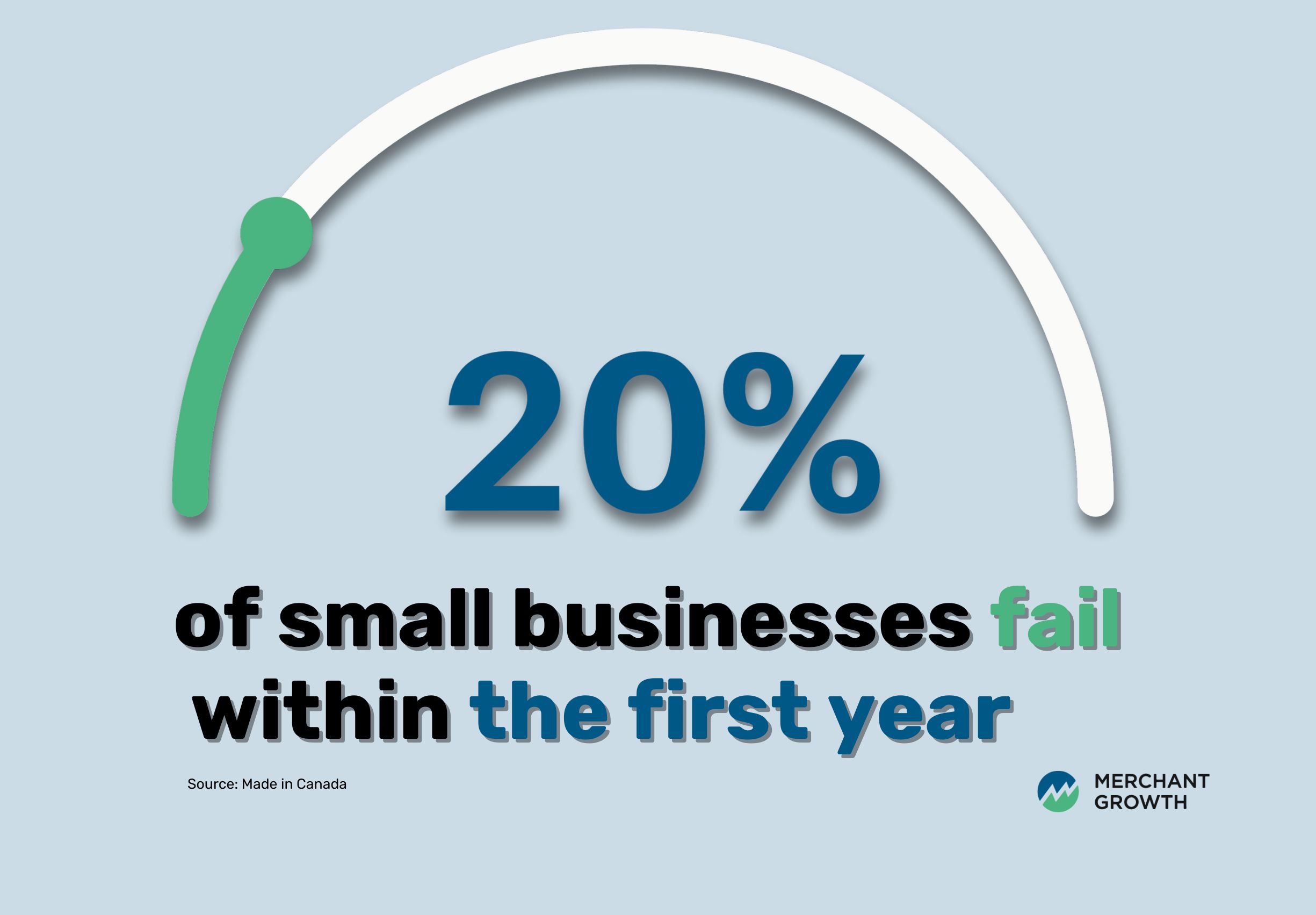

According to Made in Canada, about 20% of small businesses don’t survive their first year. But that means approximately 80% do—and with the right tools and support, many struggling businesses can be turned around.

In this article, we’ll walk you through how to spot trouble early, figure out your next steps, and tap into the resources that can help your business get back on track.

Key Takeaways

- Business failure can stem from cash flow issues, poor planning, shifting markets, or burnout, but these challenges can be addressed with the right strategies.

- Recognizing early warning signs like declining revenue, customer loss, or staff turnover is critical.

- Canadian small businesses have access to support, from government programs (BDC, Futurpreneur, etc.) to advisory services and financing solutions.

- Not every business can be saved, but many can be stabilized, pivoted, or reborn with the right approach.

Early Warning Signs of a Failing Business

Spotting trouble early can mean the difference between a successful recovery and having to shut your doors for good. In fact, only about 7% of businesses cite a ‘failure to make necessary changes’ as the primary cause for closure, highlighting just how powerful it can be to adapt when warning signs appear. Here are some red flags that should prompt a closer look:

- Declining revenue or shrinking profit margins

- Cash flow crunches and unpaid bills

- Mounting debt or rejections from lenders

- Loss of regular customers or increased churn

- High staff turnover or low team morale

- New competitors or changing market demand

- Missed deadlines, disorganized operations, or unclear roles

If several of these signs feel familiar, take it as your cue to act, not out of panic, but out of possibility. Identifying issues early gives you the best chance to course-correct, stabilize, and build a stronger, more resilient business.

Common Reasons Small Businesses Fail

Understanding why small businesses fail isn’t about placing blame—it’s about empowering yourself with the knowledge to avoid the same missteps. Many entrepreneurs pour their hearts, time, and savings into their ventures, only to be blindsided by avoidable pitfalls. Whether it’s a lack of planning, poor cash flow management, or not adapting to market changes, the root causes of failure often follow predictable patterns. By getting clear on what commonly derails small businesses, you can make smarter, more informed decisions to protect your own. Below, we break down the key challenges Canadian entrepreneurs face—and how to navigate them.

Poor Planning or Lack of a Business Model

Without a clear plan or strategy, it’s easy to drift. Whether it’s skipping market research, overestimating demand, or failing to forecast expenses, weak business planning puts you at a disadvantage from day one.

Tip: Create a simple business plan—even a one-page version—that outlines your goals, target market, revenue model, and key expenses. Tools like the BDC’s free business plan template can make this process easier and more focused.

Inadequate Marketing

If you’re not reaching the right audience or clearly showing what makes your business different, it’s hard to stand out, let alone grow. According to the CFIB, 42% of small businesses fail because they haven’t properly researched the market. That means many entrepreneurs launch without fully understanding who their customers are, where to find them, or what messages resonate.

Tip: To avoid falling into this trap, take time to define your target audience, study their behaviours, and test different marketing channels. Even a small, consistent marketing strategy can go a long way in building awareness and attracting loyal customers.

Over-Reliance on One Revenue Stream

Many businesses fail because a single client or product line dries up. Diversification is essential to long-term resilience. When too much depends on one revenue source, any disruption—like a client leaving or a product becoming obsolete—can quickly spiral into a crisis.

Tip: Explore complementary revenue streams such as new product offerings, subscription models, or targeting different customer segments. Even a modest second stream can provide helpful stability.

Weak Cash Flow Management

A lack of financial visibility is one of the top reasons small businesses fail. Late payments, poor pricing strategies, or over-investment can quickly drain your resources and leave you scrambling to cover expenses. In fact, 22% of small business owners expect to face challenges maintaining their cash flow, highlighting just how common and critical this issue is.

Tip: Use cash flow forecasting tools or work with a bookkeeper to project future cash flow needs. Review pricing regularly to ensure you’re covering costs and building in a margin for growth.

Business Owner Burnout

Business owners often wear every hat, and it catches up fast. Chronic stress, decision fatigue, and isolation can lead to poor choices or a complete loss of motivation.

Tip: Build rest and support into your business plan. Set realistic work hours, take regular breaks, and seek out mentors, peer networks, or even part-time help to reduce isolation and overload.

External Pressures

Economic downturns, supply chain disruptions, and regulatory changes can throw even successful businesses off course. These are often out of your control, but how you respond makes all the difference.

Tip: Stay agile by regularly reviewing industry trends, maintaining strong supplier relationships, and having contingency plans in place for major disruptions.

Assessing Your Business’s Financial Health

When a business starts to struggle, it’s easy to focus on surface-level symptoms—missed deadlines, mounting stress, or slow sales. But the root cause often lies in the numbers. Understanding your financial health is one of the most important steps in regaining control and avoiding deeper trouble. Consider it a financial health check—looking closely at your cash flow, revenue, and obligations to understand where your business truly stands.

Here are key areas to examine:

- Cash Flow Statement: Are your incoming funds consistently covering your expenses? If not, your business may be at risk of running into operational trouble. Download our free Cash Flow Statement Template to help you get a clearer picture ➡️ Download Here

- Profit & Loss Trends: Are you profitable month to month? Is your growth flat, steady, or slipping?

- Debt & Loan Obligations: Are repayments manageable, or are they adding strain?

- Payroll & Vendor Payments: Are you paying people (or yourself) on time, or constantly behind?

- Client Base: Are customers sticking around, or are you always trying to replace lost business?

These indicators can reveal not just how your business is doing—but where to focus your efforts first. Even small improvements in one area can create a ripple effect. Don’t be discouraged by what you find. This isn’t about perfection; it’s about clarity, direction, and taking control.

What Does “Going Concern” Mean in Business?

You may have heard the term “going concern” in business conversations, but what does it actually mean? In simple terms, it’s the assumption that your business will continue to operate and generate income in the foreseeable future, typically at least the next 12 months.

But when that assumption is at risk—due to sustained losses, cash flow problems, or mounting debt—your business may no longer be considered a going concern. This status has serious implications and is often a red flag to lenders, investors, and even employees.

Signs your business may no longer be a going concern:

- You’re unable to pay your bills or meet payroll consistently

- Your debt is growing faster than your revenue

- You’ve lost access to financing or are being turned down for credit

- Auditors raise concerns about your financial statements

- You’re relying heavily on personal savings or short-term fixes to stay afloat

Why it matters:

- It affects how you report your finances, potentially requiring disclosure of material uncertainty in your statements

- It can impact your ability to raise funds or renew lines of credit

- It signals to stakeholders (employees, partners, banks) that significant changes may be needed

Recognizing and addressing these risks early gives you a better chance to stabilize and rebuild before the situation becomes irreversible.

Revisit Your Business Model and Strategy

When your business hits a plateau—or worse, begins to decline—it’s often not just about cash flow or marketing. The root issue may lie in the foundation: your business model. What once worked to attract and retain customers may no longer meet market needs, especially in fast-changing industries or economic conditions.

Taking a step back to assess your overall strategy can give you the clarity needed to make smart, intentional changes. Think of it less as starting over and more as a recalibration.

Here are some questions to guide your evaluation:

- Does your product or service still solve a real problem?

- Are there new audiences you could reach?

- Can you adjust pricing or add new revenue streams?

- Are your operations bloated or outdated?

Small, strategic changes—like bundling your services, refining your niche, or experimenting with new sales channels—can breathe new life into a tired business model. The key is to stay curious, test ideas, and be willing to pivot. A fresh perspective might reveal untapped opportunities hiding in plain sight.

Canadian Support Programs That Can Help

You are not alone. Whether you’re experiencing a slow season, rethinking your strategy, or trying to turn your business around, there are many support systems across Canada designed to help small business owners like you.

From mentorship and financial guidance to grants and digital adoption programs, these resources can offer the tools, insight, and encouragement you need to move forward with confidence. Tapping into the right support at the right time can make all the difference.

Here’s a snapshot of national and regional programs worth exploring:

| Resource | What It Offers |

|---|---|

| BDC (Business Development Bank of Canada) | Advisory services, small business loans, planning tools, and financial calculators. |

| Futurpreneur Canada | Financing and mentorship for entrepreneurs aged 18–39, including business plan support. |

| Canada Digital Adoption Program (CDAP) | Grants and expert advisors to help small businesses modernize their digital operations. |

| Provincial Programs | Most provinces offer their own funding, training, or low-interest loan programs through economic development offices or business hubs. |

| Local Chambers of Commerce | Access to networking events, training sessions, and local business advisors or consultants. |

If you’re unsure where to start, consider speaking with a local mentor, accountant, or business coach. These professionals can help you map out a recovery plan and connect you with the programs that fit your goals and challenges best. Sometimes, just having a sounding board can reframe a tough situation—and remind you that better days are ahead.

How to Deal with Burnout as a Business Owner

Burnout isn’t just being tired—it’s a state of chronic physical, mental, and emotional exhaustion that can make even basic business decisions feel overwhelming. And it’s more common than most entrepreneurs admit.

In fact, two-thirds of small business owners reported feeling close to burnout in 2022, and over half said they were actively struggling with their mental health. With so many hats to wear and never enough hours in the day, it’s no surprise. A healthy work-life balance is not just a nice-to-have—58% of Canadian small business owners say it’s crucial to long-term success.

Recognizing what’s causing your burnout is the first step toward managing it. Here’s a breakdown of common triggers and how to address them:

| Cause | Strategy to Manage It |

|---|---|

| Overworking with no breaks | Set clear work hours and stick to them. Use scheduling tools to create structured time off—even just an hour or two daily. |

| Constant financial pressure | Work with a financial advisor to build a realistic budget or seek out flexible financing options to ease short-term stress. |

| Isolation from peers or mentors | Join a local small business network, peer mastermind group, or online community to share experiences and gain support. |

| Decision overload | Delegate low-impact decisions where possible. Use checklists, SOPs, or hire a virtual assistant to streamline daily choices. |

| Disconnect from business purpose | Revisit why you started. Reflect on wins, review client testimonials, or set fresh short-term goals to reignite motivation. |

No business thrives when the person running it is burned out. Seeking support—whether through mentorship, therapy, or a trusted network—can make the journey more manageable. Don’t wait until you’re running on empty. Just like your business, your well-being needs ongoing investment.

Resources:

For mental health and burnout prevention, explore the Government of Canada’s guide to preventing burnout and BDC’s entrepreneur well-being resources for practical tools and support.

Should You Pivot, Downsize, or Close?

It’s a tough truth: not every business survives in its original form. But choosing to pivot, scale down, or close isn’t a failure—it’s a smart, strategic decision that many successful entrepreneurs have made. Sometimes letting go of what’s not working is the bravest and most empowering move you can make.

If you’ve been losing money month after month, feeling constant anxiety, or noticing that your business is harming your health, relationships, or overall quality of life—it may be time to re-evaluate. You’re not alone. Thousands of small business owners each year go through this process, and many come out stronger on the other side.

Here are some options to consider, and when they might make sense:

| Option | When to Consider It |

|---|---|

| Pivot to a more viable offering | You’ve identified a product, service, or market with stronger demand or profitability, and still feel committed to entrepreneurship. |

| Downsize to reduce costs | Overhead is too high, but you believe in the business. Shrinking operations could give you time to regroup. |

| Merge with a complementary business | You’ve found a business with strengths that complement yours—joining forces could spark new growth. |

| Sell your assets | You’re ready to step away, but have valuable assets. Selling helps recover investment and move on cleanly. |

| Close your business legally and cleanly | You’ve tried other paths, but it’s time to move on. Formal closure frees you from future obligations. |

If you’re considering a major change—whether that’s pivoting, downsizing, or exiting entirely—what matters most is making a thoughtful, informed decision. Reflect on your goals, weigh the trade-offs, and seek guidance if needed. Clarity, not pressure, should drive your next move. Your future success doesn’t depend on holding on—it depends on choosing what’s right for you now.

Not sure where to start? ➡️ Download our Is Your Business at Risk? Self Assessment Quiz to help identify key warning signs and clarify your next step.

How to Close a Business in Canada

Deciding to close your business can be emotional and complex, but once the choice is made, handling the closure properly is essential. From notifying the CRA to settling outstanding debts, following the right steps ensures you remain compliant, protect your finances, and leave the door open for future opportunities. Below is a clear, step-by-step guide to closing a business in Canada responsibly and efficiently.

Step 1 – Decide on a Closure Date

Your closure date will act as the anchor point for everything that follows. Choose a date that gives you enough time to notify employees, inform clients, fulfill any outstanding orders, and manage final accounting. Providing advance notice shows professionalism and helps maintain your reputation.

Step 2 – Notify the CRA

Once you’ve chosen your closure date, inform the Canada Revenue Agency. You’ll need to cancel your Business Number as well as associated accounts like GST/HST, payroll deductions, and corporate income tax. Doing this prevents further tax obligations from accruing. You can start the process through the CRA’s official “Closing your business” page.

Step 3 – Finalize Employee Obligations

If you have employees, this step is critical. You’re responsible for issuing final paycheques, preparing T4 slips, and submitting Records of Employment (ROEs). Make sure you’re meeting all legal requirements related to notice periods, severance (if applicable), and final remittances.

Step 4 – Settle Debts & Collect Receivables

Take a full inventory of what your business owes and what it’s owed. Pay off any outstanding debts to suppliers, lenders, or service providers. At the same time, follow up on unpaid invoices or accounts receivable to bring in any final income before you close your books.

Step 5 – Cancel Licences and Insurance

Reach out to your municipal and provincial licensing bodies to cancel any business licences or permits. Do the same with your insurance provider to end commercial policies like liability, equipment, or property insurance. Be sure to keep a record of these cancellations.

Step 6 – Close Bank Accounts and Credit Lines

Close all business bank accounts and credit lines once your final transactions have cleared. This prevents future charges or fraudulent activity and helps you avoid ongoing fees. If your business account is linked to other services, be sure to unlink and transition them.

Step 7 – File Final Tax Returns

Even if your business is winding down, you still need to file one last set of tax returns. This includes GST/HST filings, corporate income tax returns, and payroll deductions. Submit all necessary paperwork to ensure you remain compliant and avoid penalties.

Step 8 – Retain Records

By law, you must retain business records for at least six years after closure. This includes financial statements, invoices, payroll records, and correspondence with the CRA. Store these records securely—digitally or physically—in case of audits or future reference needs.

Stabilize, Simplify, and Rebuild Confidence

When a business has gone through a rough patch, jumping straight into growth mode isn’t always the answer. In fact, recovery often starts with slowing down, taking stock, and simplifying what’s already there. It’s about regaining control, reducing unnecessary complexity, and building back your confidence—one decision at a time.

Here are some simple but powerful ways to stabilize your operations:

- Cut unnecessary subscriptions, tools, or office space that no longer serve your core needs

- Streamline your invoicing process to improve cash flow and reduce missed payments

- Double down on your most profitable services or products—let go of anything that drains time or resources

- Reconnect with loyal clients through personalized outreach to reignite trust and repeat business

Even modest changes can make a big difference. By reducing overwhelm and focusing on what works, you can build a more sustainable business foundation. Momentum builds with clarity, and every small win is a step toward long-term success.

Rebuilding with the Right Tools

If you’re facing business struggles, you’re not alone—and you’re not without options. Many entrepreneurs face bumps (or brick walls) on the road to success.

What matters most is how you respond.

Revisit your business model. Monitor your cash flow. Seek expert advice. Protect your mental health. Explore available resources.

Merchant Growth offers financing solutions tailored to Canadian small businesses, including:

- Term Financing for large one-time investments

- Lines of Credit to support cash flow or marketing pushes

With the right mindset and support system, many businesses find new life even after hitting a rough patch.

Ready to take the next step? Explore how Merchant Growth can help your business regain momentum and move forward with confidence.