How Do You Pay Yourself from Your Business? A Guide for Canadian Entrepreneurs

Running a business comes with plenty of challenges—but one of the trickiest questions for Canadian entrepreneurs is surprisingly simple:

How do I pay myself?

If you’re like many business owners, you’re great at serving customers, managing expenses, and building your brand—but when it comes to paying yourself, things get murky. Should you take a salary? Pay yourself dividends? What about taxes?

We are here to help. Let’s break down how to pay yourself from your business legally, confidently, and in a way that supports both your own personal income and your company’s success.

Key Takeaways

- How you pay yourself depends on your business structure. Sole proprietors usually take draws, while incorporated owners often choose between salary, dividends, or both.

- Salary provides steady income and CPP contributions. Dividends may offer tax advantages but aren’t considered earned income for RRSPs or CPP.

- It’s important to balance personal pay with business cash flow and tax obligations.

- The smartest approach often involves working with an accountant to build a compensation plan that supports growth—and avoids surprises at tax time.

Do Business Owners Get a Paycheque? An Overview

Short answer: sometimes—but it depends on how your business is set up.

In Canada, there’s no one-size-fits-all approach to paying yourself as a business owner. The right method depends on your business structure—whether you’re a sole proprietor, part of a partnership, or run an incorporated company. Most Canadian entrepreneurs pay themselves in one (or a combination) of three ways: an owner’s draw, a salary, or dividends. Each option comes with its own tax rules, paperwork requirements, and long-term financial considerations. Here’s how they work:

Owner’s Draw

- Common for: Sole proprietors or partnerships

- How it works: You withdraw profits directly from the business account to your personal account.

- Tax note: No payroll deductions or T4s required, but you still pay personal income tax on the business’s net profit.

Salary

- Common for: Incorporated business owners

- How it works: You pay yourself like an employee through payroll, deducting income tax and contributing to CPP (Canada Pension Plan).

- Tax note: The business deducts your salary as an expense, and you receive a T4 slip at year-end. Creates RRSP room and contributes to CPP.

Dividends

- Common for: Incorporated business owners with retained earnings

- How it works: You pay yourself from the corporation’s after-tax profits.

- Tax note: Dividends don’t require payroll setup, don’t contribute to CPP, and are taxed at a different (often lower) rate than salary.

Each method has its own benefits and drawbacks. Let’s break it down a bit further based on business structure.

How to Pay Yourself as a Sole Proprietor in Canada

If you’re a sole proprietor, you don’t pay yourself a salary—you pay yourself by taking an owner’s draw. This means transferring money from your business account to your personal account when needed.

What You Need to Know:

- You pay personal income tax on your business’s net profit (not just what you draw).

- There are no payroll deductions (like CPP or EI) at the time of payment, but you’re still responsible for taxes at year-end.

- It’s crucial to keep clear records of all withdrawals.

Pro Tip:

Consider setting aside at least 25-30% of your profits for taxes and Canada Pension Plan (CPP) contributions. Using separate accounts for business and personal expenses makes this easier.

How to Pay Yourself from a Corporation: Salary vs. Dividends

If you’ve incorporated your business in Canada, you have more flexibility in how you pay yourself—but that also means more decisions to make. The two main options are salary and dividends, and many business owners use a combination of both to balance personal income needs with tax efficiency.

Choosing between salary and dividends isn’t just about how you receive money—it affects your taxes, retirement savings, CPP contributions, and even how lenders view your income. Each method has advantages and trade-offs, depending on your goals, cash flow, and the stage your business is in.

Paying Yourself a Salary

Paying yourself a salary means you become an employee of your own corporation. Your business issues regular paycheques, deducts income tax, and handles Canada Pension Plan (CPP) contributions—just like it would for any other employee.

What You Need to Know:

- Requires setting up payroll and remitting taxes to the CRA.

- Salary payments are a tax-deductible expense for the corporation, reducing its taxable income.

- Creates RRSP contribution room based on your earned income.

- Contributes to CPP, helping you build retirement income.

- You’ll receive a T4 slip at year-end.

Paying Yourself Dividends

Dividends are a way to pay yourself a share of the company’s after-tax profits. Instead of running through payroll, you transfer funds from the corporation to yourself as a shareholder distribution.

What You Need to Know:

- No payroll setup is needed dividends are recorded in corporate records and reported via T5 slips.

- Dividends are taxed personally at a different (often lower) rate than salary, depending on your province and income level.

- They don’t generate RRSP room or contribute to CPP.

- Because no CPP is paid, you may need to plan for your retirement savings separately.

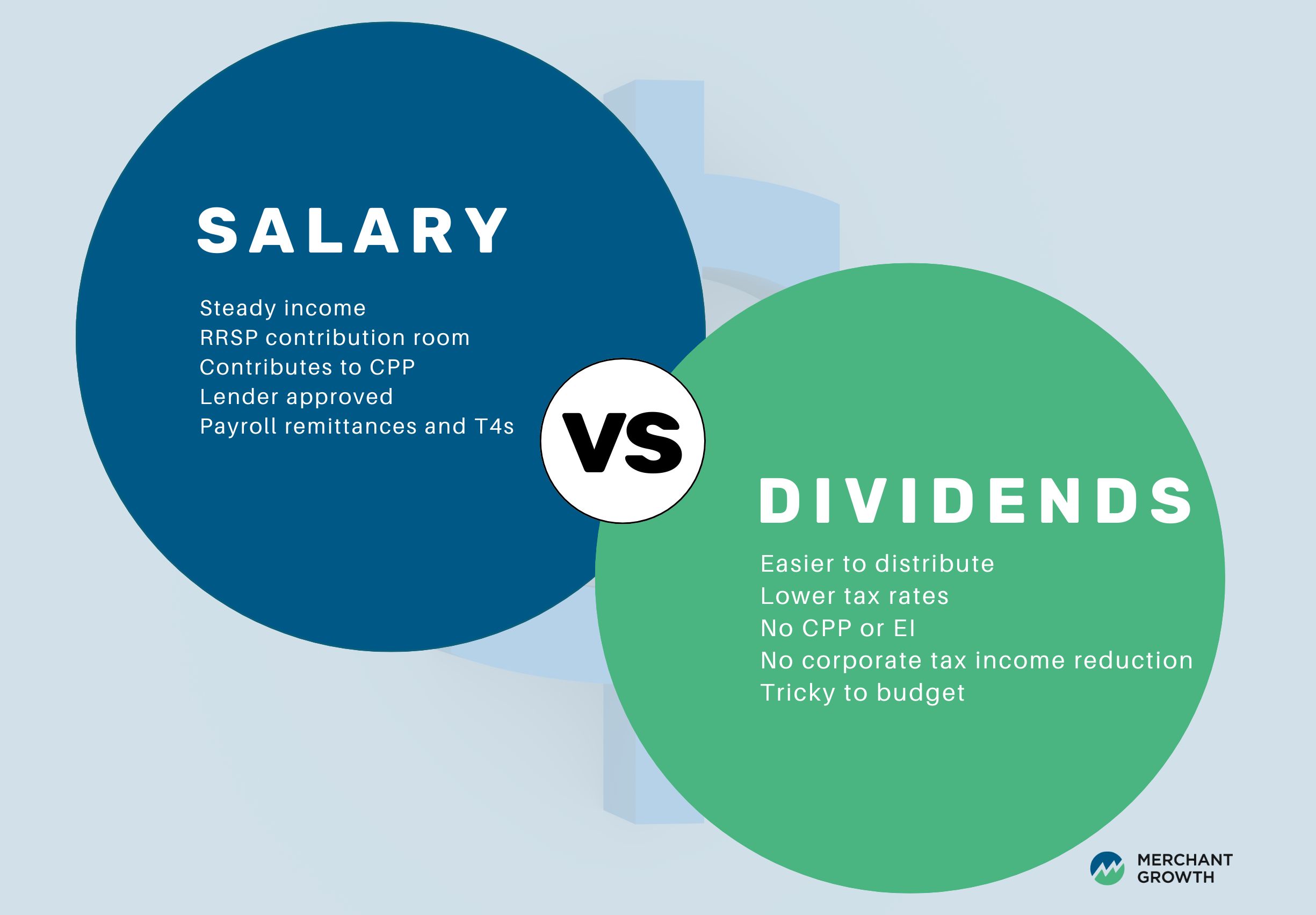

Pros and Cons of Salary vs. Dividends

Not sure whether to take a salary, dividends, or both? Each option comes with trade-offs. Here’s a quick comparison to help you weigh the benefits and drawbacks:

| Salary | Dividends |

|---|---|

| Creates steady, predictable income | Easier to distribute—no payroll setup |

| Builds RRSP contribution room | Often taxed at a lower rate |

| Contributes to CPP (future retirement benefits) | No CPP or EI required |

| Requires payroll remittances and T4s | Doesn’t reduce corporate taxable income |

| Better for loan/mortgage applications | May make personal budgeting trickier |

The best choice depends on your business goals, cash flow, and personal financial situation. It’s not about picking one method forever—it’s about finding the right mix for where you are now.

What Percentage Should You Pay Yourself?

There’s no one-size-fits-all answer—but asking the right questions can help you land on a number that’s sustainable for both your business and your personal life. Start with these:

- Can your business afford it?

Review your monthly cash flow. Are you consistently bringing in more than you’re spending? If not, consider holding off on large self-payments or starting with a small salary until you stabilize your business finances. - What do you need to cover your personal expenses?

Calculate your baseline living costs—housing, groceries, savings, debt payments—so you know what you need to take home. This gives you a target number. - Are you setting aside enough for taxes?

Whether you’re paying yourself through draws, salary, or dividends, taxes will apply. Work with your accountant to estimate how much to set aside for CRA payments so you’re not caught off guard. - What about growth?

Are you reserving funds to reinvest in your business—like hiring, new equipment, or marketing? Paying yourself should be part of the plan, but not at the expense of long-term growth.

Once you’ve answered these questions, set a reasonable pay target and revisit it regularly. Your goal is to strike a balance: pay yourself enough to live (and save), while keeping the business healthy and positioned to grow.

How Much to Pay Yourself (Without Hurting the Business)

Once you understand there is no concrete percentage of profit you should take away from your business, the next step is figuring out how much is reasonable to pay yourself, without putting your company at risk.

Here are some practical guidelines to help:

- Pay yourself a portion of monthly profits, leaving room for taxes and reinvestment.

- Compare your pay to industry norms or consider what you’d pay someone else to do your job.

- Build in room for business expenses and savings before determining your take-home amount.

When Should You Start Paying Yourself?

Many new business owners wait too long to pay themselves. While it’s smart to be cautious in the early days, you should aim to start paying yourself when:

- The business generates consistent profit (even modest amounts).

- You have at least a few months of operating expenses saved.

- You’ve stabilized customer acquisition and operating costs.

Paying yourself isn’t just a reward—it’s a sign your business model is working.

Working with an Accountant or Bookkeeper

When it comes to paying yourself, taxes are where things often get tricky—especially if you’re juggling salary, dividends, or both. The last thing you want is to make a mistake that costs you time, money, or penalties from the CRA.

That’s where a trusted accountant or bookkeeper comes in. They can help you:

- Set up payroll the right way (if you’re taking a salary)

- Stay on top of your personal and business tax obligations

- Avoid costly mistakes or CRA penalties

- Build a plan for retirement, savings, and future growth

Even better? You don’t have to do it all manually. Cloud-based tools like Wagepoint, QuickBooks Payroll, and Wave make automating payroll and remittances simple—so you can focus on running your business, not stressing over spreadsheets.

What Does “Pay Yourself First” Really Mean?

You’ve probably heard the phrase “pay yourself first”—but what does that actually mean for small business owners?

At its core, paying yourself first is about making your personal financial health a priority, not an afterthought. It means setting aside a portion of your income for yourself before spending on other expenses, just like you would with personal savings. For business owners, that can feel counterintuitive—especially when you’re used to pouring every dollar back into the business. But if you never prioritize your own paycheck, it’s easy to burn out or fall into financial stress.

How to Apply “Pay Yourself First” in Your Business:

- Set a baseline salary or draw—even if it’s small at first.

- Build your pay into your budget as a non-negotiable monthly expense.

- Separate personal and business finances so you can see clearly what’s coming in and what’s going out.

- Don’t wait for “leftover” cash to pay yourself—plan for it upfront.

This approach isn’t about being selfish—it’s about sustainability. Your business exists to support your life, not the other way around. When you pay yourself first, you’re creating a healthier balance between business growth and personal well-being.

How Merchant Growth Can Help You Build a Sustainable Business Income

Building a consistent paycheque as a business owner often requires investing in your systems—whether that’s hiring a bookkeeper, setting up payroll, or planning for growth.

At Merchant Growth, we understand that balancing your income with your business’s needs isn’t always easy. That’s why we offer flexible term financing and lines of credit to help Canadian entrepreneurs:

- Cover upfront costs like accounting software or payroll services

- Create cash flow cushions for lean months

- Reinvest in growth while maintaining personal income

With the right support, you can pay yourself fairly—without jeopardizing your business’s future.

Talk to Merchant Growth today about financing solutions that support your business—and your paycheck.