How to Start a Small Business in Canada: A Step-by-Step Guide for Entrepreneurs

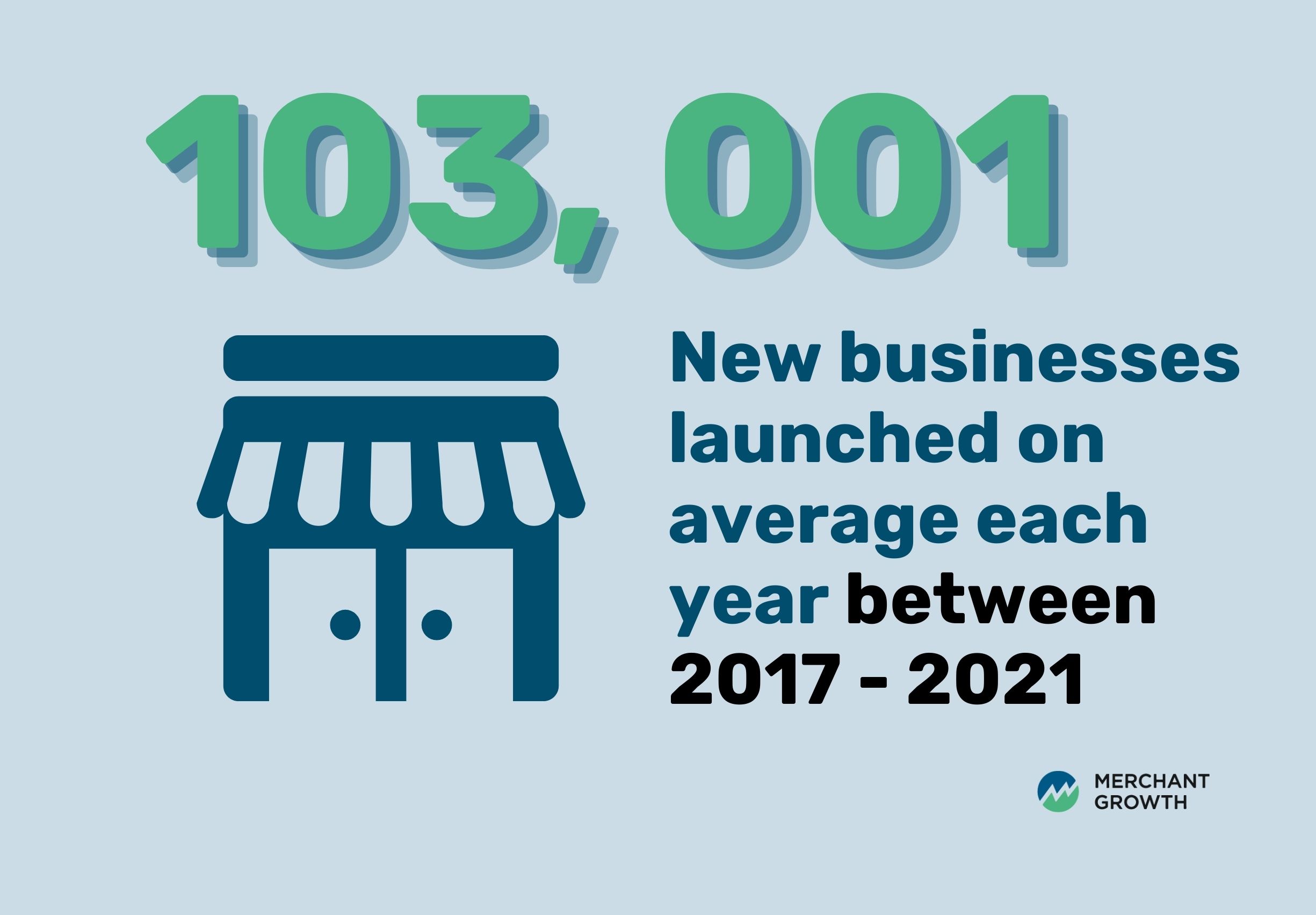

Thinking about starting a small business in Canada? You’re in good company. Between 2017 and 2021, an average of 103,001 new small businesses were launched each year, showing that Canadians are constantly turning ideas into reality.

Of course, starting a business comes with its challenges—figuring out the right idea, understanding your customers, navigating regulations, and finding the funding to get off the ground. That’s exactly what this guide is here for. Step by step, we’ll walk you through everything you need to know to start your small business, from shaping your idea and planning your budget to registering your business, securing funding, and launching with confidence. With practical tips and real Canadian resources along the way, you’ll have the roadmap you need to turn your vision into a thriving business.

Key Takeaways

- Business Planning: A detailed plan maps your goals, strategy, and finances, and serves as a guide for decision-making.

- Business Registration: Choosing a name and registering your business legally is crucial for compliance and credibility.

- Licensing & Permits: Ensure you have all the required licenses to operate without interruptions.

- Funding Options: Grants, loans, and alternative financing options can provide the capital you need to start strong.

- Growth Strategy: Budgeting for future growth ensures you can scale without financial stress.

How to Start a Small Business in Canada

Turning your business idea into a reality takes more than passion—it takes planning, smart decisions, and a clear roadmap. Canada offers plenty of resources to help new entrepreneurs, but you’ll still need to navigate things like choosing the right business structure, understanding regulations, managing taxes, and securing funding. Let’s break down each step in a practical, easy-to-follow way, starting with understanding your market and finding the right audience for your product or service.

Conduct Market Research

Before investing time and money, understanding your market is critical. Market research helps identify who your ideal customers are, what they need, and how your business can meet those needs better than competitors. Let’s look at four simple ways you can dig into the market and gather the insights you need to make smart decisions.

Understand Your Target Audience:

Start by getting clear on who you’re trying to serve. Think beyond just age and gender—consider lifestyle, habits, motivations, and pain points. Create a simple customer profile or persona:

- Who are they?

- What problems do they face that your business can solve?

- Where do they spend their time online and offline?

Once you have this profile, you can tailor your marketing, product development, and even pricing to match their expectations. Tools like surveys, social media polls, or even casual conversations with potential customers can give you real insight into what they want.

Analyze Competitors:

Understanding your competition is more than knowing their prices—it’s about uncovering their strengths and weaknesses. Look at local businesses and online competitors offering similar products or services. Check their websites, read customer reviews, follow them on social media, and see what people like or dislike about them. Take notes on their marketing approach, customer experience, and product offerings. The goal isn’t to copy them, but to find ways to differentiate your business and offer something uniquely valuable.

Identify a Gap in the Market

Once you understand your target audience and your competitors, the next step is spotting opportunities where your business can stand out. Look for areas where competitors’ products or services don’t fully meet customer needs—maybe they’re inconvenient, outdated, or missing features that your audience wants.

Ask yourself:

- What are customers frustrated with in current offerings?

- Is there a way to make a product or service simpler, faster, or more enjoyable?

- Are there groups of people whose needs aren’t being addressed at all?

Pinpointing these gaps gives your business a competitive edge and increases the chances of success. By offering something unique that solves real problems, you’re not just entering the market—you’re filling a space that customers have been waiting for.

Stay Updated on Industry Trends:

Markets are always changing, and staying ahead of trends can give your business an edge. Subscribe to industry newsletters, follow key influencers, and check government or trade association reports for insights. For example, the Government of Canada offers industry-specific data and reports that can help you spot opportunities or potential challenges in your sector. By understanding trends, you can anticipate customer needs, adapt your offerings, and make more informed strategic decisions

Use Reliable Data:

There’s nothing like hearing straight from your potential customers. Try informal methods like chatting with people in your target market, conducting interviews, or sending out short surveys. Online platforms like Google Forms, Typeform, or social media polls make it easy to gather feedback quickly. Pay attention to recurring themes or concerns—these can guide everything from product design to pricing and marketing. The more you understand your audience from their own perspective, the better positioned your business will be to serve them effectively.

Conducting thorough market research ensures your business idea is viable and gives you the insights needed to make informed decisions. With a clear understanding of your customers, competitors, and industry trends, you’re ready to take the next step: planning your business and turning those insights into a concrete strategy for success.

Plan for Your Business

A solid business plan isn’t just a document—it’s your roadmap for turning an idea into a thriving business. It helps you clarify your vision, map out financial projections, and plan operational strategies. Most importantly, it gives you the confidence to make informed decisions and shows potential investors or lenders that you’ve thought things through. Let’s break down the first steps to building your business plan and shaping your idea into something real.

Coming Up with a Business Idea:

Every successful business starts with a strong idea, but not every idea is ready to become a business. Start by thinking about your skills, passions, and the needs you see in the market. Ask yourself:

- What problems can I solve?

- What gaps exist that my business could fill?

Once you have a few ideas, test them by talking to potential customers, getting feedback, and refining your concept. The goal is to land on an idea that excites you and has a clear market demand.

Choosing a Location vs. Working from Home:

Where your business operates can have a big impact on costs, accessibility, and customer reach. If you need foot traffic or local visibility, a physical storefront might make sense—but it comes with higher overhead. Running a business from home can reduce costs, but you’ll need to think creatively about reaching customers online or delivering your services. Consider a hybrid model or co-working spaces if you want flexibility while keeping some professional presence.

Deciding Between Employment Models

Before hiring anyone or setting your own role, think about how you want your business to operate. Do you plan to hire full-time staff, rely on contractors, or manage everything as a solo entrepreneur? Each option has implications for taxes, benefits, and operational workload. Map out the responsibilities and decide which model makes sense now—and how it might evolve as your business grows.

Set Goals:

Before you dive into writing your business plan, it’s important to get clear on your goals. Short-term goals—like landing your first customers or launching your website—help you focus on immediate priorities, while long-term goals—like reaching revenue milestones or expanding your offerings—give your business direction and purpose.

Make your goals SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of “I want more customers,” try “I want 50 new customers in the first six months through social media and local events.” Clear goals make your plan actionable and give you a roadmap for measuring progress as your business grows.

Writing Your Business Plan

Now it’s time to pull everything together into a cohesive plan. Your business plan should outline:

- Your business concept and goals

- Market research and target audience

- Marketing and sales strategies

- Operational plan and staffing

- Financial projections and budget

Be as detailed as possible, but keep it clear and readable. Remember, your plan is meant to guide you, not overwhelm you.

Pro Tip: To make this process easier, you can use our own business plan template—designed specifically for Canadian entrepreneurs—to structure your ideas and build a plan that’s ready for funding, growth, and long-term success.

Choosing Your Business’s Name

Your business name is often the first thing customers notice, so it’s worth taking the time to get it right. A great name captures what your business stands for, is easy to remember, and sets you apart from the competition. Let’s break down how to choose a name that works for your brand.

Brainstorm Meaningful Names:

Start by thinking about what your business represents and what makes it unique. Consider your products, services, target audience, and brand personality. Don’t be afraid to get creative—sometimes the best names come from wordplay, metaphors, or combining ideas. Write down everything that comes to mind, then narrow the list based on which names are memorable, clear, and resonate with your customers.

Check for Availability:

Once you have a shortlist, it’s crucial to make sure your name isn’t already taken. In Canada, you can use the NUANS database to check if your desired business name is registered or too similar to existing businesses. If your name is already in use, try slight variations or add a descriptive term that highlights what your business does. This step protects you from legal headaches and ensures your brand can stand out.

Consider Online Presence:

A business name is only as good as your ability to promote it. Check if the domain name is available for a website and whether social media handles match your name. Even if you’re starting small, securing your online identity early can save you headaches later and make marketing easier as your business grows.

Choosing the right name takes time, but it’s an investment that pays off in brand recognition and credibility. With a strong name in place, you’re ready to move on to picking the right business structure, which sets the foundation for your legal, tax, and operational decisions.

Select the Appropriate Business Structure

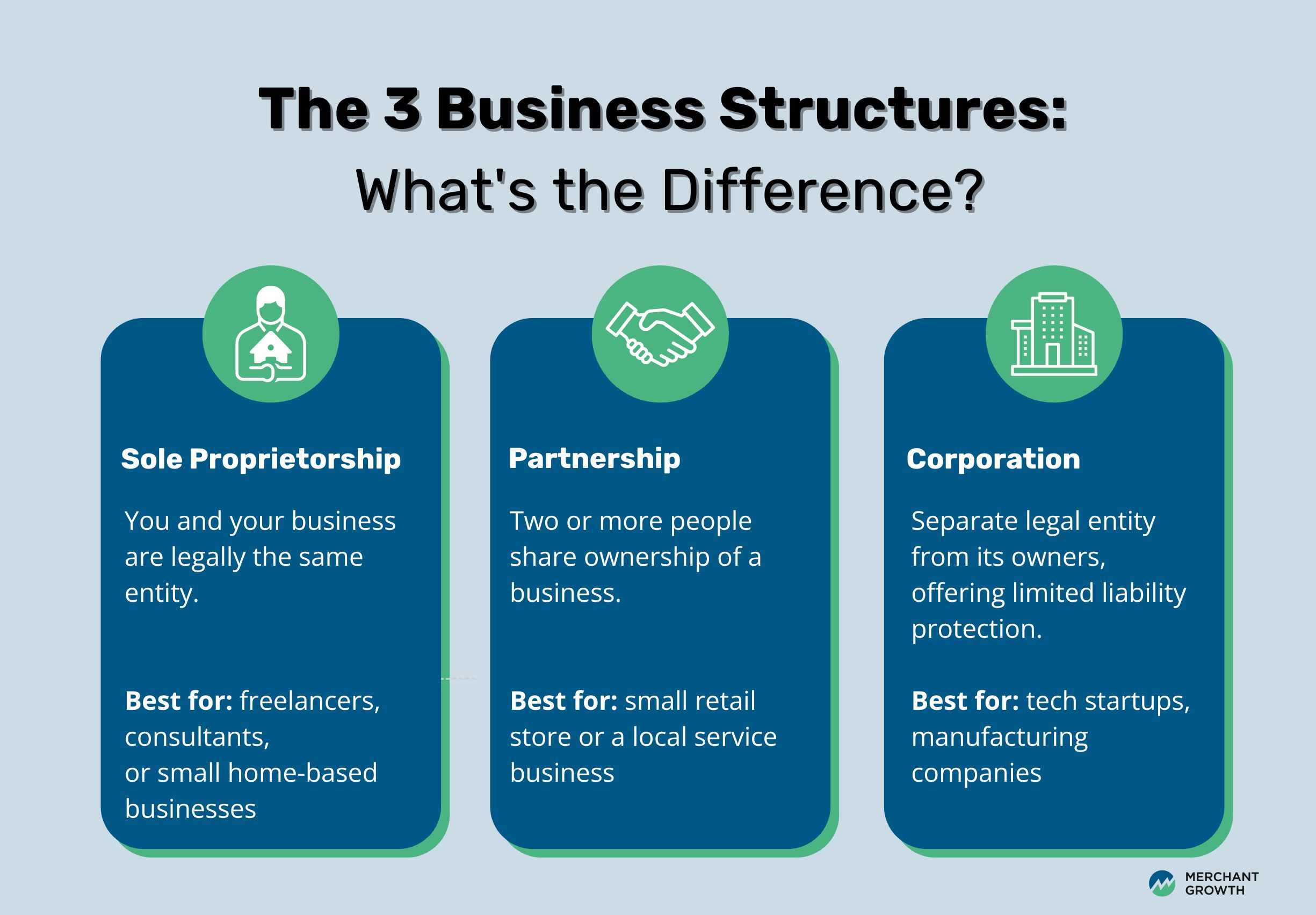

Choosing the right business structure is more than a formality—it shapes your taxes, liability, and day-to-day responsibilities. Picking the right model from the start can save you money, simplify operations, and protect you legally. In Canada, there are three main options:

Sole Proprietorship:

A sole proprietorship is the simplest and most common structure for small businesses. You and your business are legally the same entity, which means you report income on your personal tax return and have full control over decisions. The main trade-off is personal liability: if your business runs into debt or legal trouble, your personal assets are on the line.

This model works best for freelancers, consultants, or small home-based businesses just getting started. It’s easy to set up, low-cost, and gives you full control, making it perfect for solo entrepreneurs who want to test their ideas with minimal risk.

Partnership:

A partnership is when two or more people share ownership of a business. Partners share responsibility for decisions, profits, and debts. Partnerships can be general (where everyone is equally responsible) or limited (where some partners have limited liability).

This structure works well when you have trusted business partners and complementary skills. For example, a small retail store or a local service business might benefit from pooling expertise and resources. Clear agreements are essential to outline roles, responsibilities, and how profits are shared.

Corporation:

A corporation is a separate legal entity from its owners, offering limited liability protection. This means personal assets are generally safe if the business faces legal or financial challenges. Corporations also have potential tax advantages and can make it easier to raise investment capital.

Corporations are ideal for businesses with growth ambitions, like tech startups, manufacturing companies, or businesses looking to attract investors. Keep in mind that corporations involve more paperwork, legal compliance, and ongoing reporting requirements than other structures, so they’re best for those ready to commit to the extra effort.

Each structure has different tax and legal implications, so it’s worth reviewing your options carefully. The Canada Business Network offers detailed guidance to help you decide which structure fits your business goals.

Registering Your Business

Now that you’ve picked a business name and chosen your structure, you’re ready to make it official. Legal registration is a critical step—it ensures your business is recognized by the government, can open bank accounts, enter into contracts, and access funding. Thankfully, you’ve already completed some of the groundwork with the decisions you made in the previous steps, which makes the registration process much smoother.

- Decide on your business name

- Choose your structure (sole proprietorship, partnership, corporation)

- Register your business federally or provincially using the Canada Business Registrations Portal

- Keep copies of registration documents for tax and legal purposes

Once you start the online registration, you’ll notice the process is fairly straightforward but still requires careful attention. You’ll enter details about your business, confirm your structure, and submit your chosen business name for approval. Depending on your location and the type of registration, the process can take anywhere from a few hours to a few days, especially if you need name approval or additional permits. Most of the time, you can complete everything online through the Canada Business Registrations Portal, but having all your information ready in advance—like your structure, business address, and ownership details—will make the process much smoother.

Registering your business officially is a milestone: it turns your idea into a legal entity, sets the stage for growth, and opens the door to funding, banking, and other essential services.

Business Licenses and Permits

Once your business is legally registered, the next step is ensuring it meets all the rules and regulations that apply. Depending on your industry, location, and the services you provide, you may need one or more licenses or permits to operate legally. These aren’t just bureaucratic hurdles—they protect your business, your customers, and your employees, while keeping you compliant with the law. Let’s break down the main types of permits and licenses you might need in Canada, and where to obtain them.

Municipal or City Licenses

Municipal licenses are issued by your city or town and are required to operate within a specific municipality. They ensure that your business meets local zoning and safety regulations.

Examples: A retail shop, daycare, or hair salon typically needs a municipal business license.

Obtaining a municipal license: Visit your city or town’s business licensing office or website to review requirements and submit applications. Many municipalities allow online applications, which can simplify the process.

Health and Safety Permits

If your business involves handling food, providing healthcare services, or offering personal care services, you’ll need health-related permits to ensure your operations meet provincial or federal health regulations.

Examples: Restaurants, food trucks, tattoo studios, and physiotherapy clinics all require specific health permits.

Obtaining health permits: Contact your provincial health authority or local public health office for guidance on the necessary inspections, certifications, and compliance steps.

Specialized Industry Permits

Certain industries are more heavily regulated and require additional specialized permits to operate. These can include environmental, construction, retail, or childcare permits, depending on the business type.

Examples: Construction companies may need building permits, retail stores may need alcohol or tobacco licenses, and childcare centers require provincial approvals.

Obtaining specialized permits: Check with the relevant provincial or federal department overseeing your industry. Tools like BizPaL can help identify exactly which permits are required for your business.

Federal Permits and Licenses

Some businesses require federal-level permits, especially if they involve transportation, broadcasting, banking, or interprovincial operations.

Examples: Import/export companies, financial services, or national delivery services.

Obtaining federal permits: These are issued by specific federal departments. Start with the Canada Business Network or BizPaL to determine which federal agency administers the required permits for your business.

Navigating licenses and permits might feel overwhelming at first, but having them in place is essential for smooth operations and avoiding fines or shutdowns. With your business registration complete, you now have the foundation to identify exactly what you need and apply efficiently.

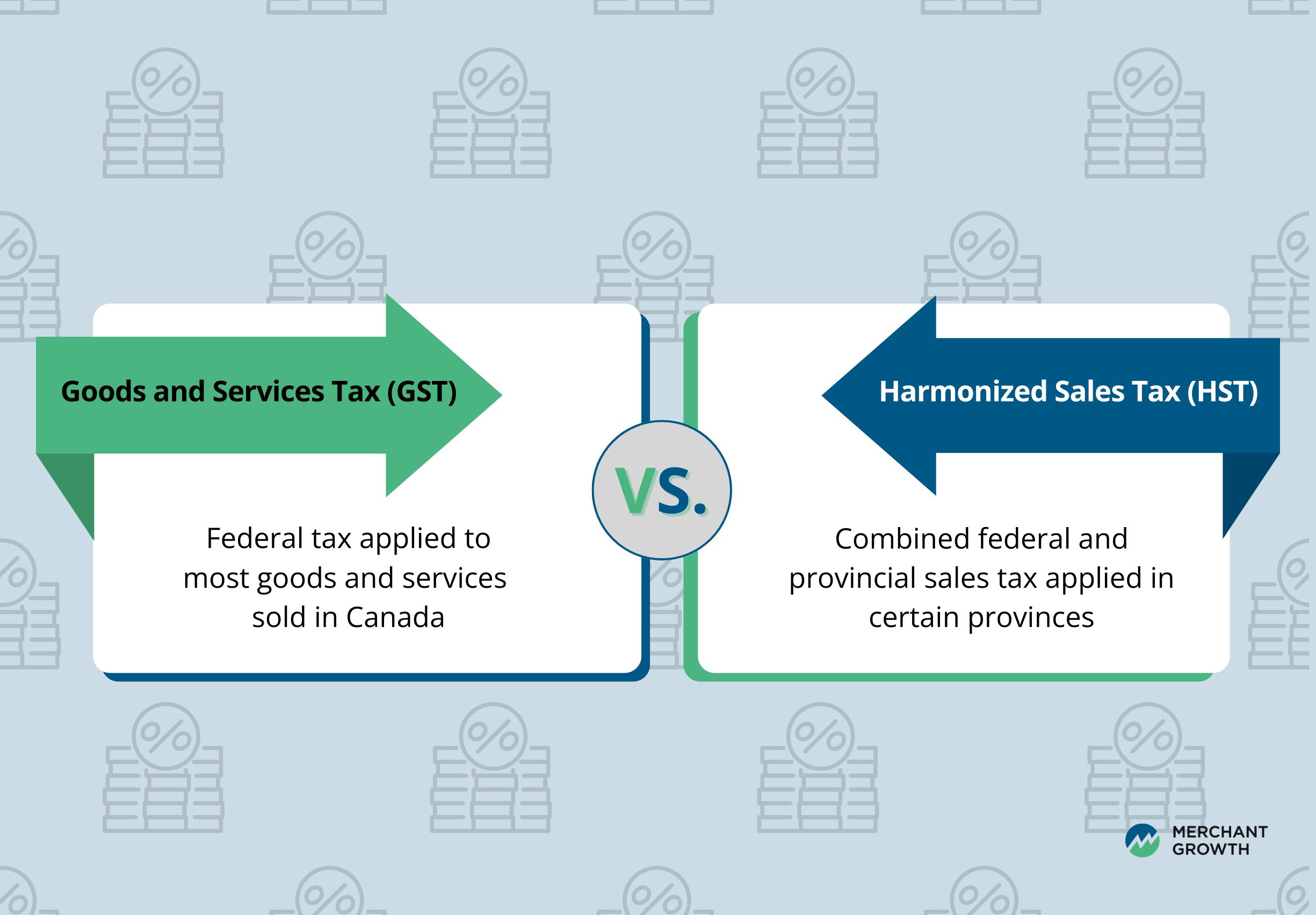

GST/HST Registration

When you start a small business in Canada, understanding taxes early is crucial. If your business generates more than $30,000 in annual revenue, you’re required to register for GST (Goods and Services Tax) or HST (Harmonized Sales Tax). Registering ensures you comply with federal and provincial tax laws and can claim input tax credits on business expenses.

Understanding GST and HST

GST (Goods and Services Tax): A 5% federal tax applied to most goods and services sold in Canada.

HST (Harmonized Sales Tax): A combined federal and provincial sales tax applied in certain provinces, replacing the separate GST and provincial sales tax. The HST rate varies depending on the province:

| Province | HST Rate |

|---|---|

| Ontario | 13% |

| New Brunswick | 15% |

| Newfoundland and Labrador | 15% |

| Nova Scotia | 14% |

| Prince Edward Island | 15% |

Provinces not listed above (e.g., British Columbia, Manitoba, Saskatchewan, Quebec) charge GST at 5% plus separate provincial sales tax (PST) where applicable. Here is a breakdown of PST for the applicable provinces:

| Province | PST Rate |

|---|---|

| British Columbia | 7% |

| Manitoba | 7% |

| Quebec | 9.975% |

| Saskatchewan | 6% |

Alberta, Northwest Territories, Nunavut and the Yukon all simply charge GST for a sales tax rate of 5% total. Understanding the right tax rate for your location ensures you charge customers correctly and remain compliant.

How to Register and File Your GST/HST

Getting started with registration: The easiest way to register for GST/HST is through the Canada Revenue Agency’s Business Registration Online portal. You’ll need your business number, legal business name, and contact information. Registration is straightforward and usually completed within a few minutes online.

Filing your returns:

Once registered, you’ll need to collect GST/HST from customers and submit periodic returns to the CRA. Most small businesses file either quarterly or annually, depending on revenue and preference. Filing can be done through CRA’s online services, by mail, or through your accounting software if it supports GST/HST reporting. Keeping accurate records of all sales and expenses will make filing much easier and help ensure you claim eligible input tax credits to reduce your net tax payable.

Registering for GST/HST might feel like a big step, but once in place, it’s simply a part of your ongoing financial routine—and one less worry as you focus on growing your business.

Budgeting for Your Business & Future Growth

A budget is more than just numbers on a spreadsheet—it’s a tool that keeps your business financially healthy and helps you make smart decisions. Without a clear picture of your income and expenses, it’s easy to overspend, miss opportunities, or struggle when unexpected costs pop up.

Start with Startup and Operating Costs

Begin by outlining all your startup costs (equipment, inventory, marketing, website development, and any professional fees. Then, factor in ongoing expenses like rent, utilities, payroll, insurance, and supplies. Being thorough here helps you understand exactly how much you need to get your business off the ground and keep it running smoothly.

Plan for Growth and Unexpected Expenses

Budgeting isn’t just about today—it’s about tomorrow. Set aside funds for unexpected expenses, like equipment repairs or temporary drops in revenue, and think ahead to future growth. Whether you plan to expand your product line, hire additional staff, or open a new location, incorporating these plans into your budget ensures you’re ready when opportunities arise. For more guidance, check out our business budgeting template and article on planning for expansion—they’ll help you map out both short-term and long-term goals.

Staying on Top of Your Budget

A budget is only useful if it’s actively managed. Track your income and expenses regularly using tools like QuickBooks Canada or Wave Accounting, and review your budget at least monthly. Compare your projections to actual spending to spot trends, adjust your forecasts, and make informed decisions. Small adjustments now can prevent bigger problems later.

Budgeting might sound tedious, but it gives you confidence. When you know where your money is going and how to plan for growth, you can focus on what matters most: building a business that thrives.

Be Aware of Tax Requirements

Budgeting and managing cash flow go hand in hand with understanding your tax obligations. Taxes can feel complicated, but getting a handle on them from the start will save you time, stress, and potential penalties. Knowing what you owe, when to pay, and what deductions you can claim helps keep your business financially healthy and compliant.

Filing Obligations

How often you file your taxes depends on both your business structure and your annual revenue:

- Sole Proprietorships and Partnerships: Generally file once a year along with your personal income tax, but GST/HST filings depend on revenue. Small businesses under $30,000 annual revenue can usually file annually, while those above may need to file quarterly or monthly.

- Corporations: Must file a corporate tax return every year, regardless of income. Larger corporations may have additional installment payments throughout the year.

Regularly reviewing your filing schedule ensures you’re never caught off guard and helps you plan your cash flow accordingly.

Payroll Taxes

If you have employees, you’re responsible for deducting and remitting several payroll taxes at both the federal and provincial levels:

- Canada Pension Plan (CPP) Contributions: Deducted from employee pay and matched by the employer.

- Employment Insurance (EI) Premiums: Deducted from employee wages and matched by the employer, with rates varying slightly by province.

- Income Tax Withholding: Deducted based on the employee’s income and province of residence.

These contributions must be remitted to the CRA on a regular schedule—monthly or quarterly, depending on your payroll size. Missing deadlines can result in penalties, so setting up reliable payroll software or consulting an accountant is highly recommended.

Incentives and Deductions

The Canadian government offers several programs and deductions designed to support small businesses:

- Small Business Deduction (SBD): Lowers the corporate tax rate for Canadian-controlled private corporations.

- Provincial Tax Credits: Programs like Ontario’s Innovation Tax Credit or British Columbia’s Small Business Venture Capital Tax Credit can help offset expenses related to research, development, or investment.

- Other Deductions: You can also deduct legitimate business expenses such as home office costs, vehicle expenses, and professional fees.

Exploring these programs early can reduce your overall tax burden and free up cash to reinvest in growth. The CRA’s Small Business section provides comprehensive guidance to help you identify eligible programs and ensure compliance.

Confirm if You Will Need Insurance

Almost every business faces some level of risk—whether it’s property damage, an accident involving a client, or an error in the services you provide. That’s why understanding your insurance needs early is essential. While not all types of coverage are mandatory, having the right insurance can protect your business, your finances, and your peace of mind. Let’s break down the main types of insurance you may need.

- General Liability: Covers third-party injuries or property damage.

- Property Insurance: Protects your assets and equipment.

- Professional Liability: Important for consultants, designers, and advisors.

- Workers’ Compensation: Mandatory if hiring employees.

Not every business requires all of these coverages, and some industries have specialized insurance requirements. The Insurance Bureau of Canada provides guidance and tools to help identify which types of insurance apply to your business. Consulting with a licensed insurance broker can also help ensure you have adequate protection without paying for unnecessary coverage.

Identify Industry Regulations

Running a business in Canada comes with responsibilities beyond making sales or providing services. Depending on your industry and location, you’ll need to comply with a range of laws and regulations designed to protect employees, customers, and the public. Understanding these rules early can save you time, money, and legal headaches. Below are the key areas most small businesses need to consider:

Health and Safety Laws

Health and safety regulations are essential for protecting employees and customers. Any business with a physical workspace—offices, stores, restaurants, or manufacturing facilities—must follow provincial and federal workplace safety standards. This includes providing proper training, safety equipment, emergency procedures, and reporting any workplace incidents. For example, a construction company must follow strict occupational health guidelines, while a restaurant must maintain hygiene and food safety protocols.

Zoning Laws

Before choosing your business location, it’s important to verify that your intended operations are allowed in that area. Zoning laws dictate where certain types of businesses can operate, such as retail stores, manufacturing facilities, or home-based offices. Checking with your municipal zoning office can prevent costly relocations or fines later on. For instance, a small café may not be allowed to operate in a strictly residential zone without a special permit.

Employment Standards

Employment laws govern minimum wage, working hours, overtime, and other labor requirements. These standards ensure fair treatment of employees and vary by province. If you hire staff, you must comply with these rules and provide things like vacation pay, breaks, and termination notice. Here’s a snapshot of the current minimum wages across Canada:

| Province/Territory | Minimum Wage (2025) |

|---|---|

| Alberta | $15.00 |

| British Columbia | $17.85 (Increase June 1 annually) |

| Manitoba | $15.80 (Increase to $16.00 October 1, 2025) |

| New Brunswick | $15.65 |

| Newfoundland & Labrador | $16.00 |

| Nova Scotia | $15.70 (Increase to $16.50 October 1, 2025) |

| Ontario | $17.20 (Increase to $17.60 October 1, 2025) |

| Prince Edward Island | $16.00 (Increase to $16.50 October 1, 2025) |

| Quebec | $16.10 |

| Saskatchewan | $15.00 (Increase to $15.35 October 1, 2025) |

| Northwest Territories | $16.95 |

| Nunavut | $19.75 |

| Yukon | $17.94 |

Minimum wage as of September 1, 2025, Source: Wagepoint

Intellectual Property (IP)

Protecting your business ideas, brand, and creative work is critical. IP laws cover trademarks, patents, copyrights, and trade secrets. For example, if you’ve developed a unique product, applying for a patent can prevent competitors from copying it. A distinctive brand name or logo can be protected as a trademark, and original content, like websites or marketing materials, is automatically protected by copyright. Understanding IP rules helps maintain your competitive advantage.

The Canadian Government offers detailed guidance on industry regulations, ensuring your business stays compliant with federal, provincial, and municipal laws. Taking the time to understand these requirements now makes future growth smoother and avoids costly legal issues.

Secure Funding for Your Small Business

Turning your business idea into reality usually requires some capital. Whether it’s covering startup costs, purchasing inventory, or marketing your new venture, having access to the right funding can make all the difference. Fortunately, Canada has a variety of financing options for entrepreneurs, ranging from traditional loans to government-backed programs and alternative lenders. Understanding your options early helps you choose the best path for your business and ensures you can grow sustainably.

- Small Business Loans: Traditional banks and credit unions offer loans designed specifically for startups. These loans often come with structured repayment plans and competitive interest rates, making them a reliable option for businesses that need larger upfront capital.

- Grants: Government programs, like the Canada Small Business Financing Program or provincial-level grants, provide non-repayable funding for eligible businesses. Grants are typically aimed at specific sectors, growth initiatives, or innovation projects.

- Alternative Lenders: Online lenders, peer-to-peer platforms, and microloan programs offer more flexible financing options, often with faster approval times. These can be a good solution if you don’t meet traditional lending criteria.

Having a clear business plan is critical when seeking funding—it demonstrates to lenders or grant providers that you’ve carefully considered your expenses, revenue projections, and growth strategy. Later, we’ll dive deeper into each funding type, including tips for applying, eligibility criteria, and strategies to improve your chances of approval. With the right funding in place, you’ll be better positioned to bring your business vision to life and tackle the challenges that come with growth.

How Much Does it Cost to Open a Small Business?

The costs of starting a business in Canada can vary significantly depending on your industry, location, and the scale of your operations. While some businesses can start with just a few thousand dollars, others may require substantial upfront investment. Understanding the different types of expenses and planning for them carefully is key to keeping your business financially healthy.

Business Registration

Registering your business is one of the first legal steps to operating in Canada. It officially recognizes your business, allows you to open a business bank account, and is required if you want to access funding, grants, or government programs.

The cost of registration varies depending on your business structure and whether you register provincially or federally. For example, sole proprietorships typically have lower registration fees, while corporations involve higher costs due to more complex filings and compliance requirements. Provincial registration fees usually range from $60 to $500, depending on the province and the type of business. Keep in mind that these are base fees—additional costs may apply for extra filings, name searches, or specialized business licenses.

Equipment and Inventory

Equipment and inventory costs depend heavily on the type of business you’re launching. A home-based online store may only need a computer, printer, and initial stock, while a café or retail shop will require commercial-grade equipment, furniture, and larger inventory.

Examples of startup equipment and inventory:

- Retail: Shelving, point-of-sale systems, initial stock

- Food services: Kitchen appliances, utensils, refrigeration units

- Office-based services: Computers, software, desks, office supplies

Startup costs can range widely—from a few hundred dollars for home-based operations to tens of thousands for brick-and-mortar businesses. Planning carefully helps ensure you don’t overspend while still investing in what’s essential.

Marketing and Website

Marketing is an essential cost to attract and retain customers. Initial expenses can include branding, logo design, website setup, social media advertising, and printed materials. While small businesses can sometimes start with lower-cost marketing strategies, investing in a professional online presence and brand identity can make a significant difference.

Examples of marketing activities and materials:

- Website domain and hosting

- Social media campaigns and content creation

- Flyers, business cards, and signage

- Email marketing platforms and customer relationship management (CRM) tools

Expect marketing costs to vary depending on your approach—some businesses may spend a few hundred dollars initially, while others may invest thousands to create a polished brand presence.

Operational Expenses

Ongoing operational expenses are essential to keep your business running smoothly. These include:

- Rent or lease for physical locations

- Salaries and wages for employees

- Utilities such as electricity, water, internet, and phone

- Software subscriptions, insurance, and supplies

- Maintenance or shipping costs

Even small businesses need to budget for at least several months of operational expenses before they start turning a profit. Factoring in unexpected costs or growth plans ensures your business remains resilient in the early stages.

Careful budgeting across all these areas—registration, equipment, marketing, and operations—sets a strong foundation for your business and helps you invest strategically in growth.

Small Business Grants in Canada

Grants are one of the most attractive ways to fund a startup because they don’t need to be repaid. However, they often come with specific eligibility requirements, including your business sector, location, and ownership structure. Many grants also require a detailed business plan, financial projections, and clearly defined objectives to demonstrate how the funds will be used effectively.

Canada offers a variety of grants at both the federal and provincial levels. Federal programs, such as those listed on Innovation Canada, provide support for research, technology adoption, and growth initiatives. Provinces often have their own programs, incubators, and industry associations that provide targeted funding for local businesses. Taking the time to research and apply for the grants relevant to your business can give you a financial boost without adding debt to your balance sheet.

Small Business Loans in Canada

While grants are ideal, loans are often the backbone of small business funding, providing the capital you need to get started or expand. Banks and traditional lenders require documentation such as a solid business plan, financial statements, and a good credit history. To improve your chances of approval, show realistic financial projections, demonstrate your ability to repay, and highlight any early signs of profitability.

Canada has several options for small business loans, including government-backed loans like the BDC Start-Up Loan and financial institutions offering small business products. These loans are generally more structured than alternative funding and often offer lower interest rates, making them a reliable option for businesses that meet the lender’s requirements.

Alternative Lenders to Support Your Small Business

For entrepreneurs who need faster, more flexible access to capital, alternative lenders have become a popular choice. These include online lenders, peer-to-peer lending platforms, and microloans offered through local development agencies. These funding sources often approve applications more quickly and offer flexible repayment terms, but they may come with higher interest rates than traditional loans.

Alternative financing is particularly useful for businesses with a proven track record but less access to traditional credit. If your business has been operating for at least six months and generates revenue above $10,000, you may be eligible for Merchant Growth term financing, which offers a streamlined application process tailored for small businesses ready to scale. Applying for funding through Merchant Growth can help you invest in growth initiatives, hire staff, or expand your operations with confidence.

Starting a small business in Canada requires more than just a great idea—it takes careful planning, compliance, and smart financial decisions. By exploring grants, traditional loans, and alternative financing options, you can find the funding that fits your business needs. Combining these resources with a clear plan, organized budgeting, and the right support can set you on the path to building a thriving business.

Ready to get started? Check out our free How to Start a Business Checklist ➡️ Download Here today.