Understanding Personal Guarantees in Business Loans

Signing a business loan can feel like a major milestone. It often represents growth, expansion, or the next phase of your company’s journey. But that confidence can shift quickly when you’re asked to personally guarantee the loan. For many business owners, the reaction is immediate: “I incorporated to protect myself, why am I personally liable?”

A personal guarantee changes the equation. It connects your personal finances to your business debt, even if your company is structured as a corporation. And while this is common in Canadian small business financing, it’s not always fully understood before documents are signed.

This guide explains what a personal guarantee is, why lenders require one, how it works in practice, and what risks and protections you should consider before agreeing to it. The goal isn’t to create fear; it’s to provide clarity.

Key Takeaways

- A personal guarantee makes you personally liable if your business defaults on its debt.

- Incorporation does not protect you once a personal guarantee is signed.

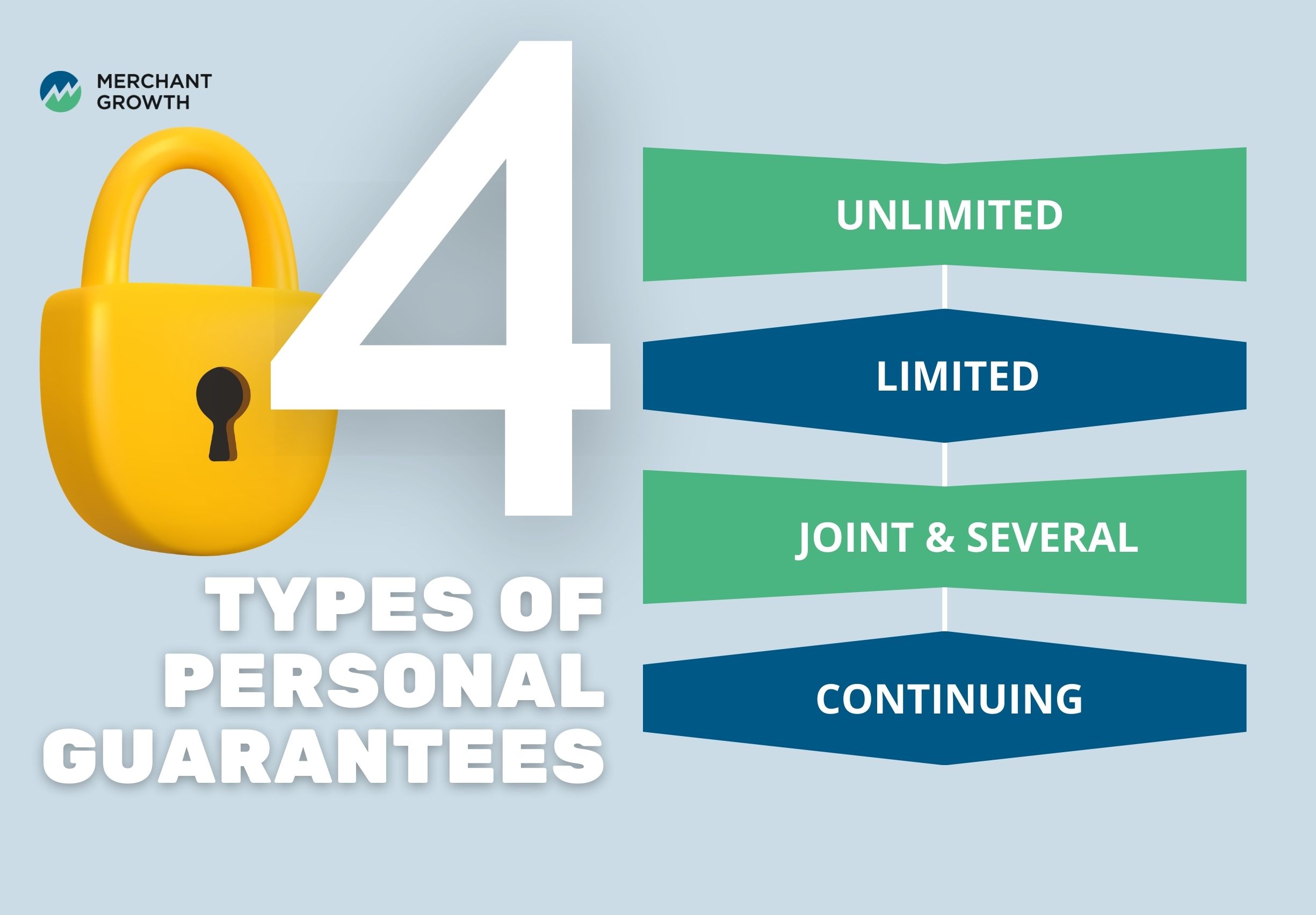

- Guarantees can be limited, unlimited, joint, or continuing.

- They may survive corporate bankruptcy.

- Not all business loans require one, but many do.

- Understanding the scope and terms before signing is critical.

What Is a Personal Guarantee?

A personal guarantee is a legally binding promise that makes an individual responsible for repaying a business debt if the company cannot. In simple terms, it means that if your business fails to meet its financial obligations, the lender can pursue you personally for repayment.

This is not symbolic language or a procedural formality. A personal guarantee is an enforceable contract. When you sign it, you are stepping outside the corporate shield and accepting individual responsibility.

It’s important to understand the distinction between the borrower and the guarantor. The corporation is the borrower; it receives the funds and operates the business. The individual who signs the personal guarantee becomes the guarantor, the party legally responsible if the borrower defaults. That distinction is what creates the risk exposure.

Why Lenders Ask for Personal Guarantees

From a lender’s perspective, small businesses can present a higher risk than large, established corporations. Many early-stage or growing businesses have limited assets, shorter operating histories, or inconsistent revenue patterns. A personal guarantee helps offset that risk.

By requiring the business owner to personally guarantee repayment, the lender aligns accountability with borrowing. It signals commitment and reduces the likelihood of strategic default. In many cases, it is a standard condition for approving small business loans, leases, equipment financing, and credit facilities.

Business owners often ask, “Do all business loans require a personal guarantee?” The answer is no, but many do, especially for smaller companies without substantial collateral. Requirements vary depending on the lender, loan size, structure, and overall risk profile.

How a Personal Guarantee Overrides Limited Liability

One of the primary benefits of incorporation is limited liability. A corporation is a separate legal entity, meaning its debts are generally distinct from the personal finances of its shareholders or directors.

However, when you sign a personal guarantee, you voluntarily override that protection. You are effectively reconnecting personal assets to corporate obligations. Incorporation does not shield you from liabilities you have personally agreed to assume.

This is where many business owners are caught off guard. The protection of incorporation remains intact for other business liabilities, but the specific debt covered by the guarantee becomes personally enforceable. Understanding that distinction before signing is critical.

Types of Personal Guarantees

Not all personal guarantees are structured the same way, and the differences can significantly affect your level of personal risk. Many business owners assume a guarantee is a standard, one-size-fits-all clause. In reality, the scope of liability depends entirely on how the agreement is written. The financial exposure, duration, and enforcement rights can vary meaningfully from one contract to another.

Before signing any personal guarantee on a business loan, it’s important to understand exactly what you are agreeing to. The wording in the agreement determines whether your liability is capped, shared, ongoing, or unlimited. A careful review of structure is just as important as reviewing the loan amount itself.

Here are the most common types of personal guarantees.

Unlimited Personal Guarantee

An unlimited personal guarantee means the guarantor is responsible for the full outstanding balance of the debt, plus potential interest, fees, and legal costs. There is no financial cap limiting liability. If the business defaults, the lender may pursue repayment for the entire amount owed.

This structure provides the lender with maximum protection and is common in smaller or higher-risk loans. For the guarantor, however, it represents the broadest potential exposure. Understanding the full scope of liability under an unlimited guarantee is essential before signing.

Limited Personal Guarantee

A limited personal guarantee places a cap on liability, either as a fixed dollar amount or a percentage of the debt. This structure creates clearer financial boundaries and can reduce personal exposure.

Limited guarantees are sometimes negotiated when multiple partners are involved or when the business has a stronger financial footing. While they still create personal liability, they offer more predictability around maximum risk.

Joint and Several Guarantees

When multiple individuals sign a guarantee, they may be jointly and severally liable. This means each guarantor can be held responsible for the entire debt, not just their share. The lender has the right to pursue any one of the guarantors for full repayment, regardless of internal ownership splits.

This structure is common when multiple shareholders or directors are involved. It’s important for each guarantor to understand that their personal exposure may extend beyond what they consider their “portion” of the business.

Continuing Guarantee

A continuing guarantee extends beyond a single loan and may apply to future credit advances until formally revoked. This means the guarantee can remain active even as new borrowing occurs under the same credit facility.

Without careful review, business owners may not realize that their obligation remains in effect across multiple transactions. Continuing guarantees are particularly important to examine when dealing with revolving credit lines or long-term financing relationships.

What Happens If the Business Defaults?

If a business misses payments and enters default, lenders typically begin by pursuing the company itself. They may attempt to recover funds through corporate assets, secured collateral, or negotiated repayment plans.

If those efforts are insufficient, the lender may then pursue the guarantor personally. This can include seeking legal judgments, enforcing collection actions, or pursuing personal assets, depending on the agreement.

Business bankruptcy and personal guarantees are often misunderstood. Filing for corporate bankruptcy does not automatically eliminate personal liability under a signed guarantee. The corporation may discharge its obligations, but the guarantor’s personal responsibility can remain enforceable.

This is why a bankruptcy personal guarantee scenario can become particularly complex. The guarantee exists independently of the corporate structure once it has been executed.

Credit Impact: What Business Owners Should Know

Many business owners ask whether a personal guarantee affects their credit score or appears on their credit report. In most cases, the guarantee itself does not immediately show up as a reported debt. It represents contingent liability, meaning it only becomes actionable if the business defaults.

However, if default occurs and the lender initiates collection or legal action, that activity can affect your personal credit. Court judgments, delinquent accounts, or settlements may appear in credit reporting systems.

Understanding this distinction helps clarify risk. A guarantee does not automatically damage your credit, but default and enforcement actions can.

How Personal Guarantees Apply to Common Canadian Financing

Personal guarantees appear across many financing products in Canada, but the way they are structured can vary significantly depending on the lender, the purpose of the funding, and the specific program rules. Some products rely heavily on personal guarantees as part of their risk management process, while others may have alternative structures or government backing that change how liability is handled.

Understanding how guarantees apply across different financing types helps business owners avoid assumptions. Just because one loan required a personal guarantee does not mean every product will be structured the same way.

Government-Backed Emergency Loans (e.g., CEBA)

Programs such as CEBA were created under specific federal guidelines and delivered through participating financial institutions. Because these loans were government-backed and designed as emergency support, their structure differed from conventional business loans. In many cases, they did not rely on personal guarantees in the traditional sense.

However, the exact terms depended on program rules and how the lending institution administered the funds. Business owners should always review the original agreement rather than assuming government support eliminates all personal exposure.

BDC Financing

BDC offers a range of financing products, and whether a personal guarantee is required depends on the structure of the loan, the borrower’s financial profile, and the available security. For early-stage or higher-risk financing, personal guarantees may be part of the approval framework. For more established businesses with strong assets or performance history, structures may differ.

The key takeaway is that BDC financing is not automatically personally guaranteed in every case. Requirements are assessed individually, and terms vary by product and risk level.

Business Credit Cards

Many small business credit cards require the primary applicant to personally guarantee repayment. Even though the account is issued in the name of the business, the individual cardholder is often ultimately responsible for outstanding balances if the company cannot pay.

This structure is common because credit cards are typically unsecured forms of financing. Without pledged collateral, lenders use personal guarantees to reduce risk. Business owners sometimes overlook this detail when applying, assuming the corporate name alone limits liability.

These examples illustrate that personal guarantees are common across Canadian financing products, but they are not universal or identical in structure. The specific agreement, not the product category, determines your personal exposure. Careful review of each financing contract ensures there are no surprises later.

Can You Get Out of a Personal Guarantee?

Once signed, a personal guarantee cannot simply be revoked at will. It is a binding contractual obligation. However, there are circumstances where liability may change.

In some cases, guarantees can be limited before signing through negotiation. After repayment of the loan, the guarantee is typically released. Refinancing with a different lender may also alter or replace the original obligation.

If you are unsure about your exposure, reviewing the agreement with legal counsel can provide clarity. It is far easier to negotiate terms before signing than to unwind them afterward.

The Real Risks to Personal Wealth

A personal guarantee may expose savings, real estate equity, investments, and in some cases, future income to enforcement actions if default occurs. The actual risk depends on the structure of the guarantee, the amount outstanding, and the lender’s enforcement approach.

This does not mean default is inevitable or that guarantees are inherently reckless. It means business owners should understand the scope of potential exposure. Risk awareness supports responsible decision-making.

A Responsible Approach to Personal Guarantees in Small Business Financing

Personal guarantees are common in small business lending, but how they are structured matters. Transparent communication, realistic repayment expectations, and disciplined underwriting reduce the likelihood of default.

Responsible financing should be clear about obligations, scope, and duration. When lenders assess cash flow carefully and structure repayment around sustainable performance, both parties benefit. Strong underwriting protects the lender while also protecting the borrower from overextension.

At Merchant Growth, financing decisions are built around real business performance and practical growth planning. The goal is not to impose unnecessary personal jeopardy, but to structure capital in a way that aligns with your company’s capacity and trajectory.

Before You Sign: A Practical Checklist

Before agreeing to a personal guarantee, it’s worth slowing down and reviewing the details carefully. These agreements are often presented as standard paperwork, but the fine print can meaningfully change your level of personal exposure. Taking a few extra minutes here can save you from confusion later and help you make a decision that fits your risk comfort level.

Here are the key questions to review before you sign:

- Is the guarantee limited or unlimited?

- Is there a financial cap?

- Does it apply to future advances?

- Is it joint and several with other guarantors?

- When does the obligation expire?

- Should legal counsel review the agreement?

Clarity at the outset reduces uncertainty later, especially if your business faces an unexpected slowdown or financing needs change over time. When you understand exactly what you’re signing, you can move forward with confidence, and avoid unpleasant surprises down the road.

From Understanding Personal Guarantees to Financing With Confidence

Most Canadian entrepreneurs will encounter a personal guarantee at some point in their business journey. The key is not avoiding them entirely, but understanding what they mean and how they work.

When you understand your obligations, review terms carefully, and align financing with realistic growth plans, personal guarantees become part of a structured risk-sharing framework rather than a hidden hazard.

Personal guarantees are serious commitments, but they don’t have to be confusing. If you’re considering business financing and want clarity before signing, speak with Merchant Growth about financing solutions designed for Canadian entrepreneurs who value transparency and sustainable growth.