Can Your Business Afford a Loan? Understanding Debt Service Coverage Ratio (DSCR)

When you’re thinking about taking on a loan, the first question usually isn’t about interest rates or repayment terms, it’s whether your business can realistically afford the debt in the first place. You might be generating steady revenue and managing day-to-day expenses, but that doesn’t always mean there’s enough room to comfortably take on additional financial obligations. This is where many business owners find themselves unsure of what their numbers are really telling them. Debt Service Coverage Ratio, or DSCR, helps bring clarity to that uncertainty.

DSCR is one of the most important financial metrics lenders use to evaluate whether a business can handle debt, but it’s just as valuable for business owners trying to make smarter financial decisions. Understanding DSCR gives you a clearer picture of your financial capacity, helping you move from guesswork to informed planning when it comes to borrowing.

What Is Debt Service Coverage Ratio (DSCR)?

At its core, the Debt Service Coverage Ratio measures how much income your business generates compared to the amount of debt it needs to repay. It’s a simple ratio that answers a very practical question: Do you have enough income to cover your loan payments?

The calculation compares your available income, typically referred to as net operating income, to your total debt obligations, which include both principal and interest payments. The result is a number that shows whether your business is covering its debt, just breaking even, or falling short.

For example, a DSCR of 1.0 means your income exactly matches your debt payments. Anything above that indicates a buffer, while anything below suggests your business may struggle to meet its obligations. With that foundation in place, it becomes easier to understand how this ratio is used in real-world decision-making.

What Does DSCR Tell You?

While the formula itself is straightforward, the insight it provides is much more meaningful. DSCR offers a quick way to assess financial health and risk without needing to analyze every detail of your financial statements.

From a lender’s perspective, DSCR helps determine whether a borrower is likely to repay a loan reliably. A higher ratio suggests a stronger ability to absorb unexpected changes, while a lower ratio signals potential risk. For business owners, it provides a practical way to evaluate whether taking on new debt aligns with current income.

More importantly, DSCR highlights how much flexibility your business has. It shows not just whether you can cover your debt today, but how much room you have if conditions change, which makes it a useful tool for both short-term decisions and long-term planning.

Debt Service Coverage Ratio Formula

The formula for DSCR is relatively simple, but understanding what goes into each part is key to using it effectively.

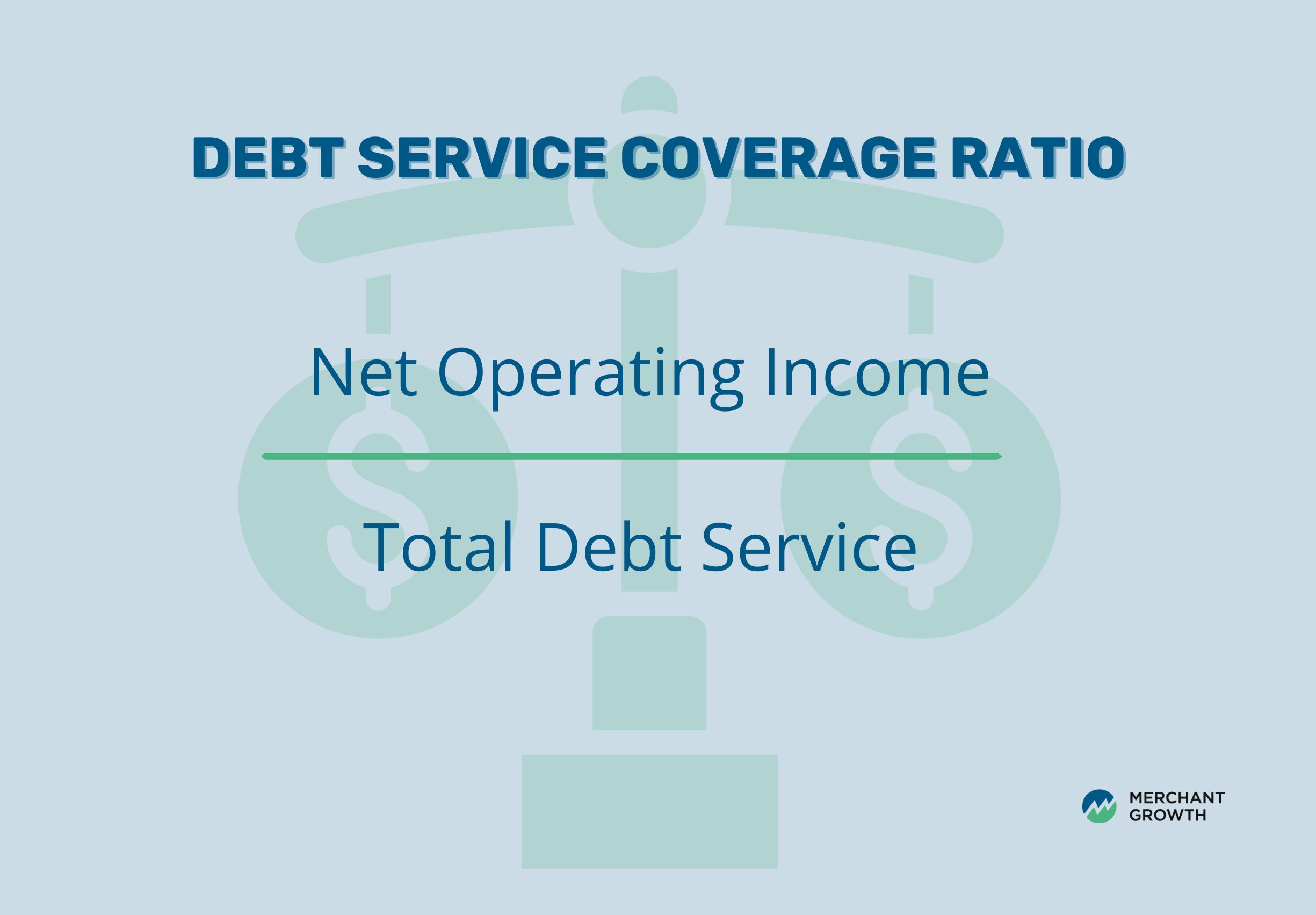

DSCR = Net Operating Income ÷ Total Debt Service

Net Operating Income

Net operating income represents the income your business generates after operating expenses but before debt payments. This is the portion of your cash flow that’s available to cover your financial obligations.

Total Debt Service

Total debt service includes all required loan payments over a given period, typically combining both principal and interest. This may include multiple loans if your business has more than one outstanding obligation.

By comparing these two figures, DSCR shows how comfortably your business can meet its debt commitments. Once you understand the formula, applying it becomes much more straightforward.

How to Calculate DSCR (Step-by-Step)

Calculating DSCR does not require complicated tools, but it does require accurate numbers and a clear process. Breaking it into steps makes it easier to understand and helps ensure your calculation reflects your business’s actual financial position.

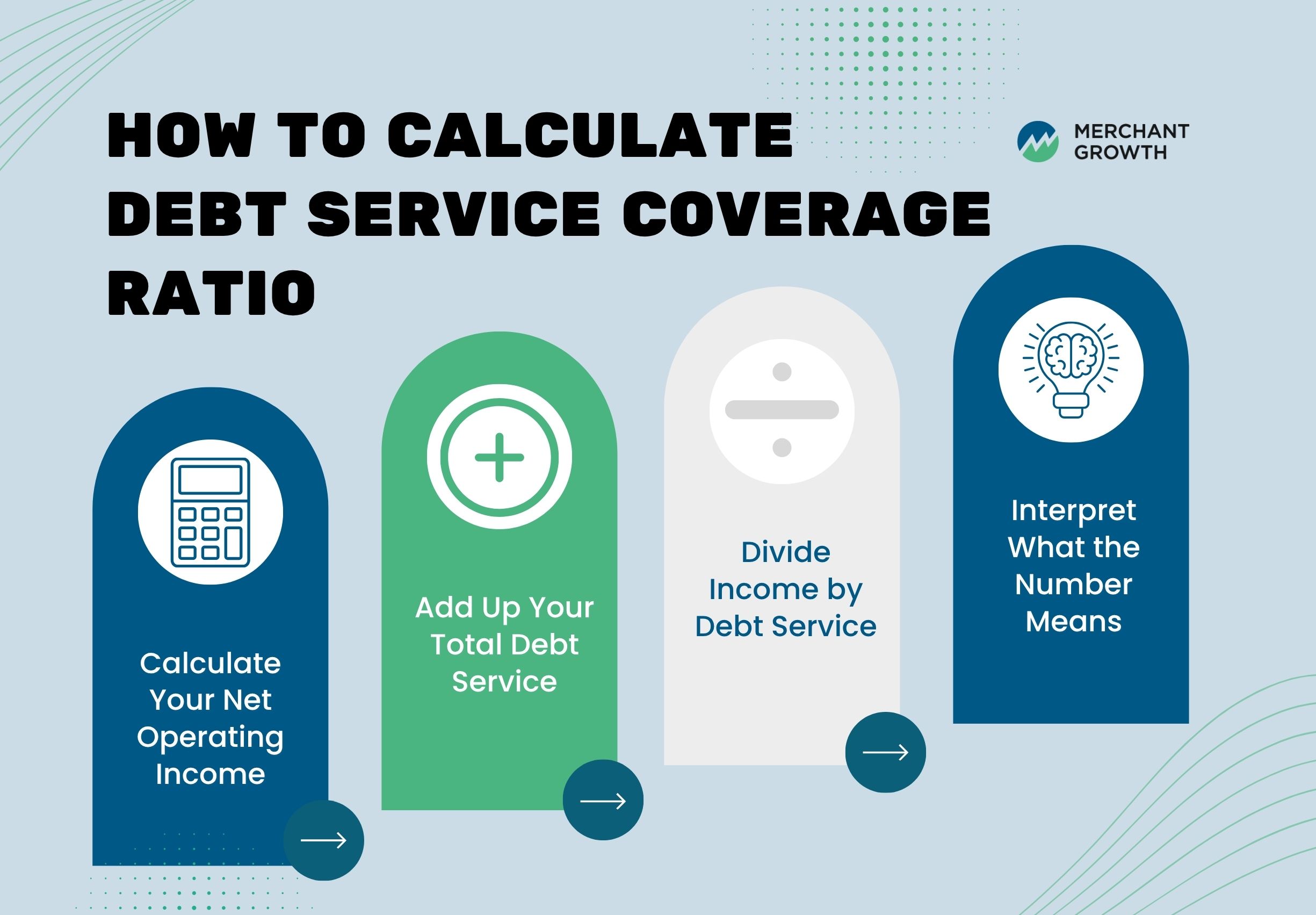

Step 1: Calculate Your Net Operating Income

Start by determining how much income your business generates after operating expenses. This usually means taking your total revenue and subtracting costs such as rent, payroll, utilities, software, etc. The goal is to isolate the income that is available to cover debt payments, rather than the total amount your business brings in before expenses.

This step matters because DSCR is meant to reflect repayment capacity, not just top-line revenue. A business may generate strong sales, but if operating expenses are high, the amount left over to service debt may be much smaller than expected. Using a realistic operating income figure makes the rest of the calculation much more meaningful.

Step 2: Add Up Your Total Debt Service

Next, calculate the total amount your business is required to pay toward debt over the same period. This includes both principal and interest payments and should capture all existing loan obligations, not just the most obvious or largest one. If you are calculating DSCR annually, make sure your debt service total also reflects annual payments.

This part of the formula is just as important as the income side because missing a debt payment can distort the ratio. For example, leaving out a smaller equipment loan or line of credit payment may make your DSCR appear healthier than it actually is. A complete view of your obligations gives you a more accurate picture of your borrowing capacity.

Step 3: Divide Income by Debt Service

Once you have both numbers, divide your net operating income by your total debt service. The result is your DSCR. This tells you how much income your business generates for every dollar of debt it must repay.

Step 4: Interpret What the Number Means

The final step is understanding what your DSCR is telling you in the context of your business. Rather than focusing only on whether the number is “good” or “bad,” it’s more useful to look at what it reveals about your financial flexibility and risk.

Start by asking how much room your business has to handle change. If your income were to drop or expenses were to increase, would your current DSCR still support your debt payments? Looking at your ratio this way helps you understand how resilient your business is, not just whether it works on paper.

It’s also important to consider how stable your DSCR is over time. A consistent ratio suggests predictable performance, while large fluctuations may indicate underlying cash flow challenges. When you view DSCR as part of a broader pattern rather than a single number, it becomes a much more practical tool for decision-making.

DSCR Example

Understanding the formula is one thing, but seeing how DSCR plays out in a real scenario makes it easier to apply. Instead of just calculating the ratio, it’s helpful to look at how small changes in your numbers can affect the outcome.

Consider a business with a net operating income of $120,000 and total annual debt payments of $100,000. In this case, the DSCR is 1.2, meaning the business generates 20% more income than required to cover its debt. On the surface, this looks stable, but it’s important to understand how sensitive that margin can be.

For example, if expenses increase slightly and reduce income to $110,000, the DSCR drops to 1.1. If revenue dips further, the ratio can quickly approach 1.0, leaving very little room for error. This is why DSCR is not just about hitting a number; it’s about understanding how stable your finances are under different conditions.

What Is a Good Debt Service Coverage Ratio?

There’s no single “perfect” DSCR, but there is a practical way to think about what makes a ratio strong or risky. Instead of focusing only on benchmarks, it’s more useful to understand what different ranges mean for your business in real terms.

- A DSCR below 1.0 means your business is not generating enough income to cover its debt, which often signals immediate financial pressure.

- A DSCR around 1.0 means you are covering your obligations, but with no flexibility if anything changes.

- A DSCR between 1.2 and 1.5 generally indicates a reasonable buffer, which is why many lenders use this range as a minimum requirement.

- A DSCR above 1.5 suggests a stronger financial position, with more room to handle fluctuations or take on additional opportunities.

What matters most is not just where your DSCR falls, but how stable it is over time. A business with a consistent DSCR of 1.3 may be in a better position than one that fluctuates between 1.0 and 1.6. Lenders and business owners alike look for consistency because it signals reliability.

Why DSCR Matters for Loans and Financing

When applying for financing, DSCR is one of the primary metrics lenders use to evaluate your application. It helps determine whether your business qualifies for a loan and influences the terms you may be offered.

A stronger DSCR can improve your chances of approval, increase your borrowing limit, and lead to more favourable interest rates. Conversely, a lower DSCR may result in stricter conditions or reduced access to capital.

For Canadian small businesses, this is particularly important, as lenders often prioritize stable cash flow. Understanding how DSCR impacts these decisions allows you to approach financing with greater confidence and preparation.

How Business Owners Can Use DSCR

Once you understand your DSCR, it becomes easier to pressure-test your decisions before committing to them. Instead of relying on assumptions, you can use your numbers to see how new debt might impact your business in real terms.

For example, before committing to a loan, you can calculate how it will affect your DSCR and determine whether your business can comfortably support the additional payments. This helps reduce the risk of overextending your finances.

It can also be used to assess growth opportunities, such as hiring, expanding operations, or investing in equipment. By understanding how these decisions impact your ratio, you can move forward with greater clarity and confidence.

How to Improve Your Debt Service Coverage Ratio

If your DSCR isn’t where you’d like it to be, there are several ways to strengthen it over time. Because the ratio is influenced by both income and debt obligations, improvements can come from either side of the equation.

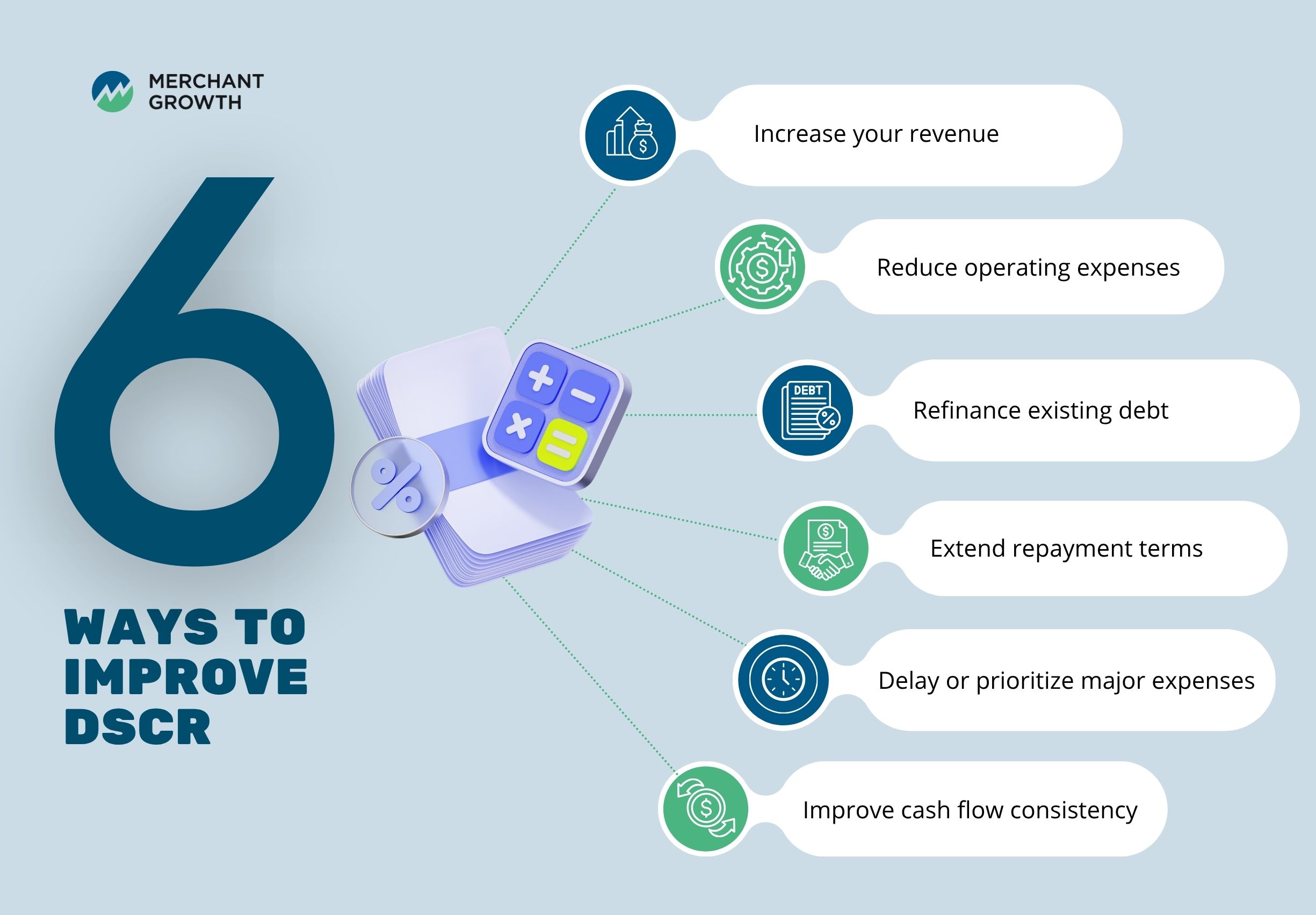

Here are some of the most effective strategies:

Increase your revenue

Growing your revenue directly improves your DSCR by increasing the income available to cover debt payments. This might involve expanding your customer base, adjusting pricing, or introducing new offerings. Even gradual increases can make a noticeable difference over time.

Reduce operating expenses

Lowering your expenses improves your net operating income, which strengthens your ratio. This could include cutting unnecessary costs or improving efficiency in your operations. Small savings can add up and have a meaningful impact on your financial position.

Refinance or restructure existing debt

Adjusting your loan terms can reduce your total debt service. Refinancing at a lower rate or consolidating payments can make your obligations more manageable. This approach can improve your DSCR without requiring changes to your revenue.

Extend repayment terms

Lengthening repayment periods reduces your regular payment amounts, improving your short-term cash flow. While it may increase total interest paid, it can help stabilize your finances and improve your DSCR in the near term.

Delay or prioritize major expenses

Timing large purchases carefully can help preserve your cash flow. Delaying non-essential expenses or prioritizing those that generate revenue can strengthen your financial position. This helps maintain a healthier balance between income and obligations.

Improve cash flow consistency

More predictable cash flow makes it easier to manage debt payments. This can involve improving invoicing processes, tightening payment terms, or encouraging faster customer payments. Stability in your income helps support a stronger DSCR over time.

Improving your DSCR is less about one major change and more about consistently strengthening your financial position. As these improvements take effect, your ratio becomes a more reliable indicator of your ability to manage debt.

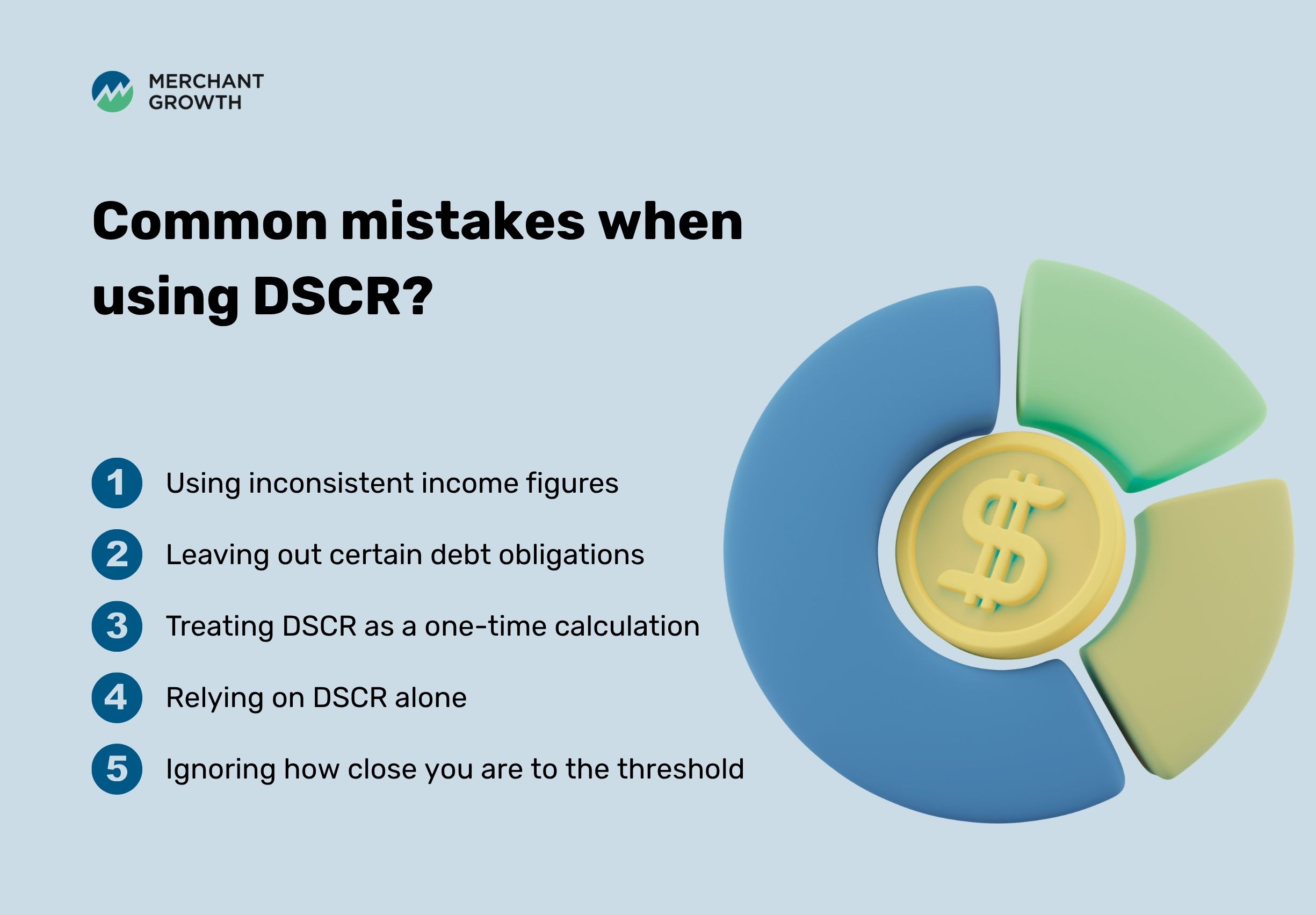

Common Mistakes When Using DSCR

Even though DSCR is straightforward to calculate, small mistakes can lead to inaccurate conclusions. Being aware of these pitfalls helps ensure your ratio reflects your true financial situation.

Here are some common mistakes to avoid:

Using inconsistent or inaccurate income figures

If your income is based on rough estimates or inconsistent reporting periods, your DSCR may not reflect reality. For example, mixing monthly and annual figures or relying on unusually strong months can distort your results. Using consistent, up-to-date financial data ensures your ratio is both accurate and comparable, giving you a clearer picture of your actual repayment capacity.

Leaving out certain debt obligations

All loan payments should be included in your calculation, not just your primary or most visible debt. Smaller obligations like equipment financing, lines of credit, or secondary loans can still impact your ability to manage payments. Missing even one of these can make your DSCR appear stronger than it actually is, which may lead to overestimating how much debt your business can realistically handle.

Treating DSCR as a one-time calculation

Your business is constantly changing, which means your DSCR should be updated regularly to reflect those changes. Revenue can fluctuate, expenses can shift, and new obligations may arise, all of which affect your ratio. Relying on a single calculation over time can create a false sense of stability and lead to decisions based on outdated information.

Relying on DSCR alone

DSCR is a useful metric, but it doesn’t capture every aspect of your financial health. It doesn’t reflect factors like market conditions, customer concentration, or operational risks that can also impact your ability to repay debt. Using DSCR alongside other tools, such as cash flow forecasts or budgeting, gives you a more complete and reliable understanding of your financial position.

Ignoring how close you are to the threshold

A DSCR just above 1.0 may technically indicate that you can cover your debt, but it leaves very little room for error. Even small changes in revenue or unexpected expenses can push your ratio below that level. Understanding how much buffer you have, and how quickly it could change, helps you better manage risk and make more cautious financial decisions.

Recognizing these challenges helps you use DSCR more effectively. With that awareness, it becomes easier to understand where the metric is most useful and where it has limitations.

Limitations of Debt Service Coverage Ratio

While DSCR is a valuable tool, it does not provide a complete view of your financial health. Understanding its limitations helps you use it more effectively as part of a broader strategy.

Here are some key limitations:

It reflects a single point in time

DSCR is based on current or projected numbers, which means it captures a snapshot of your finances rather than a long-term view. While this can be useful for assessing your position today, it doesn’t automatically account for future changes in revenue or expenses. Regularly recalculating your DSCR helps ensure it stays relevant as your business evolves.

It doesn’t account for market conditions

External factors like economic shifts, industry trends, or changes in customer demand are not reflected in the ratio. Even if your DSCR looks strong, these outside influences can still impact your ability to generate income and repay debt. This is why it’s important to consider the broader business environment alongside your financial metrics.

It assumes stable cash flow

DSCR works best when income is relatively consistent, but many businesses experience fluctuations throughout the year. Seasonal trends, project-based work, or delayed payments can all affect cash flow in ways the ratio doesn’t fully capture. Looking at your cash flow patterns alongside your DSCR provides a more realistic view of your financial stability

It excludes unexpected expenses

Unplanned costs, such as equipment repairs, supplier changes, or sudden increases in operating expenses, are not included in DSCR calculations. These events can reduce the cash available for debt payments, even if your ratio appears healthy. Building a contingency buffer into your finances can help offset this limitation and reduce risk.

It should not be used in isolation

DSCR is a helpful indicator, but it is only one part of your overall financial picture. It doesn’t replace tools like budgeting, cash flow forecasting, or profitability analysis, all of which provide additional insight into your business. Using multiple metrics together allows you to make more informed and balanced financial decisions.

Understanding these limitations strengthens how you use DSCR. When combined with other insights, it becomes a more reliable tool for planning your next steps.

Using DSCR to Plan Your Next Financial Move

Once you understand your DSCR, it becomes a practical tool for planning ahead. It allows you to evaluate different scenarios and understand how changes in your finances could impact your ability to manage debt.

This forward-looking approach helps you make more confident decisions about borrowing, investing, or scaling your business. Instead of relying on assumptions, you’re working with a clearer understanding of your financial capacity.

How Merchant Growth Can Support Your Financing Goals

Understanding your DSCR is an important step in preparing for financing, but it’s not the only factor that determines your options. Many traditional lenders rely on strict requirements, which can limit access for some businesses.

Merchant Growth offers flexible funding solutions designed to help Canadian small businesses manage cash flow and invest in growth. With faster access to capital and fewer barriers than traditional lending, it provides an alternative path for businesses looking to move forward.

By combining a clear understanding of your financial metrics with the right funding partner, you can make more confident decisions and position your business for long-term success.