What is Leasing & Why More Businesses Are Choosing It to Improve Cash Flow

Leasing has evolved from a simple affordability tactic into a strategic financial tool for businesses of all sizes. Whether you’re outfitting an office, upgrading equipment, or adding vehicles to your fleet, leasing provides much more than just cost savings. It offers flexibility, preserved cash flow, and the ability to scale faster—all without the upfront burden of large capital investments.

In fact, leasing is becoming a go-to option for many Canadian business owners: according to Equipment Financing Canada, the 2024 market is shaped by several key trends, including a rising reliance on flexible financing solutions, increasing demand for sustainable equipment, and the ongoing impact of technological innovation. In today’s fast-moving economy, more Canadian businesses are choosing leasing to remain agile, competitive, and financially resilient. Let’s explore why.

Key Takeaways

- What leasing is and how it works for small businesses

- The three main types of leasing arrangements

- How leasing can fuel business growth while maintaining strong cash flow

- Whether leasing is the right financial decision for your business

What is Leasing in Business?

Leasing is a financial arrangement that allows businesses to access and use essential equipment, vehicles, or property without owning them outright. Instead of purchasing the asset, the business (known as the lessee) agrees to pay a fixed monthly fee to the lessor—the leasing company or lender that owns the asset—over a set term.

This model is especially beneficial for small businesses looking to preserve working capital while still acquiring the tools needed for growth. Leasing can apply to a wide range of assets, including office furniture, medical or construction equipment, software, commercial vehicles, and more.

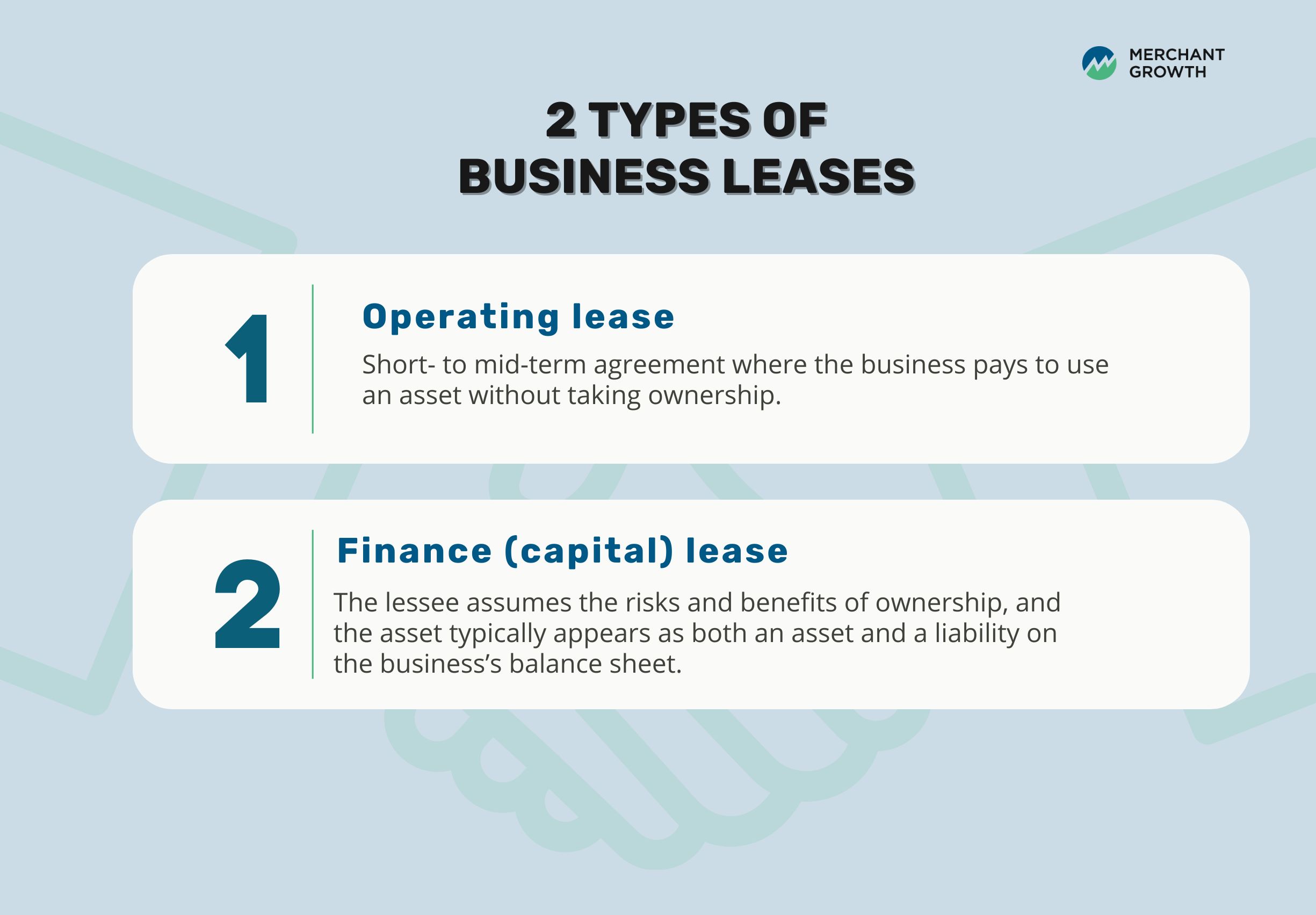

The Two Main Types of Leasing

Choosing the right leasing structure can make a significant difference in how your business manages cash flow, accesses equipment, and plans for the future. Whether you're a start-up looking to preserve capital or an established business planning to scale, understanding the different types of leases is key to selecting an option that fits your operational and financial needs.

Operating lease

An operating lease is typically a short- to mid-term agreement where the business pays to use an asset without taking ownership. The asset remains on the lessor’s balance sheet, and lease payments are treated as operating expenses, often fully deductible. This type of lease is commonly used for assets that depreciate quickly or require frequent upgrades, such as office equipment, technology, or vehicles.

Best for: Businesses that need flexibility or regularly upgrade equipment.

Finance lease (capital lease)

A finance lease—also known as a capital lease—is structured more like a purchase. The lessee assumes the risks and benefits of ownership, and the asset typically appears as both an asset and a liability on the business’s balance sheet. Finance leases often include a buyout option at the end of the term, making them ideal for businesses that intend to retain the equipment long-term.

Best for: Businesses that plan to keep the asset long-term and want the benefits of ownership without a large upfront payment.

Breaking Down the Components of a Lease

Lease agreements can be intimidating, especially if you’re not familiar with the terminology or how the numbers are calculated. If you've ever wondered what exactly you're paying for, how lease payments are structured, or what happens at the end of your lease, you're not alone. Many business owners hesitate to lease because the details feel murky or overly technical.

But understanding just a few key components can make a big difference. By breaking down the most important elements of a lease—like how costs are calculated, what fees to expect, and how asset value plays a role—you’ll be in a much stronger position to evaluate your options and make decisions that support your business and your cash flow. Let’s take a closer look at what really goes into a lease.

The capitalized cost

Also known as the “cap cost,” this is the total amount being financed through the lease. It typically includes the negotiated price of the asset, plus any additional fees, delivery costs, or taxes rolled into the lease. The higher the capitalized cost, the higher your monthly payment will be.

Example: A small dental clinic leases a new digital imaging machine with a negotiated price of $45,000. Delivery and installation add another $2,000, bringing the capitalized cost to $47,000. This full amount is used to calculate the monthly lease payment.

The lease term

This refers to the length of time you’ll be making lease payments, usually ranging from 12 to 60 months. Shorter lease terms typically mean higher monthly payments but offer more flexibility to upgrade sooner, while longer terms reduce monthly costs but lock you in for a longer period.

Example: A catering company leases a commercial-grade oven. They choose a 36-month term to keep payments manageable while ensuring they’ll have the option to upgrade when technology or capacity needs change.

The residual value

Residual value is the estimated worth of the leased asset at the end of the lease term. It plays a critical role in determining your monthly payments—the higher the residual value, the lower your payments. It also affects your buyout cost if you decide to purchase the asset when the lease ends.

Example: A small architecture firm leases a high-end plotter with a residual value of $10,000 after a 48-month lease. This reduces the amount being amortized over the lease term and gives them the option to purchase it affordably later.

The disposition fee

This is a fee some lessors charge at the end of the lease to cover costs like inspection, cleaning, and preparing the asset for resale. It’s typically non-negotiable and can range from a few hundred to over a thousand dollars.

Example: A logistics company returns three leased delivery vans at the end of a 3-year lease. They’re charged a $750 disposition fee per vehicle to cover inspection and preparation for auction.

Depreciation

Depreciation is the loss in value of the asset over time. In most leases, you’re essentially paying for the portion of the asset’s life you’re using. Depreciation is factored into your monthly payments and varies based on asset type and usage.

Example: A tech startup leases laptops for its developers. The devices are expected to depreciate by 50% over two years. Their lease payments are structured to cover that loss in value, with the option to upgrade when the term ends.

Misconceptions We Often Hear About Leasing for Your Business

Leasing is often misunderstood as a financial last resort or a backup plan for businesses that can’t afford to buy outright, but that couldn’t be further from the truth. In reality, leasing is a widely used and strategic financial tool embraced by companies of all sizes, from lean start-ups to large-scale enterprises.

Yet, many business owners hesitate to explore leasing because of outdated assumptions or unclear information. Let’s take a moment to debunk some of the most common myths and shed light on what leasing really offers in today’s business environment.

Myth: Leasing is more expensive in the long run.

Fact: While monthly payments may add up over time, leasing can be cheaper when you account for cash flow preservation, tax deductions, and lower maintenance costs.

Myth: Leasing is only for businesses that can’t afford to buy.

Fact: Leasing is a strategic choice used by successful businesses to keep capital free for growth and operations.

Myth: Leased equipment is outdated.

Fact: Many leasing programs give access to the newest models or let you upgrade regularly.

Myth: Leasing contracts are rigid.

Fact: Lease terms can be customized—short-term, seasonal, or tailored to cash flow cycles.

Myth: Leasing means you’ll never own the equipment.

Fact: Many leases include end-of-term buyout options, giving you flexibility.

How Leasing Can Support Your Cash Flow

For many businesses, managing cash flow is a constant balancing act—ensuring there’s enough capital to cover day-to-day expenses while also funding growth and staying ahead of the competition. That’s where leasing can offer significant advantages. Beyond simply acquiring the tools or equipment you need, leasing can be a powerful tool for protecting liquidity, improving predictability, and allowing your business to operate with greater confidence.

Here are a few of the most impactful ways leasing can support your cash flow:

Preserves capital

Rather than spending a large lump sum to purchase equipment outright, leasing spreads costs over time, keeping your cash reserves intact. This allows businesses to stay nimble and redirect funds toward higher-return activities like hiring, marketing, or product development.

Predictable monthly payments

Leasing agreements typically involve fixed monthly payments, which makes it easier to plan, forecast, and manage budgets with less financial volatility. This kind of stability is especially helpful for businesses with tight margins or fluctuating revenues.

Frees up cash for growth or operations

Because leasing limits large capital expenditures, businesses can reallocate their available cash toward immediate operational needs or expansion initiatives. Whether you're launching a new product, entering a new market, or hiring talent, having cash on hand creates strategic flexibility.

Avoids equipment obsolescence

Technology and equipment evolve quickly, and owning assets outright often means holding onto outdated tools longer than you should. Leasing gives businesses the ability to refresh and upgrade regularly, without the full burden of replacement costs, keeping operations efficient and competitive.

Utilize Equipment Leasing as a Tool to Grow Your Business

Leasing isn't just about keeping the lights on—it’s about fueling growth without overextending your business financially. For companies ready to expand, take on larger contracts, or enter new markets, leasing can provide the freedom to act quickly and confidently. By removing the need for major upfront capital, leasing helps business owners move forward on their own timeline, without compromising cash flow or delaying key initiatives.

Here’s how leasing empowers strategic, scalable growth:

Supports expansion without cash drain

Whether you're opening a new location or ramping up production, growth often comes with the need for new equipment, and that can get expensive. Leasing lets you access the tools, vehicles, or technology you need without putting a strain on your cash reserves. It’s a practical way to scale sustainably, giving you the resources to grow while maintaining a strong financial foundation.

Example: A landscaping business lands a citywide maintenance contract and leases additional lawnmowers and trucks to scale up quickly, without tying up capital needed for staffing and supplies.

Allows faster execution on opportunities

Opportunities don’t always wait for your bank balance to catch up. Leasing gives you the power to act when the timing is right. Whether it’s onboarding a new client, upgrading outdated equipment, or preparing for a busy season, with leasing, you can move fast without financial hesitation.

Example: A printing company secures a high-volume contract but needs additional machines to meet demand. Instead of dipping into reserves, they lease the equipment and start production immediately.

Simplifies forecasting

One of the biggest advantages of leasing is predictability. Fixed monthly payments make it easier to build reliable cash flow forecasts and long-term budgets. This consistency helps with planning, investor reporting, and reducing surprises that can derail growth strategies.

Example: A medical clinic leasing diagnostic equipment knows exactly what their monthly costs will be for the next three years, making it easier to budget for hiring and expansion.

Get to Know the Potential Tax Benefits of Leasing

Leasing doesn’t just help with cash flow—it can also offer meaningful tax advantages for Canadian businesses. In many cases, lease payments are fully deductible as business expenses. This means the total lease cost can be subtracted from your gross income when calculating taxable income, lowering your overall tax burden.

Depending on the type of lease and how it’s structured, leasing may also qualify as an off-balance-sheet transaction, particularly in the case of operating leases. This means the leased asset and its corresponding liability don’t appear on your balance sheet, which can improve your debt-to-equity ratio and make your business appear less leveraged to potential investors or lenders.

According to the Canada Revenue Agency (CRA), leasing costs may be deductible if they are reasonable and incurred to earn business income. Generally, operating lease payments for assets used in a business are deductible, though certain limitations—such as those related to passenger vehicles—may apply. To be fully deductible, the expense must relate to business use and comply with CRA rules.

Keep in mind that tax treatment can vary based on province, lease structure, and the nature of the asset, so it’s always best to consult a tax professional or accountant for personalized advice.

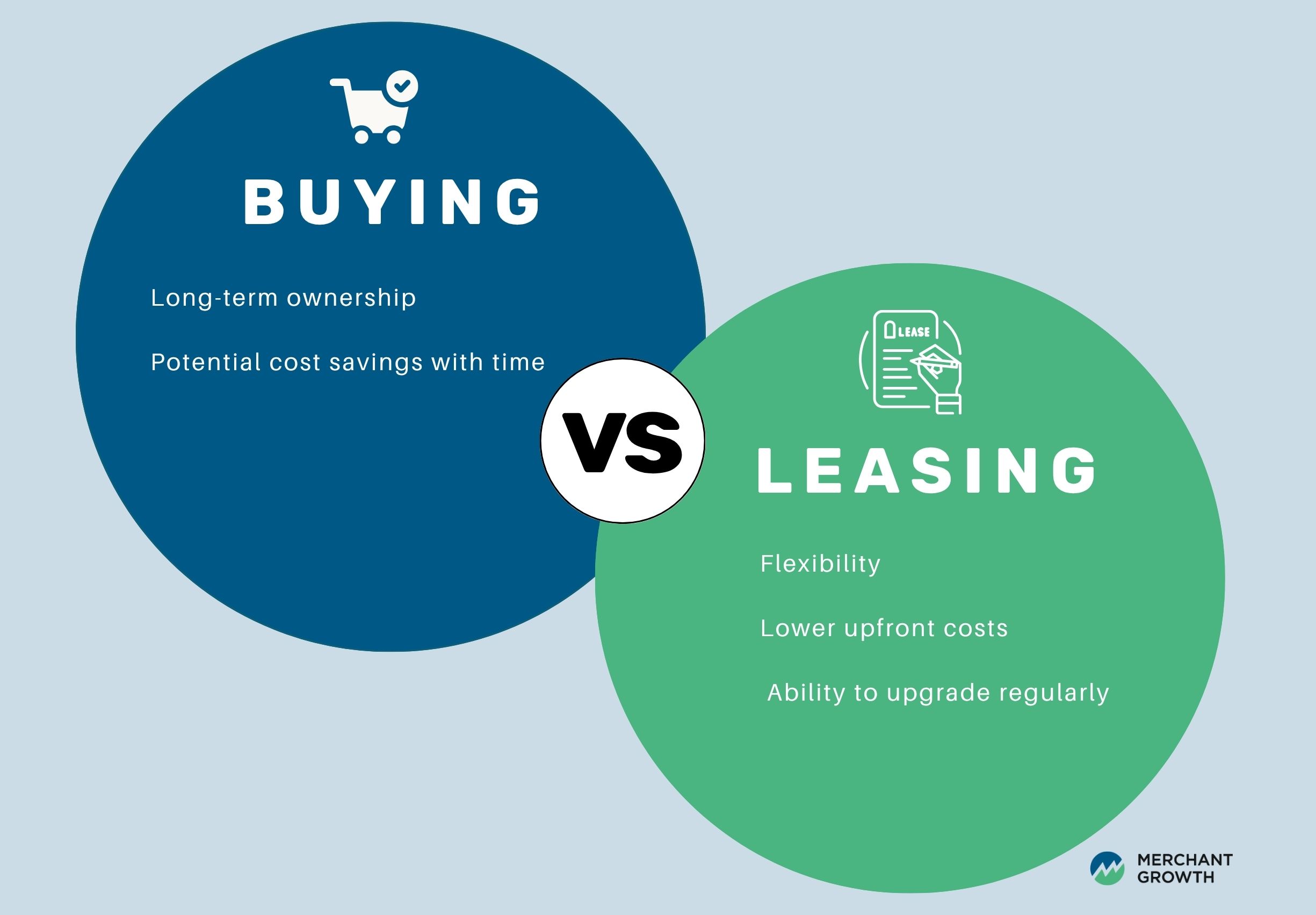

Equipment Leasing vs. Buying: Which is Right for Your Business?

Both leasing and buying have their advantages—it all depends on your business’s financial goals, cash flow situation, and how you plan to use the asset. Leasing offers flexibility, lower upfront costs, and the ability to upgrade regularly, while buying provides long-term ownership and potential cost savings over time. Understanding the pros and cons of each option can help you make a decision that aligns with your current needs and future plans.

Here’s how the two approaches stack up:

| Leasing | Buying | |

|---|---|---|

| Upfront Cost | Low | High |

| Monthly Cost | Fixed payments | No payments after purchase |

| Ownership | No (unless buyout) | Yes |

| Maintenance | Often included | Owner responsibility |

| Tax Benefits | Lease payments often deductible | Depreciation over time |

| Cash Flow Impact | Positive | Negative (initially) |

Questions to Ask Yourself Before Entering a Business Lease

Before signing a lease, ask yourself the following:

Does this decision support my business goals today and tomorrow?

Leasing can be a powerful financial tool, but like any commitment, it works best when it aligns with your cash flow, operational needs, and long-term plans. By taking a few minutes to reflect on the questions below, you’ll set yourself up for a more confident, strategic decision.

- Is this equipment something I need every day, or just for a specific project or short-term use?

- How long will I actually need the equipment, and would leasing give me more flexibility than buying it outright?

- If I lease instead of buy, could I use that saved capital for other important areas like payroll, marketing, or inventory?

- Will the monthly lease payments fit comfortably within my current cash flow?

- Do I need the latest and greatest tech, or would a slightly older model still get the job done?

- What options do I have at the end of the lease—can I buy the asset, return it, or upgrade to something newer?

- Are there any hidden costs I should watch for—like maintenance, end-of-term fees, or penalties for ending the lease early?

How Merchant Growth Can Help

Acquiring new equipment or assets is a strategic move, and leasing offers a smart way to do it without draining your cash flow. It’s flexible, scalable, and ideal for growing businesses that need to stay agile. But if leasing isn’t the right fit—whether due to eligibility or a need for full ownership—term financing can be a strong alternative, offering upfront capital with predictable repayments. The right choice depends on your goals, budget, and how you plan to grow.

At Merchant Growth, we offer flexible financing options that can complement or replace leasing depending on your business needs. From lines of credit to working capital loans, we help Canadian businesses grow without compromising their cash flow.

Explore our financing solutions or speak to our team about how we can help support your next big move.