The Importance of Cash Flow (And How to Stay on Top of Management)

Sales may generate excitement, but it’s cash flow that keeps the lights on. You can have the best products, reliable customers, and a great staff, but if cash isn’t flowing smoothly, your entire business can come to a grinding halt.

The good news? You can manage your cash flow with a few proactive strategies. This will allow you to take control of your finances, avoid cash crunches, and build a stronger foundation for growth.

But before we get to the how, let’s start with the what: What exactly is cash flow, and why does it matter so much?

Unlike profit, which measures the surplus after all expenses have been paid, cash flow focuses on actual liquidity—the money you have available right now. A profitable business can still experience a cash crunch if revenue isn’t collected in time or expenses outpace earnings.

Let’s explore exactly what cash flow is, why managing it matters, how to improve it, and how financing can support positive, predictable cash flow.

Key Takeaways

- Cash flow management is tracking, analyzing, and optimizing the money moving through your business.

- Understanding your cash flow statement helps you stay informed about your financial health.

- Effective cash flow management includes monitoring, forecasting, controlling, and optimizing cash movement.

- Financing tools like lines of credit or invoice factoring can help stabilize cash flow.

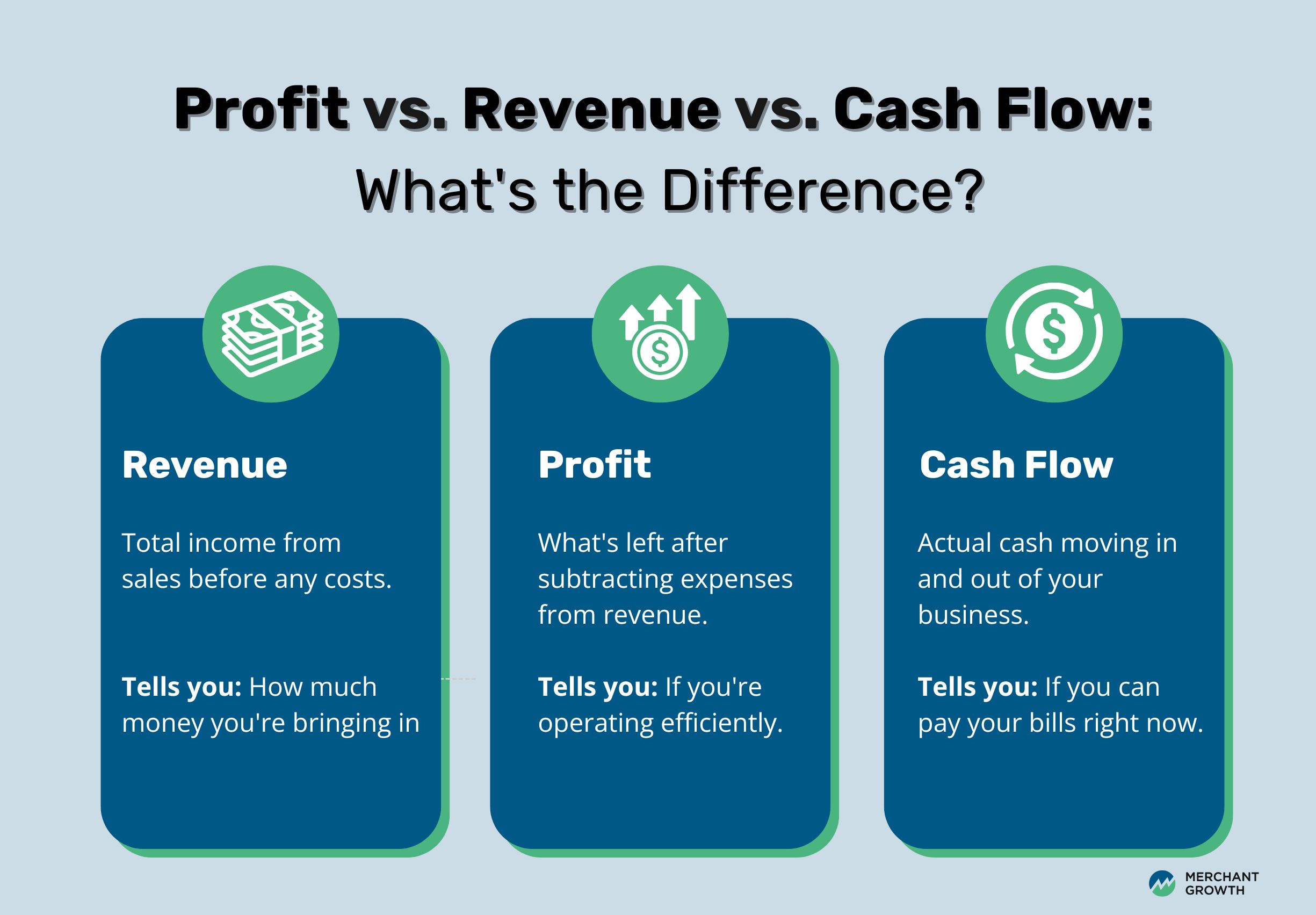

The Difference Between Profit, Revenue, and Cash Flow

Although revenue and profit are often confused with cash flow, they refer to very different concepts. Revenue is the total amount a business earns from its operations, while profit is the amount remaining after all expenses are deducted from that revenue.

Cash flow, however, is the movement of actual cash in and out of your business. You might have high revenue but poor cash flow if clients are slow to pay. Similarly, you could report a profit on paper while struggling to cover expenses due to delayed income or rising costs.

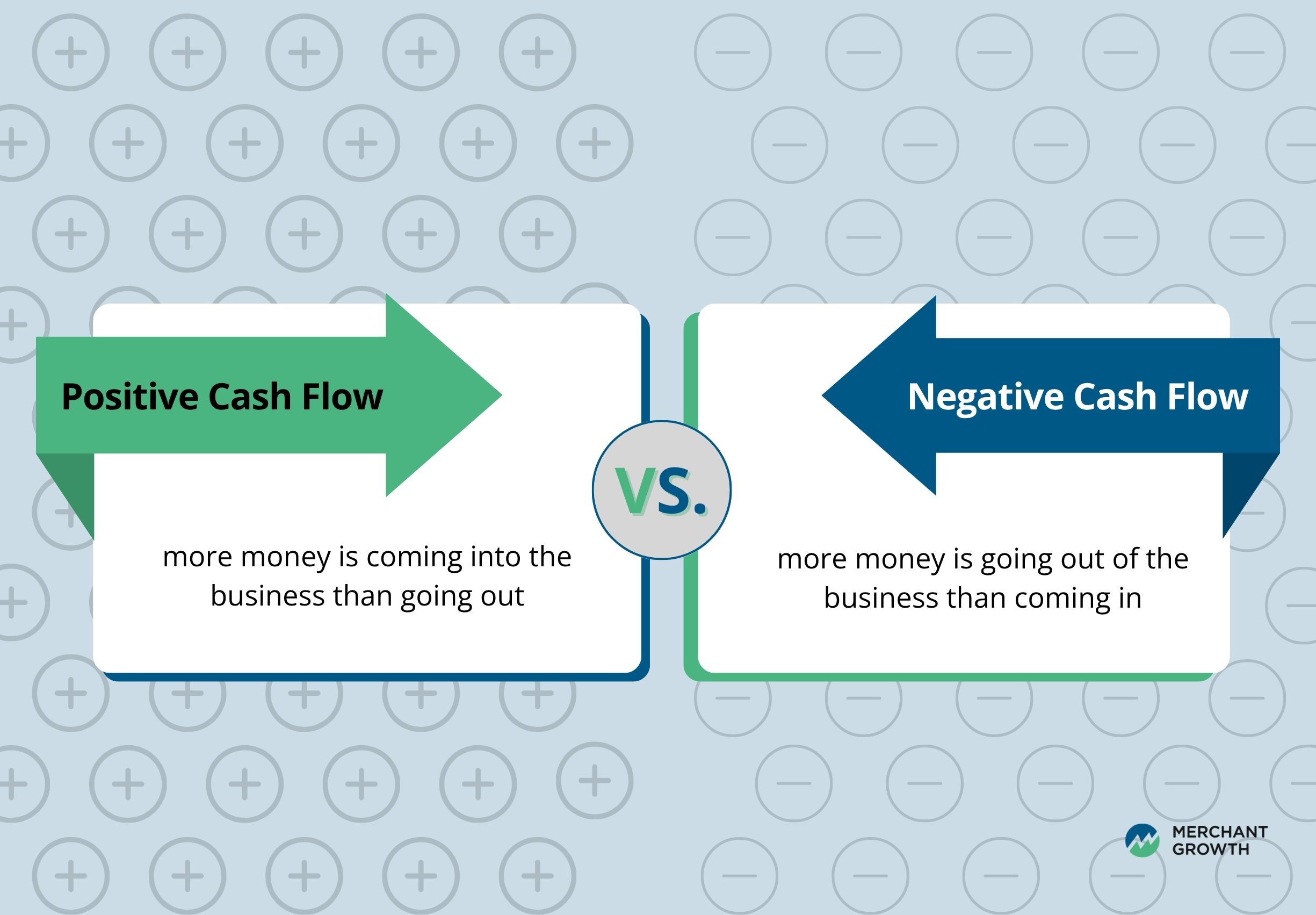

What is the Difference Between Negative and Positive Cash Flow?

Positive cash flow occurs when more money is coming into the business than going out, enabling a company to cover its costs, invest in growth, and build a cash cushion. Negative cash flow, on the other hand, happens when expenses exceed income over a given period. This can lead to financial strain and disrupt business operations.

The Five Cash Flow Categories

While cash flow is typically seen as either positive or negative, it can be broken down further into five categories:

| Cash Flow Category | Definition |

|---|---|

| Operating cash flow | Cash generated from day-to-day operations such as sales and services. |

| Investing cash flow | Cash spent or received from buying or selling assets like property, equipment, or investments. |

| Financing cash flow | Cash from funding sources, including loans, equity investment, or repayments. |

| Net cash flow | The total amount of cash a business gains or loses over a specific period. |

| Future cash flow | Projected cash flow based on current operations and trends, used for planning ahead. |

Understanding these categories helps businesses identify where money is going, uncover inefficiencies, and develop a better growth plan.

What is Cash Flow Management?

Cash flow management is the process of tracking how much money is coming into and going out of your business to ensure that you always have enough on hand to meet obligations and invest in opportunities. It involves monitoring your income, managing your expenses, and making sure there’s a balance between what you’re earning and what you’re spending.

Good cash flow management helps businesses anticipate shortages, avoid overdraft fees or missed payments, and remain flexible in times of uncertainty. For small and medium-sized businesses in Canada, it can be the difference between surviving and thriving.

Why is Cash Flow Management Important?

Managing cash flow isn’t just about balancing the books—it’s about building a business that can weather uncertainty, seize opportunity, and plan for the future with confidence. Even profitable businesses can run into trouble if cash isn’t flowing in at the right time. Without a solid handle on where your money is going—and when it’s coming in—you risk falling behind on payments, missing growth opportunities, or worse, facing financial distress. Below are some of the biggest reasons why cash flow management is essential to your business’s health and success:

Improves financial stability

Consistent cash flow is the foundation of financial stability. When businesses actively track their inflows and outflows, they can spot red flags early, like rising expenses, delayed payments, or declining revenue. Catching these issues before they snowball allows business owners to take timely action, such as adjusting spending or arranging additional funding. It ensures that regular obligations—like payroll, rent, and vendor payments—are met without disruption.

Supports growth

Growth costs money—whether it’s expanding your team, investing in new technology, or launching a new product line. Positive cash flow ensures that funds are available to reinvest without taking on excessive debt or sacrificing operational stability. It provides the flexibility to scale at the right time, take calculated risks, and invest in long-term improvements that fuel your company’s evolution.

Avoids financial distress

Even a few missed payments can grow into serious financial trouble. Without healthy cash flow, businesses may struggle to pay employees, fall behind on vendor accounts, or incur penalties and late fees. Over time, this can damage credit, strain relationships with partners and suppliers, and in extreme cases, lead to insolvency or bankruptcy. Strong cash flow helps you stay ahead of obligations and out of crisis mode.

Helps with making informed decisions

With a clear picture of when money is coming in—and where it’s going—business owners can make smarter, more strategic decisions. Whether you’re budgeting for next quarter, evaluating a new hire, or deciding on a capital investment, accurate cash flow data gives you the insight to plan with confidence and reduce guesswork. It turns decision-making from reactive to proactive.

How to Understand Your Cash Flow Statement

A cash flow statement is broken into three sections:

1. Operating Activities

This section reflects the cash your business generates or spends during its day-to-day operations. It’s a strong indicator of your company’s core financial health.

Includes:

- Cash received from sales of products or services

- Payments to suppliers for inventory or materials

- Employee wages and payroll expenses

- Rent, utilities, and office supplies

- Insurance premiums

- Income taxes paid

- Other operating expenses (e.g., marketing, short-term software subscriptions)

Essentially, if it’s tied to your business’s primary operations, it belongs here.

2. Investing Activities

This section covers cash used to acquire or sell long-term assets, often tied to the growth or future performance of your business.

Includes:

- Purchase or sale of property, equipment, or vehicles (e.g., a new delivery van or computer systems)

- Investments in tools, capitalized software licenses, or technology infrastructure

- Buying or selling shares in other companies (if applicable)

- Proceeds from the sale of long-term assets

These activities don’t happen frequently, but they’re crucial for tracking how your business reinvests capital.

3. Financing Activities

This section tracks how you raise money to fund your business and how you repay those obligations.

Includes:

- Cash received from business loans, lines of credit, or merchant advances

- Equity financing (money received from investors or shareholders)

- Loan repayments (principal only; interest goes in operating activities)

- Owner withdrawals or dividends paid out to shareholders

- Repurchasing company shares (if applicable)

This section helps investors and lenders understand how your business is financed and how you’re managing debt and equity.

Understanding your cash flow statement helps you spot trends, identify potential issues early, and make decisions based on actual liquidity—not just accounting profit. Use accounting software or consult a bookkeeper to review your statement regularly.

👉 Download our Cash Flow Statement Template here.

What Is the Cash Flow of My Business?

To calculate cash flow, begin with your net income (from your income statement), then:

- Add back non-cash expenses like depreciation.

- Subtract increases in non-cash revenues such as accrued revenue.

- Include net figures from investing and financing activities.

This gives you a complete view of your business’s actual cash movement. Regularly calculating cash flow can help you identify bottlenecks or opportunities for improvement.

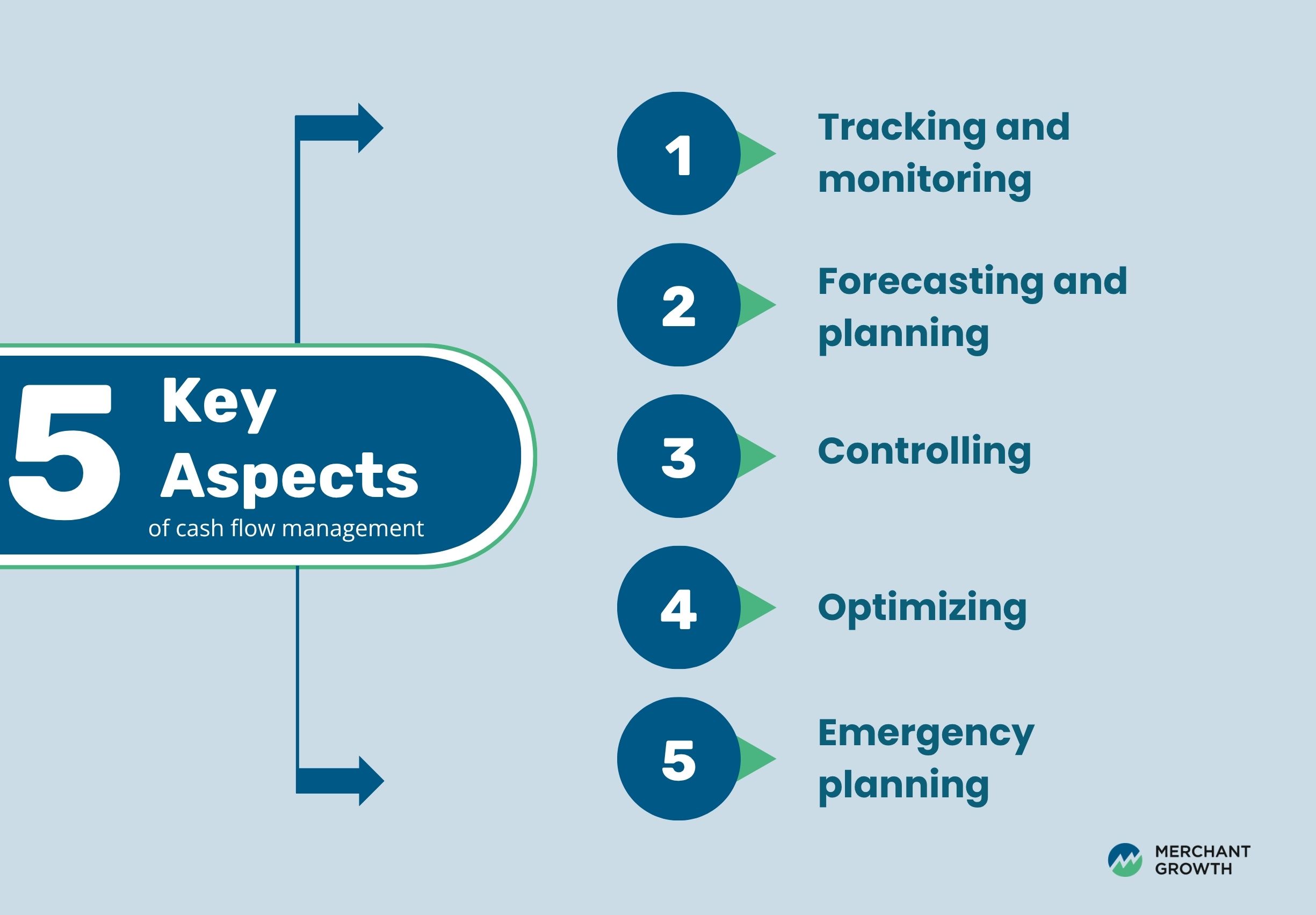

What Are the Key Aspects for Cash Flow Management?

Mastering cash flow doesn’t happen by chance—it requires discipline, planning, and a proactive mindset. Successful business owners treat cash flow management as an ongoing practice, not just a financial report to glance at during tax season. By focusing on a few essential pillars, you can create a system that helps your business stay resilient in lean times and ready to grow when opportunity strikes.

Here are five foundational elements of strong cash flow management:

1. Tracking and monitoring

The first step in managing cash flow is knowing where your money is going—and when it’s arriving. Regularly tracking daily, weekly, and monthly cash movements allows you to stay ahead of any gaps, delays, or unexpected expenses. This isn’t just bookkeeping—it’s visibility. The more frequently you monitor your cash inflow and outflow, the better equipped you’ll be to make real-time adjustments and avoid unpleasant surprises.

Tip: Use cloud-based accounting tools or connect with a bookkeeper who can provide ongoing reports that show cash trends over time.

2. Forecasting and planning

Cash flow forecasting involves projecting your income and expenses over the weeks and months ahead. By using historical data and factoring in upcoming seasonal trends, large purchases, or potential slow periods, you can anticipate when cash might get tight and plan accordingly. Effective forecasting turns your finances from reactive to strategic, helping you avoid last-minute scrambles.

Tip: Build forecasts for multiple scenarios (e.g., best case, expected, and worst case) so you’re always prepared.

3. Controlling

Controlling your cash flow is about actively managing expenses and tightening up areas where money might be leaking. This means sticking to budgets, reviewing costs regularly, and keeping a close eye on payment terms. Ensure you’re not paying vendors faster than you’re being paid, and try to align outflows with inflows as closely as possible.

Tip: Implement approval processes for larger expenses and review recurring charges quarterly to trim unnecessary costs.

4. Optimizing

Optimization focuses on getting the most out of every dollar your business spends or earns. This can include renegotiating supplier contracts, improving your invoicing process to speed up payments, or incentivizing early customer payments. Small adjustments to operations or cash management processes can have a big impact over time.

Tip: Offer early payment discounts to clients and consider automating your billing system to avoid delays.

5. Emergency planning

No matter how well you plan, unexpected costs can and will arise—whether it’s a broken piece of equipment, a late-paying client, or a market downturn. Emergency cash flow planning involves setting aside a financial buffer or access to fast capital so you’re not caught off guard. This fund is your safety net, helping you cover urgent expenses without disrupting operations or going into high-interest debt.

Tip: Aim to build a contingency reserve equivalent to at least one month of operating expenses, and consider maintaining access to a line of credit for additional flexibility.

Technique & Tips for Successful Cash Flow Management

Once you understand the importance of cash flow, the next step is putting practical strategies into action. This section focuses on simple, actionable techniques that can help you manage your cash flow more effectively on a daily, weekly, and monthly basis. Whether you’re looking to tighten control, improve predictability, or support future growth, these tips are designed to give you more clarity and confidence in your business’s financial operations.

Perform cash flow analysis regularly

Reviewing your cash flow on a weekly or monthly basis is one of the simplest but most powerful ways to spot trends before they become problems. Look at your cash inflows and outflows to understand what’s driving your financial position — and where adjustments might be needed. Regular reviews help you make proactive decisions and plan for both expected and unexpected changes.

Slow down the outflow

Managing cash flow means stretching every dollar as far as it can go. Whenever possible, negotiate longer payment terms with suppliers or delay non-essential spending. This gives your business more time to generate revenue before bills are due, keeping more cash in hand during tight periods.

Audit your expenses

Wasteful or redundant expenses can quietly chip away at your financial stability. Schedule regular expense audits to identify subscriptions, services, or purchases that no longer serve your business goals. Even small cuts can free up meaningful cash over time — without sacrificing operational efficiency.

Use credit strategically

Business credit should act as a safety net or bridge — not a crutch. Use a business line of credit or short-term financing to cover temporary cash gaps, manage inventory cycles, or respond to urgent needs. Avoid relying on credit for ongoing expenses that indicate deeper cash flow issues.

Make inflow reliable

Improving your receivables process helps ensure cash flows in when it’s supposed to. Send invoices promptly, include clear payment terms, and consider offering early payment incentives. Establishing consistent follow-ups for overdue invoices can also minimize delays and improve predictability in your revenue stream.

Add a layer of protection

Having an emergency reserve or rainy-day fund can help you navigate seasonal slowdowns, unexpected repairs, or market downturns without panic. Even setting aside a small percentage of revenue each month can create a cushion that protects your business’s long-term health.

Scale with intention

Growth is exciting, but it must be sustainable. Before expanding your team, inventory, or physical space, make sure your current and forecasted cash flow can support the move. Scaling too fast without the cash to back it up is a common pitfall that can quickly lead to financial strain.

Lean into tech

Modern financial tools can automate cash flow tracking, reporting, and forecasting. Cloud-based accounting software, integrated payment platforms, and real-time dashboards provide clarity and save time, allowing you to focus on making informed, strategic decisions.

Business Types that May be More Prone to Cash Flow Management Issues

While every business needs to manage its cash flow, some industries are naturally more vulnerable to fluctuations due to the nature of their operations. Factors like seasonality, economic cycles, or heavy upfront investment requirements can create uneven revenue streams — making it harder to maintain consistent liquidity. Below are two types of businesses that often face unique cash flow challenges, along with examples of how and why these issues arise.

Cyclical industries

Industries tied to commodity pricing or broader economic cycles—such as construction, oil and gas, mining, and manufacturing—often deal with unpredictable demand. For instance, construction companies may experience project delays during economic downturns or harsh winters, halting payments and pushing back revenue timelines. Similarly, manufacturers reliant on fluctuating raw material prices may see profit margins squeezed, impacting cash reserves.

Seasonal businesses

Companies in industries like retail, tourism, events, landscaping, and agriculture often generate the bulk of their revenue during specific times of the year, while certain expenses continue more evenly across the calendar. For example, a ski resort may earn most of its income during the winter months but still needs to maintain head office staffing, handle off-season maintenance, and invest in year-round marketing to stay top of mind. Similarly, agricultural businesses typically spend heavily on equipment, planting, and labor in the spring but may not see revenue until harvest season months later. While some costs—like seasonal staff—drop off after peak periods, key operational and preparatory expenses often persist throughout the year.

Common Cash Flow Management Issues to Avoid

Even with the best intentions and strategies, cash flow issues can creep in when certain business practices go unchecked. Identifying and avoiding these common pitfalls is crucial for maintaining financial stability and growth. Below are some of the most frequent cash flow challenges that businesses, especially small and growing ones, should watch out for.

Rapid business growth & expansion

Growth is exciting, but scaling too quickly without a solid financial footing can be dangerous. Rapid expansion often comes with increased expenses—new hires, inventory, marketing, equipment—that require upfront capital. If cash inflows can’t keep up, businesses may find themselves overextended and struggling to meet financial obligations, despite strong sales.

Lacking organization in your accounts receivable

Cash flow problems often stem from money that’s earned but not yet collected. Without clear systems for sending invoices, following up on late payments, and tracking receivables, it’s easy for payments to slip through the cracks. Disorganized accounts receivable processes delay inflows and can leave businesses short on cash, even when sales are strong.

Extending credit without safeguards

Offering payment terms to customers can help close sales, but doing so without proper credit checks or limits can be risky. If too much of your capital is tied up in unpaid invoices, your business may struggle to cover its own bills. Without a well-managed credit policy, what seems like a customer-friendly gesture can quickly turn into a liquidity crisis.

Difficulty projecting expenses

Unexpected costs are a part of business, but failing to anticipate them can throw your cash flow off course. Many businesses underestimate recurring costs (like taxes or maintenance) or forget to build in a buffer for emergency expenses. Without a reliable forecast, even a small surprise cost can force you into short-term borrowing or payment delays.

How to Increase Cash Flow

If your business is experiencing negative cash flow—or if you’re simply looking for ways to improve your overall cash position—there are several proactive steps you can take. Strengthening cash flow doesn’t always require drastic changes; in many cases, small, strategic adjustments to how you manage expenses, collect payments, or plan ahead can make a significant difference. The following techniques can help you improve liquidity, reduce financial stress, and create a more stable foundation for growth.

- Reduce operating expenses: Cut unnecessary costs by renegotiating contracts or outsourcing.

- Increase revenue: Add new revenue streams or increase prices.

- Improve collection of accounts receivable: Use payment incentives and enforce late fees.

- Manage inventory levels: Reduce overstock and optimize turnover.

- Seek financing: Use loans or lines of credit to cover shortfalls and fund growth.

Financing for Cash Flow Management

Financing can be a valuable tool for supporting positive cash flow, especially during slow periods, seasonal downturns, or when facing large, upfront costs that could otherwise strain your budget. Rather than depleting your cash reserves to cover operating expenses or investments, the right financing solution, such as a business line of credit or a short-term loan, can provide the flexibility needed to maintain stability. These options allow businesses to bridge temporary gaps in cash flow, manage recurring costs, and seize growth opportunities without sacrificing day-to-day operations. Choosing the right type of financing is key to ensuring it works with, rather than against, your broader financial strategy.

Line of credit

A business line of credit can assist businesses in improving their cash flow by offering a flexible source of funds that can be used as required. A line of credit can bridge gaps in cash flow, manage growth periods, and take advantage of unexpected opportunities. It also helps businesses to avoid late payment penalties, improve purchasing power, and ensure smooth operations.

Invoice factoring

Invoice factoring can improve a company’s cash flow by providing immediate funds based on their outstanding invoices, reducing the need for collections and improving cash flow predictability. It can also help companies maintain good customer relationships by offering more flexible payment terms and avoid taking on additional debt since it is not a loan.

Term financing

Term financing is an option that can help companies improve their cash flow by providing immediate funds based on future credit and debit card sales. It is easy to qualify for, does not require collateral, and has flexible repayment terms that adjust based on the business’s cash flow. With term financing merchant cash advance, businesses can predict their future cash flow based on their credit and debit card sales, helping them better plan and manage their finances.

Strategic use of financing can be the difference between stalling and seizing an opportunity. Whether you’re ramping up for a busy season, investing in new equipment, or simply smoothing out uneven revenue cycles, access to flexible capital lets you move forward without putting strain on your day-to-day cash flow. If you’re exploring how financing can fit into your cash flow strategy, this overview of cash flow financing options is a helpful place to start.

Merchant Growth Can Provide the Funds Your Business Needs

Managing cash flow effectively is essential for the long-term success of any business. If you’re struggling to manage your cash flow or having negative cash flow difficulties, Merchant Growth can help. As a leading alternative lender for small and medium-sized businesses, we offer a range of financing solutions that will help your business thrive.

Our financing solutions include fixed financing, business lines of credit, and more. So, if you’re looking to improve your cash flow and take your business to the next level, contact Merchant Growth today to learn more about our financing solutions.