Are We in a Recession? What Canadian Small Businesses Are Saying—and How to Prepare

Are we in a recession, or just feeling like we are? With rising costs, cautious consumers, and increasing chatter about a potential economic downturn, many Canadian small business owners are left navigating more questions than answers. Officially, Canada hasn’t entered a recession—but the warning signs are starting to stack up, and the uncertainty is real.

To better understand how this moment is impacting entrepreneurs on the ground, Merchant Growth conducted an exclusive survey of 150 small business owners across Canada in June 2025. While economists debate GDP numbers and technical definitions, our goal was simple: to capture how business owners are actually feeling, what they’re doing, and where they’re struggling most.

The result is a real-world snapshot of how small businesses are bracing for economic turbulence—and what strategies they’re already putting in place to stay resilient.

Here’s what Canadian entrepreneurs told us—and what you can learn from their experiences to better prepare your own business.

Key Takeaways

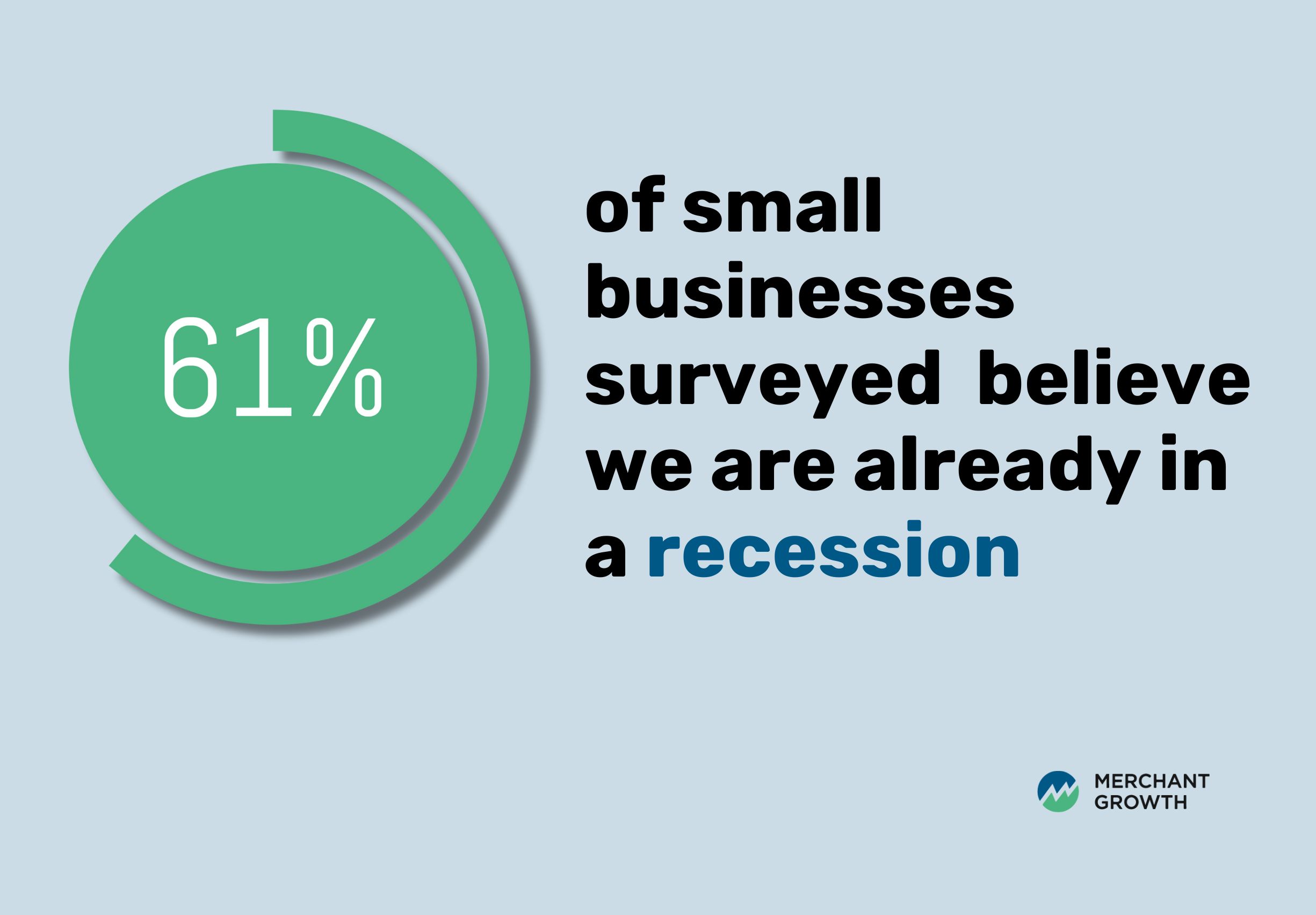

- Most small businesses believe Canada is already in a recession or will be soon — 61% think we’re in a downturn now, and another 22% expect one within the year.

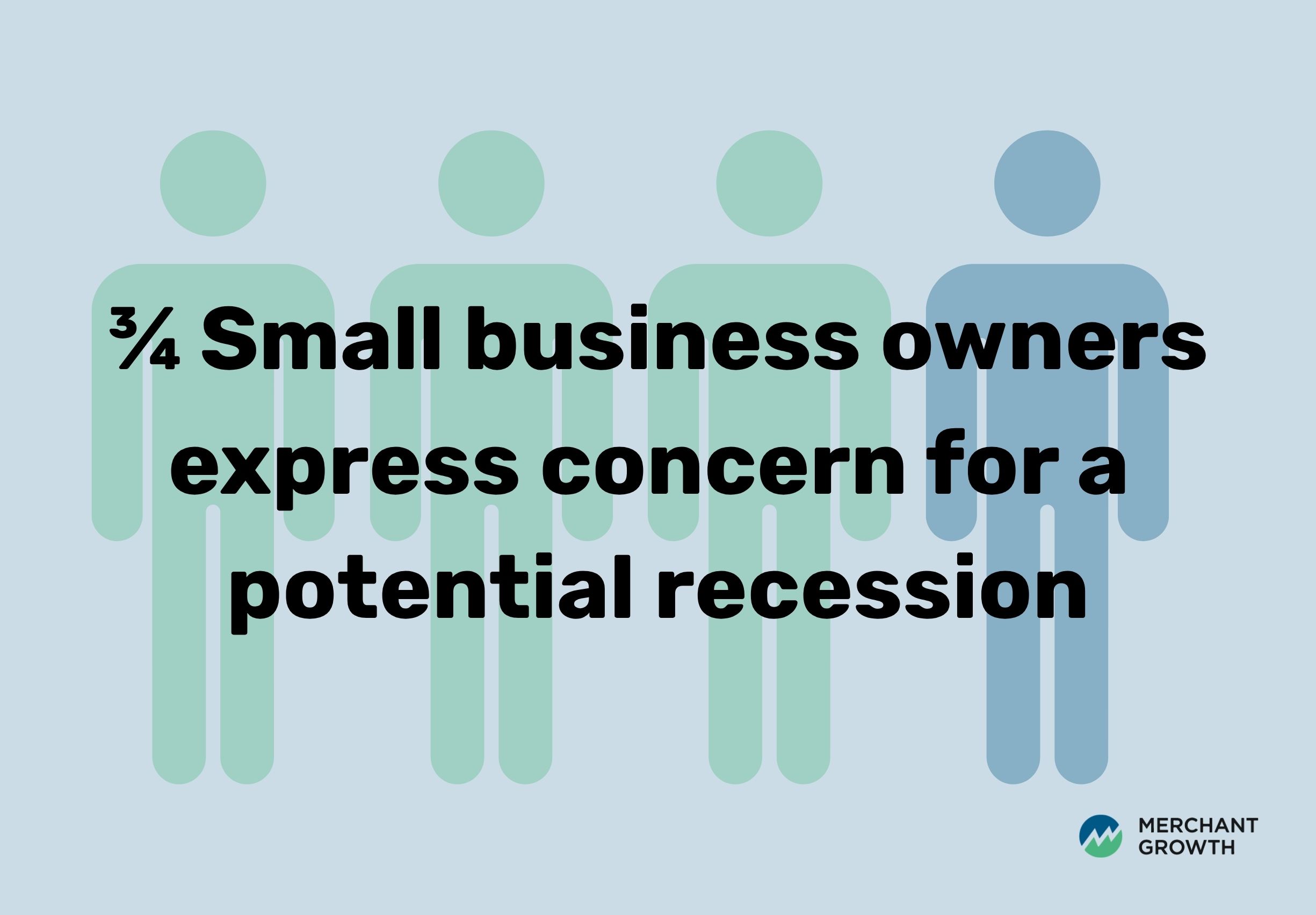

- Concern is high, and action is happening — 74% of respondents are concerned about the economy, with the majority cutting costs, delaying hiring, and pausing expansion to stay ahead.

- Access to support is a top priority — 75% of businesses surveyed said access to low-interest loans would be most helpful, alongside requests for tax relief, subsidies, and less red tape.

- Preparation is the best strategy — Understanding cash flow, diversifying revenue, and building lender relationships now can help businesses stay resilient, no matter what the economy brings.

What Is a Recession—and Why Does It Matter for Small Businesses?

A recession is typically defined as two consecutive quarters of economic decline, often measured by GDP. For small business owners, however, the technical definition matters less than the real-world impact—reduced customer spending, tighter credit, slower payments, and pressure to scale back operations.

Recessions also bring opportunity. Some of the most successful businesses today were born or rebuilt during downturns. What matters is how you prepare and adapt.

What Canadian Small Businesses Are Saying Right Now

To better understand how entrepreneurs are feeling about the economy in mid-2025, Merchant Growth surveyed 150 small business customers across Canada. Their responses provide an honest and insightful snapshot of how businesses are interpreting the current climate and preparing for potential economic turbulence.

How Small Business Owners Feel About the Current Canadian Economy

When asked about the current state of the Canadian economy, 61% of small business owners said they believe the country is already in a recession or economic downturn. Another 22% felt a downturn is not yet here, but likely within the next 12 months. Only a small fraction—9%—believe a recession isn’t coming anytime soon.

This shows a strong majority of small business owners are either already feeling the impact or bracing themselves for a shift in the coming year.

Entrepreneurs Share Concern for Potential Recession

Not surprisingly, this economic sentiment is paired with a high level of concern. Three in four business owners (74%) reported feeling either somewhat or very concerned about a potential recession. Meanwhile, only 3% said they are not at all concerned, suggesting that anxiety about the economy is nearly universal among respondents.

Many Small Businesses Are Already Adjusting

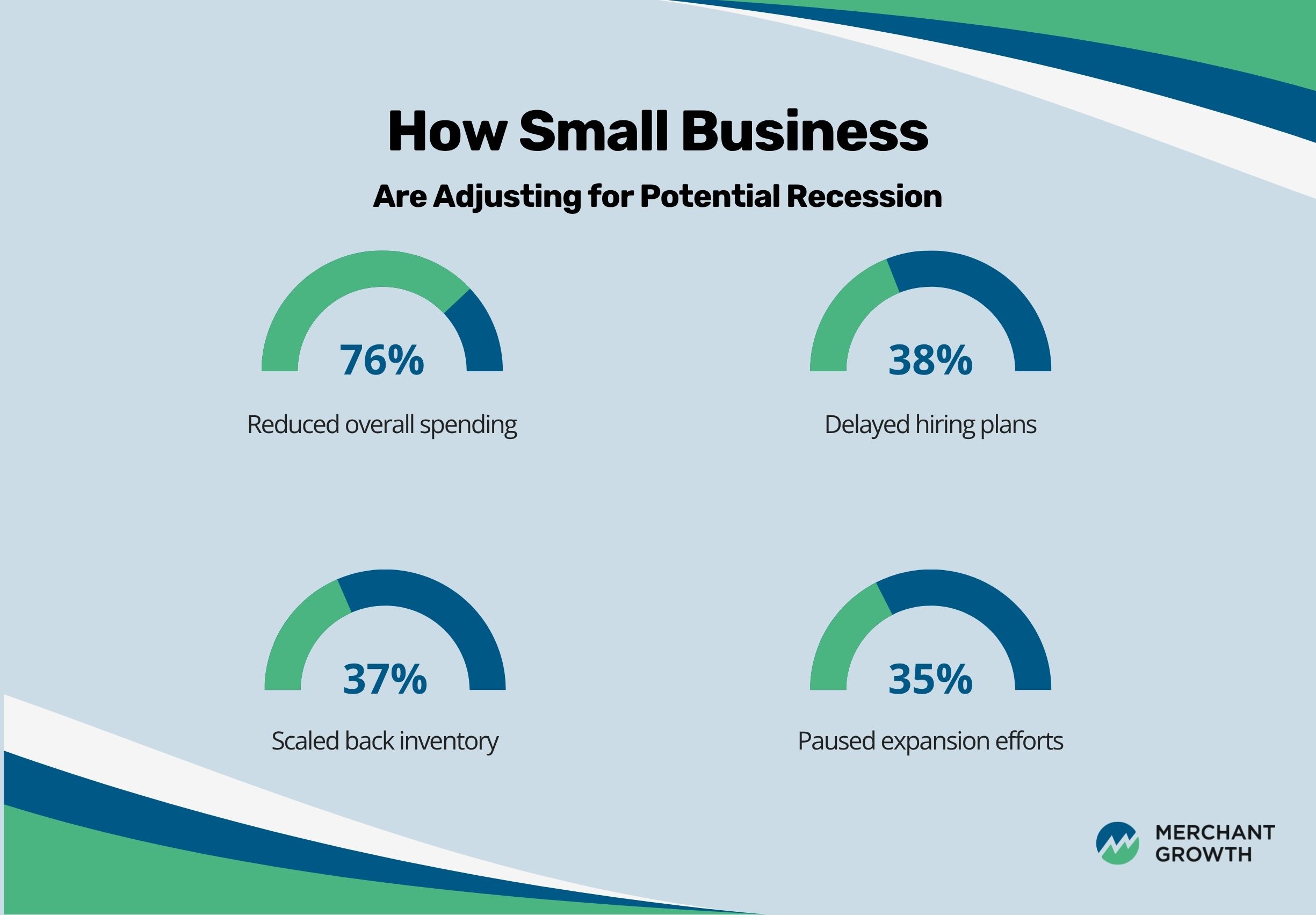

That concern is turning into action. Many entrepreneurs are already making strategic decisions to protect their operations. Among those who have taken steps to prepare:

- 76% have reduced overall spending

- 38% have delayed hiring plans

- 37% have scaled back inventory

- 35% have paused expansion efforts

Interestingly, 20% of businesses haven’t made any changes yet, which may reflect either confidence in their current model or uncertainty about what steps to take.

Canadian Businesses Maintain Confidence to Navigate a Recession

Despite the challenges, more than half of the respondents still feel optimistic about their ability to weather a potential downturn. 56% of business owners said they feel confident—or very confident—in their ability to navigate a recession. That said, 26% feel neutral, and 18% expressed low confidence, indicating that many are still unsure how they’ll manage if conditions worsen.

Is Canada Officially in a Recession?

Economists are divided. While inflation has cooled and interest rates remain high, GDP growth has slowed, and consumer spending has softened. Technically, Canada may not yet meet the formal criteria for a recession at the time of writing, but many small business owners are already feeling the effects.

Remember: small businesses often feel the economic pinch well before it shows up in official data. Declining foot traffic, longer sales cycles, and cautious customers are often the first signs.

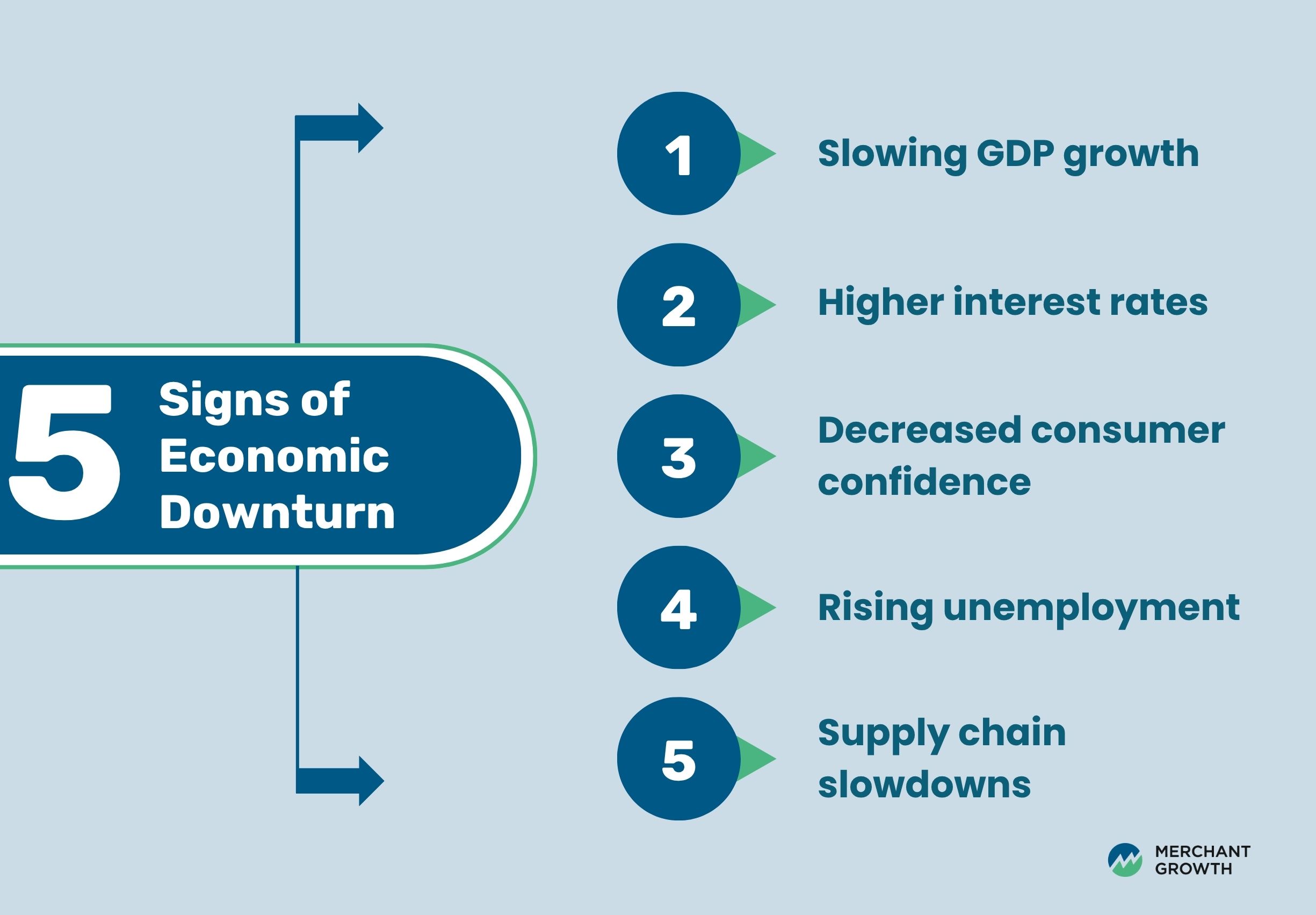

Signs We Might Be Heading for a Downturn

Economic forecasts can be uncertain, but there are consistent indicators that economists and business leaders alike watch to assess the health of the economy. While Canada hasn’t officially declared a recession, many of these markers are flashing yellow, and small business owners are feeling the pressure.

Some of the clearest signs pointing to a potential downturn include:

- Slowing GDP growth

- Higher interest rates

- Decreased consumer confidence

- Rising unemployment

- Supply chain slowdowns

These factors don’t guarantee a recession, but they do signal shifting conditions. Our survey shows many entrepreneurs aren’t waiting for confirmation—they’re already adjusting their strategies in response to what they’re seeing on the ground.

How a Recession Impacts Canadian Small Businesses

A recession can hit small businesses in subtle ways at first—until suddenly, it’s everywhere. Sales slow down, clients become cautious, and the everyday rhythm of your business feels off. For many entrepreneurs, it’s not one big crisis but a series of small strains that build over time.

Here are some of the most common challenges small businesses face during a downturn:

Customers pull back on spending

Whether you’re selling products or services, recessions typically cause consumers and businesses alike to cut non-essential purchases. Even loyal customers may reduce how often they buy or start shopping around for cheaper alternatives. If your business serves other businesses (B2B), their tightening budgets can also reduce demand for your services.

Sales cycles stretch out

It often takes longer to close deals. Prospects may hesitate, postpone decisions, or require more convincing than usual. For subscription-based or service-oriented businesses, this can lead to inconsistent cash flow and added stress on sales teams or solo operators.

Inventory and supply chain costs rise

Inflation and supply disruptions don’t disappear during a downturn—in fact, they can worsen. You may find yourself paying more for inventory while customers are simultaneously spending less. This squeeze on both sides makes it harder to maintain healthy margins.

Credit terms become stricter

Suppliers, lenders, and partners may tighten payment terms or reduce access to credit. If you’ve relied on trade credit or small loans to keep operations running smoothly, this shift can limit your flexibility or even force you to scale back unexpectedly.

Financing becomes harder to secure

Banks and alternative lenders typically become more risk-averse during uncertain times. If your business isn’t already on solid financial footing—or lacks a strong track record—it may be more difficult to qualify for loans or lines of credit just when you need them most.

Employee stress and retention issues

In times of economic uncertainty, your team may worry about job security, reduced hours, or frozen wages. For small teams, even one resignation or burnout episode can have a big impact.

While these impacts are challenging, they’re not insurmountable. The key is to stay agile—keep a close eye on your cash flow, focus on high-value customers, and be ready to adjust your strategy as conditions evolve.

Recessions test your resilience, but they also push you to run a smarter, leaner, and more focused business. By being proactive rather than reactive, you can protect what you’ve built—and even find opportunities others overlook.

How to Prepare Your Business for a Recession

Recessions are challenging, but with thoughtful preparation, your business can weather the storm and even come out stronger. Preparation doesn’t mean bracing for disaster; it means making intentional decisions to strengthen your foundation, improve cash flow, and reduce vulnerability. The following strategies are practical, proactive, and widely recommended by financial experts and small business advisors.

1. Review Your Cash Flow in Detail

Cash flow is the heartbeat of your business—especially in uncertain times. Review your inflows and outflows regularly to understand how much working capital you truly have. Can you confidently cover next month’s expenses if revenue slows down? Look for any recurring costs that are quietly eroding your margins.

Tip: Use a cash flow forecast to map out your finances for the next 3–6 months. And if you don’t already have one, now’s a great time to download our free Cash Flow Template.

2. Cut Non-Essential Expenses

Recessions call for a leaner approach. Scrutinize every recurring cost—subscriptions, software tools, professional memberships, marketing services—and ask, “Is this absolutely necessary right now?” Cancel or pause anything that doesn’t directly contribute to revenue or business stability. Be careful not to cut things that will hurt long-term growth, like essential marketing or client service tools.

3. Diversify Your Revenue Streams

If most of your income comes from one product, client, or market segment, you’re vulnerable. Look for ways to broaden your offerings: introduce lower-cost services, bundle packages, explore new platforms, or tap into different customer groups. The goal isn’t to reinvent your business overnight, but to reduce reliance on any one source of income.

Example: A freelance designer could offer template packages or branded merchandise. A retailer might introduce subscription boxes or pop-up sales online.

4. Stay Visible with Smart Marketing

Marketing doesn’t need to stop during a downturn—it just needs to be smarter. Keep your brand top of mind by focusing on cost-effective tactics: email newsletters, organic social media, customer referrals, and community partnerships. Messaging should reflect the moment—emphasize value, empathy, and solutions to customer pain points.

5. Build or Maintain a Cash Buffer

If you can, set aside at least 2–3 months’ worth of operating expenses in an emergency fund. If that’s not possible right now, focus on improving your accounts receivable: invoice promptly, follow up consistently, and consider offering small early payment incentives. Having some runway gives you breathing room when income dips or costs spike.

6. Talk to Lenders Before You Need Them

If financing might be part of your strategy during a downturn, don’t wait until you’re desperate. Build relationships with lenders while your business is still relatively stable. This includes your bank, government-backed programs like the BDC, and alternative lenders. Being proactive gives you more options—and better terms—than scrambling under pressure.

Canadian entrepreneurs are already taking action—cutting costs, pausing expansion plans, and focusing on what matters most. These small, strategic shifts can build real financial resilience and help maintain control, even in uncertain times.

What Canadian Small Businesses Say They Need Most

Access to the right support can make the difference between simply surviving a downturn and emerging stronger. We asked Canadian entrepreneurs what types of assistance would help them navigate an economic slowdown—and their answers were clear. From affordable financing to reduced red tape, small business owners are looking for targeted, accessible resources that meet the realities they’re facing on the ground.

Here’s what they told us:

| Support Type | % of Respondents Wanting It |

|---|---|

| Low-interest small business loans | 75% |

| Permanent tax relief | 55% |

| Wage or hiring subsidies | 39% |

| Rent or utility subsidies | 36% |

| Reduced red tape/regulatory burden | 18% |

Fortunately, programs like the BDC, Canada Digital Adoption Program, and provincial loan initiatives exist, but many businesses say it’s still hard to access support quickly.

Why Recession Talk Feels So Uncertain

The truth is, there’s no single light switch that flips from “growth” to “recession.” Economic slowdowns don’t always follow a clear timeline—and for small business owners, that uncertainty can be one of the biggest challenges.

Canada’s current economic landscape is shaped by a mix of persistent and emerging pressures:

- Lingering post-pandemic shifts continue to affect how people work, shop, and spend.

- Global supply chain issues are still causing delays and unpredictability across industries.

- High household debt is limiting consumer spending and stretching budgets thin.

- Rising borrowing costs—driven by high interest rates—are making it harder for businesses to access capital or finance growth.

These overlapping factors create a grey zone, where the economy may not be in a technical recession, but still feels strained. For entrepreneurs, it can feel like walking a tightrope—balancing caution with ambition.

That’s why this is the time to prioritize scenario planning, improve financial visibility, and stay adaptable. When conditions are uncertain, clarity becomes your most powerful tool.

Merchant Growth: Standing with Canadian Businesses

At Merchant Growth, we’re committed to supporting entrepreneurs through all economic cycles. That’s why we surveyed our customers, and why we continue to offer flexible financing options like:

- Term loans for equipment or one-time investments

- Lines of credit for working capital or seasonal dips

Whether you’re preparing, pivoting, or growing through uncertainty, we’re here to help.

Final Thoughts: Stay Grounded, Stay Ready

There’s no need to panic—but there is a need to plan. Whether or not Canada enters a technical recession, many small businesses are already making smart, proactive decisions.

Take time now to understand your numbers, streamline your operations, and strengthen relationships with clients, partners, and lenders.

Need support or financing? Let’s talk. Merchant Growth is ready to help you face whatever comes next—with confidence.