How Much Is Business Insurance? A Guide for Canadian Small Business Owners

Running a small business in Canada means juggling a lot—inventory, customers, payroll, and day-to-day operations. But even with the best planning, things like weather-related damage, equipment breakdowns, or a client dispute can quickly throw things off track. That’s where business insurance comes in

Still, for many entrepreneurs, insurance can feel like just another line item on an already tight budget. According to a 2024 report from the Canadian Federation of Independent Business, 62% of small business owners consider insurance costs to be among the most harmful expenses to their operations. The report also found that half of Canadian business owners experienced a 10% increase in insurance premiums within the last year, adding up to as much as $1,500 in additional costs for some. While the price tag can sting, the cost of not having coverage when something goes wrong can be far higher.

So, how much does business insurance actually cost? And what kind of coverage does your business need? In this guide, we’ll break it all down.

Key Takeaways

- Business insurance in Canada can cost as little as $25 to as much as $250/month, depending on your business type, location, and industry risk level.

- Common policies include general liability, property insurance, and business interruption coverage.

- Online tools and brokers make it easier than ever to compare quotes and tailor your coverage.

- Not having insurance can leave your business vulnerable to legal and financial setbacks.

What Is Business Insurance (and Do You Really Need It)?

Business insurance protects your company from financial losses tied to accidents, lawsuits, damage, or other unexpected events. It’s not always legally required, but it’s often necessary.

Although business insurance isn’t federally mandated in Canada, it often becomes essential depending on where and how you operate. Certain provinces prescribe coverage for specific industries, particularly those involving commercial vehicles or higher-risk fields like construction and transportation. Even if it’s not legally required, many landlords and clients won’t move forward without proof of insurance. Whether you’re a consultant, tradesperson, retailer, or freelancer, having the right policy in place adds professionalism and helps you operate with confidence.

What Does Business Insurance Cover?

Business insurance isn’t one-size-fits-all. It can—and should—be tailored to match the nature of your operations, your risks, and your industry. Whether you run a storefront, consult from home, or manage a growing team across multiple locations, having the right types of coverage helps protect your bottom line. Below are some of the most common policies Canadian small business owners should consider.

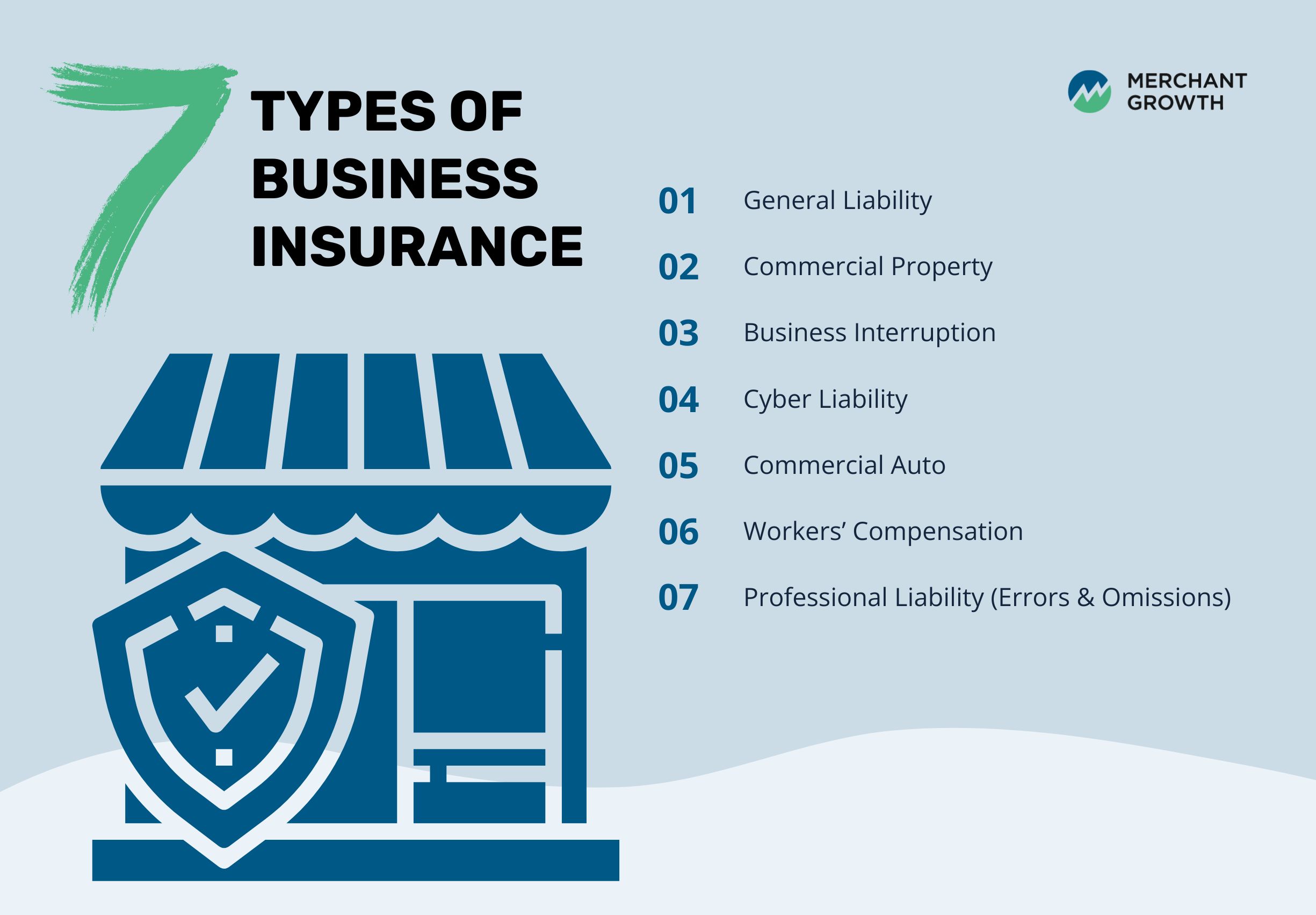

General Liability

General liability insurance covers third-party claims for bodily injury, property damage, or personal injury (like libel or slander) that arise from your business operations. It’s not legally required, but it’s strongly recommended for nearly all businesses, especially those that interact with customers, operate a physical location, or provide hands-on services. In fact, 92% of insured Canadian small businesses carry this type of coverage, according to the CFIB in 2024.

Example: A customer trips over a display at a local flower shop and suffers a sprained ankle. The shop’s general liability insurance covers their medical expenses and legal costs if the customer decides to sue.

Commercial Property

This coverage protects your business’s physical assets—like equipment, inventory, furniture, or buildings—from risks such as fire, theft, vandalism, or weather-related damage. While it’s not legally mandatory, it’s often required by lenders or landlords if you lease a commercial space. It’s especially valuable for retail stores, warehouses, restaurants, and manufacturers. 84% of insured Canadian small businesses have this type of coverage in place.

Example: A burst pipe damages inventory at a clothing boutique. Commercial property insurance helps cover repair costs and product losses.

Business Interruption

Also known as income interruption coverage, this insurance helps replace lost income and cover ongoing expenses if your business is forced to shut down temporarily due to a covered event (like fire or flooding). It’s usually added as part of a commercial property policy.

Example: A bakery is forced to close for two weeks after a kitchen fire. Business interruption insurance helps cover payroll, rent, and lost revenue during the downtime.

Professional Liability (Errors & Omissions)

Professional liability insurance protects businesses that provide services or advice. It covers legal costs and damages if a client claims your work caused them financial harm due to a mistake, oversight, or failure to deliver. This coverage is essential—and sometimes required—for consultants, marketing firms, real estate agents, financial advisors, and similar professions.

Example: A freelance web designer misses a key deadline, causing their client to lose a major launch opportunity. Professional liability insurance covers legal fees and any settlements.

Cyber Liability

This policy protects against losses related to data breaches, hacking, or other cybersecurity threats. It’s becoming increasingly vital for any business that stores sensitive customer or payment information online. While not mandatory, it’s highly recommended in industries like e-commerce, healthcare, finance, and IT.

Example: A physiotherapy clinic’s patient database is compromised in a cyberattack. Cyber liability insurance covers the cost of notifying clients, legal defence, and reputation management.

Commercial Auto

If you use a vehicle for business—whether for deliveries, job site visits, or transporting tools—commercial auto insurance is legally required. This applies even if you’re using a personal vehicle for work-related tasks. It’s a must-have for tradespeople, mobile service providers, and delivery-based businesses. In fact, 69% of insured Canadian small businesses carry this type of coverage.

Example: An electrician uses their van to transport tools to job sites. If they’re involved in an accident while on a call, commercial auto insurance covers the damage and liability costs.

Workers’ Compensation

In most provinces, workers’ compensation is mandatory if you have employees. It covers medical expenses and lost wages if a worker is injured on the job. Requirements vary by province, but it’s typically managed through a provincial board (like WorkSafeBC or WSIB in Ontario).

Example: A warehouse employee injures their back while lifting heavy stock. Workers’ compensation helps cover their medical treatment and time off work.

How Much Does Business Insurance Cost in Canada?

Business insurance costs in Canada can vary significantly depending on your industry, size, and risk level. According to Ratehub, some small businesses may pay as little as $400 to $2,500 annually, but premiums can climb much higher in industries with more complex operations or greater exposure to liability.

CFIB data states that commercial auto insurance is typically the most expensive coverage for SMEs, averaging around $6,000 per year. Commercial property insurance follows at $5,000, and general liability insurance comes in close behind at about $4,850.

Certain industries tend to carry higher premiums across the board. For example:

- Transportation businesses often face $16,000+ annually in commercial auto premiums.

- Construction firms pay roughly $9,850 for auto and up to $10,000 for liability insurance.

- Manufacturing and hospitality businesses see average costs of around $8,000 for property coverage and $7,800 for liability.

- Agricultural businesses top the property insurance category at $9,000 per year.

While these averages help give a general sense of what to expect, business insurance premiums can also vary significantly by province. For example, businesses in Ontario and British Columbia often face higher rates due to greater population density, higher claim volumes, and more complex regulatory environments. In contrast, provinces like Alberta or Manitoba may offer more competitive premiums, though factors like extreme weather or local industry risks (e.g., oil and gas) can drive up costs. Wherever you operate, it’s important to compare quotes within your province and industry to ensure you’re getting the right coverage at a fair price.

Other Factors That Affect Cost

In addition to your industry and coverage type, several other variables can influence how much you pay for business insurance in Canada. Insurers evaluate your risk profile based on both operational details and your history, which can cause rates to vary widely between businesses, even within the same sector.

1. Business Size and Revenue

Larger businesses or those with higher revenue typically face greater risks, which can lead to higher premiums. Insurers may assume you have more assets to protect or a larger customer base to be liable for.

2. Number of Employees

The more employees you have, the more likely you are to need workers’ compensation coverage or face risks related to human error, injury, or employment practices liability.

3. Type of Industry and Services Offered

High-risk industries like construction or manufacturing usually pay more for insurance than low-risk sectors like consulting or online retail due to the potential for injury, property damage, or equipment failure.

4. Previous Claims History

If your business has made frequent or high-value claims in the past, insurers may see you as a higher risk and charge more. A clean claims record can help reduce your premiums.

5. Where Your Business Operates (Urban vs. Rural)

Your location affects both the likelihood and cost of potential claims. Urban areas often have higher rates due to the increased risk of theft, property damage, or lawsuits compared to rural locations.

How to Get Business Insurance in Canada

Getting insured doesn’t have to be overwhelming. In fact, a well-chosen policy can bring peace of mind and allow you to focus on what really matters—running your business. Whether you’re just starting out or revisiting your current coverage, here’s a step-by-step guide to help you navigate the process with confidence.

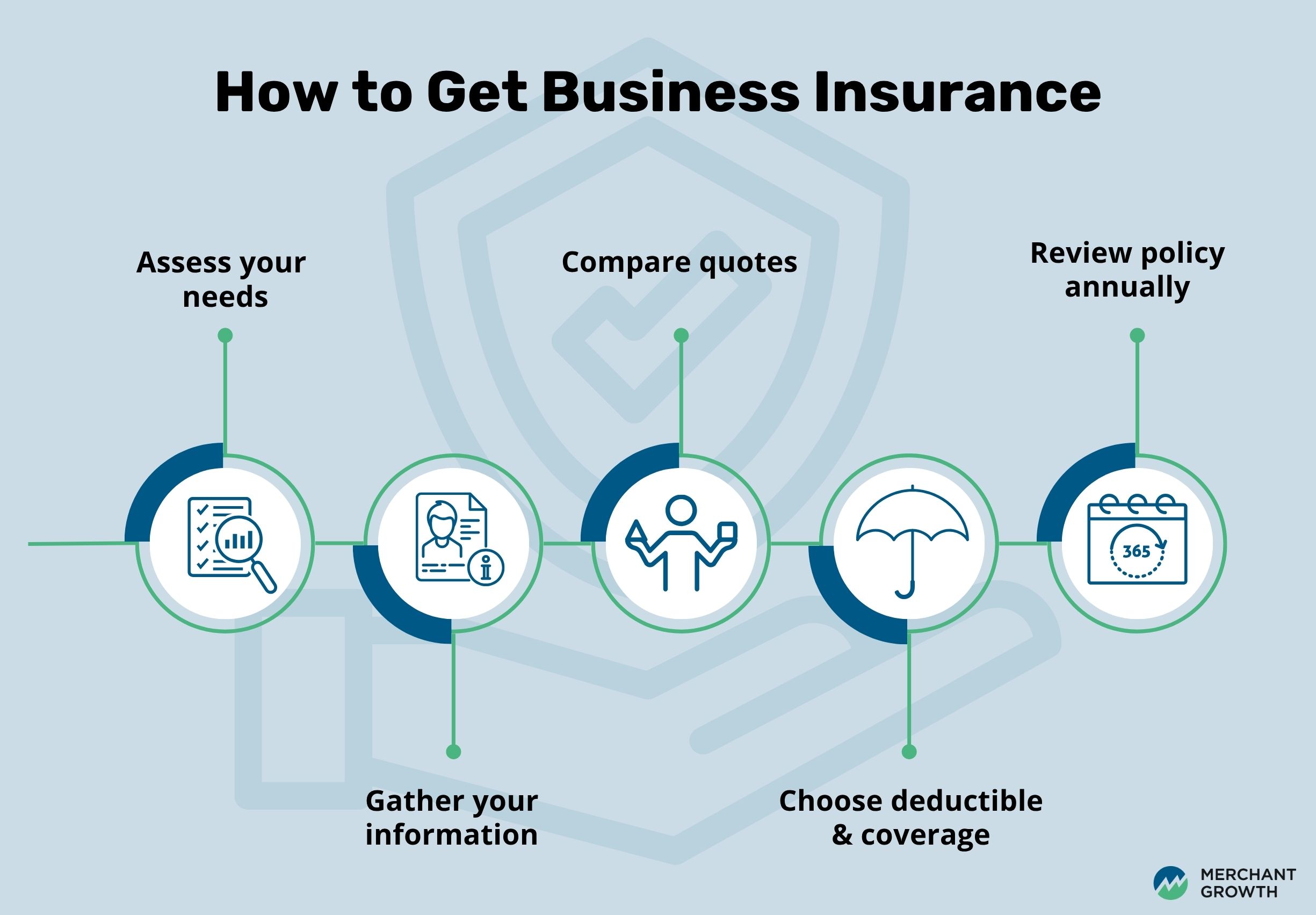

1. Assess Your Needs

Start by identifying the specific risks your business faces. Do you rely on expensive equipment? Interact with clients in person? Store sensitive customer data? Every business has unique vulnerabilities, so this step helps determine which coverage types are essential—whether it’s general liability, cyber protection, or commercial auto insurance.

2. Gather Your Business Information

To get accurate quotes, you’ll need to share basic business details such as your annual revenue, number of employees, business structure, years in operation, and physical location. Insurers use this information to evaluate your risk and determine your premium.

3. Compare Quotes

It’s a good idea to shop around. Use online platforms like TruShield or Mitch Insurance to compare multiple options based on your needs. According to CFIB, 8 in 10 Canadian small business owners used an insurance broker to help them secure the best rate—proof that expert guidance can go a long way in simplifying the process.

4. Choose Your Deductible and Coverage Limits

Your deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in. Your coverage limit is the maximum amount your insurer will pay for a claim. A higher deductible typically lowers your premium but be sure it’s an amount you could realistically pay if something goes wrong. At the same time, ensure your coverage limits are high enough to protect your business assets and liabilities.

5. Review Your Policy Annually

Your insurance needs may evolve as your business grows, expands into new markets, or adds new services. Make it a habit to review your policy at least once a year. This ensures you’re not underinsured—and that you’re not paying for coverage you no longer need.

Tips to Save on Business Insurance

Business insurance is essential, but that doesn’t mean it has to break the bank. There are several smart ways to keep your premiums manageable without sacrificing coverage. By understanding how insurance pricing works and making strategic decisions, you can reduce your costs while still protecting your business.

- Bundle your policies with one provider

- Choose a higher deductible to lower premiums

- Improve your safety protocols to avoid claims

- Avoid filing small claims that may increase future premiums

- Pay annually rather than monthly if cash flow allows

As your business evolves, so should your coverage. Make it a habit to review your policy regularly—especially after major growth, changes in services, or operational shifts—to ensure you’re properly protected without overspending.

What Happens If You Don’t Have Insurance?

No insurance = big risks.

A single lawsuit, fire, or unexpected closure can cost thousands or shut down your business entirely. Beyond financial risk, not having insurance can also limit your ability to sign contracts, lease office space, or hire employees.

What Type of Insurance Does a Small Business Need?

Every business faces unique risks—and that means insurance needs will look different depending on what you do and how you operate. Whether you’re running a café, working as an independent consultant, or selling products online, tailoring your insurance coverage to your business model is key. The right combination of policies can protect you from the most common threats in your industry while keeping your premiums cost-effective.

Here’s a starting point for typical coverage needs by business type:

• Retailers & Restaurants: General liability + property + interruption

• Consultants & Freelancers: Professional liability + cyber

• Trades & Contractors: Liability + tools coverage + commercial auto

• Online Businesses: Cyber insurance + product liability + interruption

Don’t Let the Unexpected Catch You Off Guard

Business insurance isn’t just a safety net—it’s peace of mind that protects everything you’ve worked hard to build. And with some plans starting at just a few dollars a day, the right policy can be one of the smartest investments you make in your business’s future. But costs can add up, especially when premiums rise unexpectedly or cash flow gets tight.

That’s where Merchant Growth can help. Our flexible term financing options are designed to give Canadian small businesses access to fast, reliable funding, without the long approval process or rigid repayment terms of traditional banks. Whether you need extra funds to cover insurance premiums, purchase new equipment, or manage a seasonal dip, our financing solutions are built to support you when it matters most.

Need help managing customer payments, too? Consider offering flexible financing at checkout. With Tabit, our Buy Now, Pay Later solution, you can let customers pay over time, without the hassle of chasing invoices or worrying about late payments. It’s a simple way to improve your cash flow while helping your clients get what they need.

Ready to make your business more resilient? Learn more about how Merchant Growth can help.