10 Best Payment Processors for Small Businesses in Canada

From cafés to contractors, every small business depends on smooth payments. But with so many options and fee structures, finding the right system can be a challenge. The good news is that choosing the right payment processor can simplify your operations, protect your profits, and give customers the fast, secure checkout they expect.

Whether you’re a retailer, restaurant owner, or e-commerce seller, the right system helps you collect payments quickly, reduce errors, and prevent fraud while offering a seamless experience that keeps customers coming back. In today’s competitive market, payment processing isn’t just about transactions; it’s about building trust and ensuring healthy cash flow.

It’s no surprise that Canadian business owners see payment innovation as a key to success. In fact, twenty-four percent of businesses in Canada say it’s extremely important to support their company’s health and growth.

Key Takeaways

- Payment processing is the backbone of smooth, secure transactions for any small business.

- Understanding how payments move — from authorization to payout — helps owners manage costs and avoid delays.

- Comparing processors by fees, features, and security ensures you pick the best fit for your operations.

- The right system can streamline checkout, improve cash flow, and enhance customer trust.

- Canada offers a range of trusted options — from Square and Shopify to Moneris and Helcim.

Why Payment Processing Matters for Small Businesses

That focus on innovation starts with how you handle payments. Beyond simply processing a transaction, an effective system keeps your operations organized and your customers confident that their money is in good hands. A dependable setup ensures funds move smoothly, records stay accurate, and cash flow remains steady.

The scale of digital payments in Canada shows just how vital these systems have become. In 2022, a total of 20.5 billion transactions valued at $11.7 trillion were conducted, reflecting how deeply electronic payments are woven into the country’s business landscape.

For small business owners, every delay or error in getting paid can create ripple effects across daily operations. A reliable payment process helps you manage inventory, pay suppliers on time, and plan confidently for future growth.

It also shapes how customers perceive your business. People expect simple, secure, and flexible ways to pay whether they’re shopping online, in person, or on their phones. Meeting those expectations reinforces trust and leaves a lasting impression.

In essence, effective payment processing supports every part of your business, from back-office efficiency to front-end customer experience.

What Is Payment Processing and Why It’s Essential

As digital payments become the norm, understanding how money moves from your customer to your business has never been more important. In 2022, 40% of Canadians increased their use of digital payment methods, showing just how quickly habits are changing and how vital modern payment systems have become.

Payment processing is the system that makes these transactions possible. It’s the technology that enables your business to accept and settle electronic payments, including credit cards, debit cards, and digital wallets. Every time a customer pays, a network of services works together behind the scenes to transfer funds securely and accurately.

Here’s a quick look at the key players involved:

- Merchant: Your business, which accepts the payment for goods or services.

- Payment Processor: The service that routes transaction information between your customer’s bank and your own.

- Payment Gateway: The secure software that encrypts and transmits payment data for authorization.

- Issuing Bank: The customer’s bank, which provides their credit or debit card and approves the payment.

- Acquiring Bank: Your financial institution, which receives the funds on your behalf.

Together, these players form the backbone of every digital transaction. Understanding their roles helps small business owners make better decisions about which systems to use and how to keep payments running smoothly.

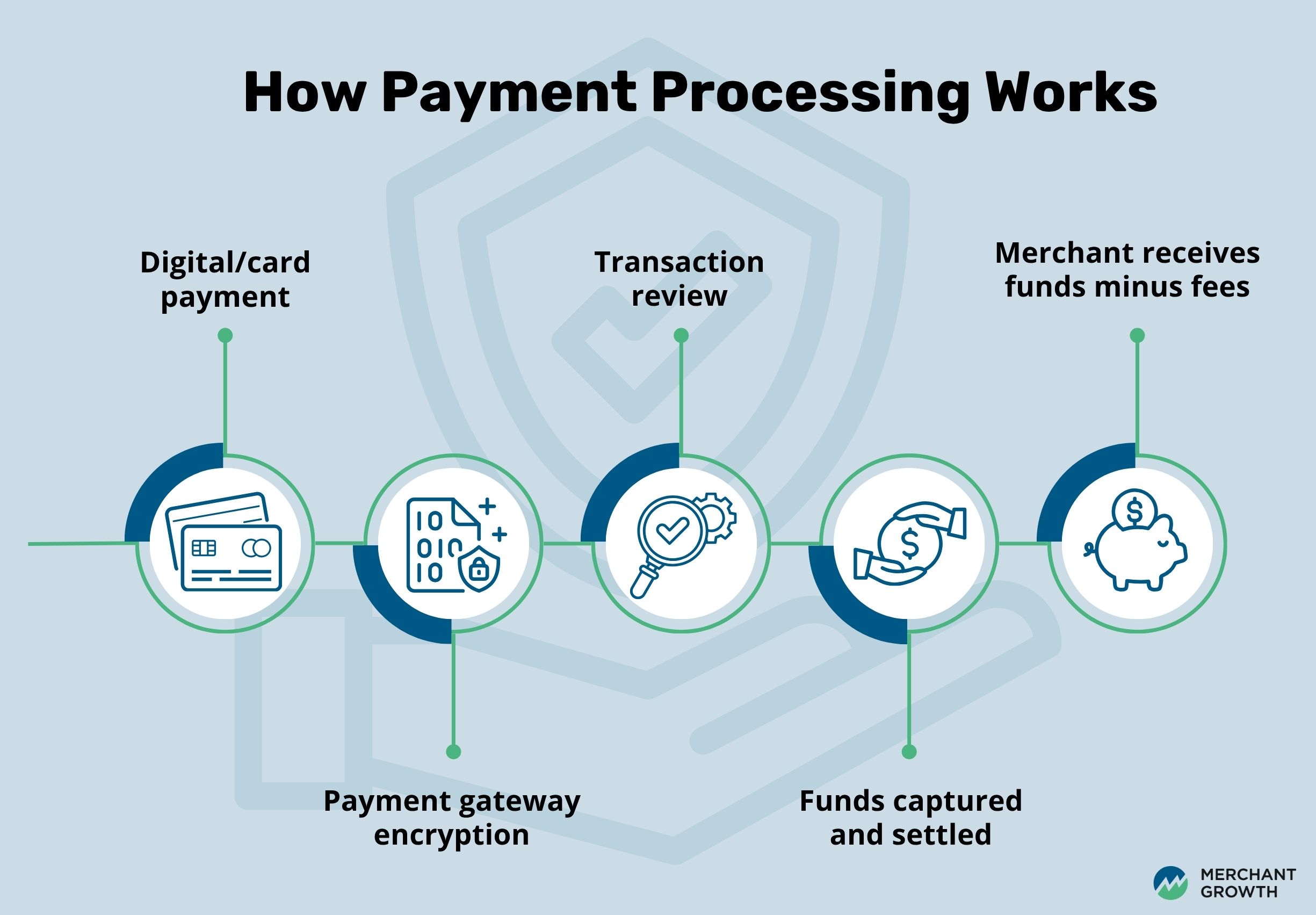

Step-by-Step: How Payment Processing Works

Now that you know who is involved in a transaction, let’s look at what actually happens when a customer makes a payment. Each sale triggers a quick series of steps that work together to move money safely and efficiently from your customer’s account to yours.

- Customer pays using a credit card, debit card, or digital wallet.

- The payment gateway encrypts the information and sends it for authorization.

- The bank or card network reviews the transaction and either approves or declines it.

- Once approved, the funds are captured and settled into the merchant’s account.

- The business receives payment, minus transaction fees and processing costs.

These steps happen in just a few seconds, but having a dependable payment processor ensures everything runs smoothly from start to finish. Knowing how the process works also makes it easier to decide which type of payment system best fits your business needs.

The Different Types of Payment Processing Systems

Now that we’ve walked through how payment processing works, it’s time to look at the different systems that make it happen. The right setup depends on where and how you sell, the kind of experience you want to offer customers, and the tools you already use to manage your business. From in-store point-of-sale systems to online gateways and mobile apps, there’s a solution for every business model.

1. Point-of-Sale (POS) Systems

POS systems are the backbone of in-person transactions. Commonly used in retail stores, cafés, and restaurants, they combine hardware such as card readers and terminals with software that tracks sales, manages inventory, and produces detailed reports. Modern POS systems often integrate with accounting tools and loyalty programs, helping you manage more than just payments. For small business owners, the benefit is having everything in one place, from daily sales to end-of-day reconciliation, without extra manual work.

2. Online and E-Commerce Payment Gateways

For businesses that sell online, payment gateways make digital transactions possible. These systems securely process payments made through your website or app, handling everything from encryption to approval. As online shopping continues to grow, so does consumer comfort with digital transactions. In 2022, 88% of Canadians said they were likely to use a digital payment method in the next year, showing just how critical these systems have become for reaching modern customers. Popular examples include Shopify Payments, Stripe, and PayPal, each offering tools that integrate checkout, subscriptions, and fraud prevention. For e-commerce sellers, choosing a reliable gateway means faster payments, fewer abandoned carts, and stronger customer trust.

3. Mobile Payments

Mobile payments give small businesses the flexibility to accept payments anywhere, whether it’s at a market, a client’s home, or on the job site. Using a smartphone or tablet, you can take payments through tap, chip, or QR code, perfect for service providers, delivery businesses, or mobile vendors. For small businesses, mobile processing is an affordable way to expand where and how you sell while offering customers the convenience they expect.

4. Virtual Terminals

Virtual terminals are ideal for businesses that take payments over the phone or by email. Instead of using a physical card reader, you enter payment details manually into a secure online form. These systems are common among professional service providers, repair companies, or B2B businesses that invoice clients. While virtual terminals may not suit high-volume retail, they provide a simple, secure way to handle remote payments without needing a full e-commerce platform.

5. Integrated Systems

Integrated payment systems bring all your channels together. They connect your in-store POS, online sales, and mobile transactions into a single dashboard so you can track everything in one place. This type of system is especially useful for hybrid or omnichannel businesses that sell both online and offline. By syncing sales, inventory, and reporting automatically, integrated solutions save time, reduce errors, and provide a clear picture of your overall business performance.

Each payment system offers unique advantages, and the best choice depends on your business model, sales channels, and customer preferences. Whether you’re setting up a new online store or upgrading your in-person checkout, understanding these options helps you find a system that fits how you work.

Understanding Payment Processing Fees

For small business owners, every percentage point matters. The fees charged by payment processors may seem small at first glance, but over hundreds or thousands of transactions, those costs can quickly add up. Understanding where each fee comes from helps you compare providers more effectively and avoid surprises on your monthly statements.

Most processors use a combination of different charges, depending on the types of cards you accept, your sales volume, and whether payments happen online or in person. Here’s a closer look at the most common ones.

Interchange Fees

Interchange fees are set by major card networks such as Visa and Mastercard. They’re paid to the cardholder’s bank each time a customer makes a purchase with a credit or debit card. These fees usually represent the largest portion of your overall processing costs and can vary depending on the type of card and how the transaction is made (tap, chip, or online).

Transaction Fees

Transaction fees are the small costs applied to each individual sale. They typically combine a flat amount per transaction, often between 10 and 30 cents, with a percentage of the total sale, such as 2.6 percent. While that might not sound like much, it can add up fast, so it’s important to calculate how these fees will affect your margins over time.

Monthly Fees

Some providers charge a monthly fee for account maintenance or access to advanced features. These might cover customer support, reporting tools, or integrations with accounting software. For smaller businesses with lower transaction volumes, it’s worth comparing whether a provider without monthly fees might be more cost-effective.

Hardware Costs

If you accept in-person payments, you may need equipment such as terminals, card readers, or POS systems. Some providers offer these at a one-time purchase price, while others include them as part of a monthly rental or lease. It’s worth comparing the long-term costs of each option before you commit.

Chargeback Fees

A chargeback occurs when a customer disputes a transaction, and the funds are returned to them while the issue is investigated. Processors typically charge a fee for handling these disputes, which can add up if they happen frequently. Clear refund policies, accurate records, and strong fraud protection can help reduce this risk.

PCI Compliance Fees

Payment Card Industry (PCI) compliance ensures your business meets security standards for handling sensitive customer data. Some processors include compliance in their pricing, while others charge a separate fee to help you maintain it. Even if it’s an extra cost, staying compliant protects your business from much larger losses due to fraud or data breaches.

Tip: Always read the fine print. Some providers bundle fees, while others charge separately for add-ons like currency conversion or cross-border transactions. Comparing total cost of ownership is key.

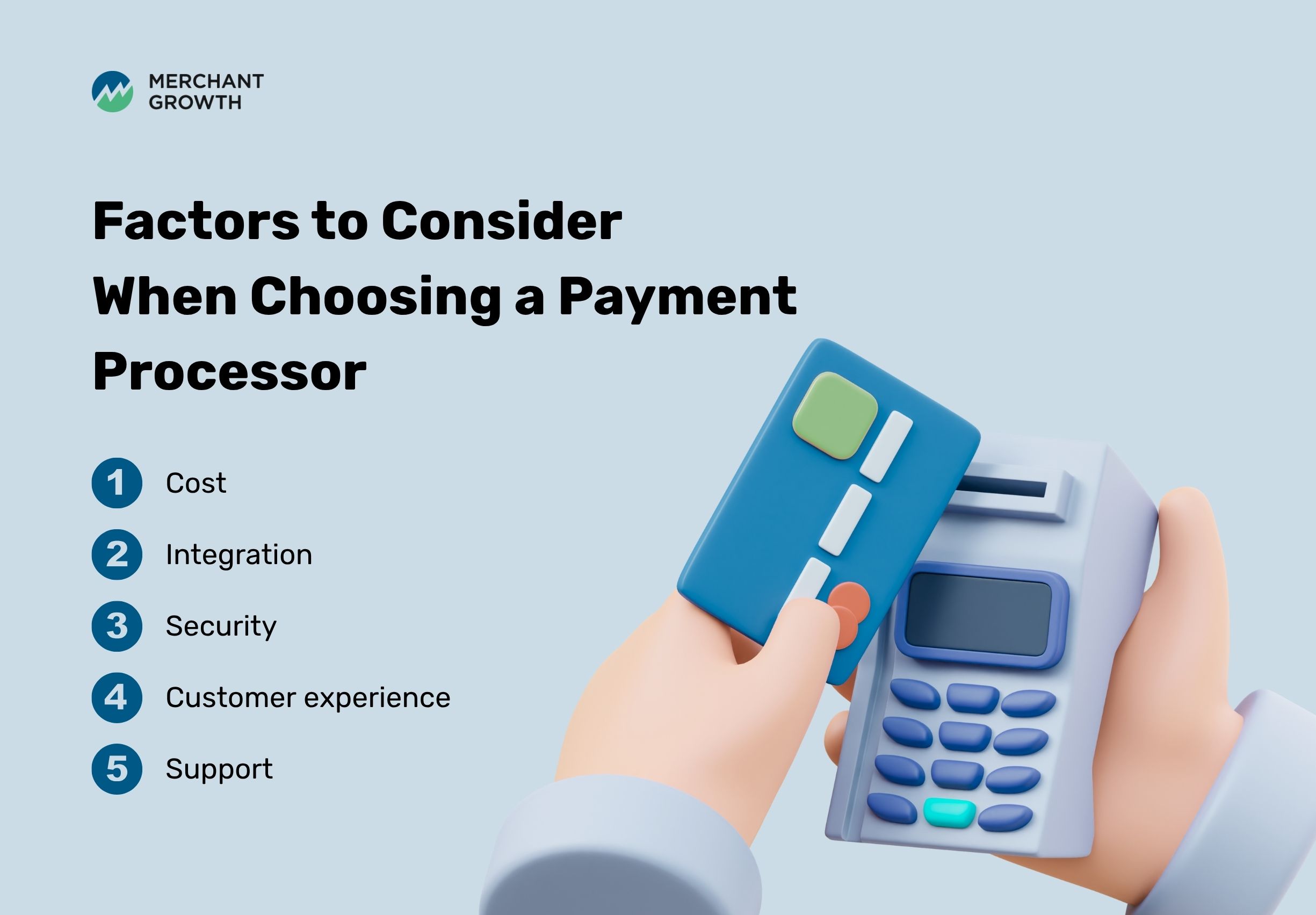

How to Choose the Right Payment Processor

With so many payment processors available, choosing the right one can feel overwhelming. The best option for your business depends on your budget, your sales channels, and how much support or flexibility you need. Once you understand the different fees involved, it’s time to look at the bigger picture and how well each provider fits into your daily operations and long-term goals.

Here’s a simple framework to guide your decision.

Costs

Start by looking closely at all the fees, not just the advertised rate. Review transaction fees, setup costs, monthly charges, and any additional expenses for features like hardware or international payments. Even small differences in rates can add up quickly, so it’s worth calculating your potential monthly total based on your average transaction volume.

Integration

Your payment system should work seamlessly with the tools you already use, such as your POS system, e-commerce platform, or accounting software. Integration saves time, reduces manual data entry, and helps you track sales and revenue more accurately. The more connected your systems are, the easier it is to manage everything from one place.

Security

Security should always be a top priority. Look for processors that are PCI compliant and use strong encryption and fraud detection tools. Protecting your customers’ payment data builds trust and helps safeguard your business from chargebacks and potential breaches.

Customer Experience

A smooth checkout process can make all the difference. Choose a payment system that offers fast, flexible options whether customers are paying in person, online, or through mobile devices. The easier it is for customers to complete their purchase, the more likely they are to come back.

Support

Good customer service can save you time and frustration when things go wrong. Look for providers with reliable, around-the-clock support and clear communication channels. Quick help when you need it most can make all the difference in keeping your business running smoothly.

Pro Tip: Before committing to a contract, try testing the system with a trial or demo account. This gives you a feel for how the platform works and whether it meets your business needs before you make a long-term decision.

The Top 10 Payment Processors for Small Businesses in Canada

Deep Dive: Which Processor Is Right for You?

Choosing a payment processor isn’t one-size-fits-all; it’s about finding the right match for how your business runs. The best option depends on where and how you sell, the size of your business, and the kind of experience you want to offer your customers. Here’s what you should know about the leading choices available to Canadian small businesses.

Square

Square is one of the most popular choices for small businesses because it’s easy to set up and even easier to use. It’s especially well-suited for mobile sellers, pop-up shops, and cafés that need quick, reliable transactions without complex contracts. The company offers transparent pricing, free POS software, and affordable hardware like card readers that connect to your phone or tablet. Square also includes simple analytics and inventory tools, making it an all-in-one option for entrepreneurs who want to start accepting payments right away.

Although Square’s POS software is free to use, it is important to consider the transaction fees associated with each type of payment. As of 2025, Square’s pricing structure is as follows:

Processing Fees for In-Person Transactions

- Credit cards: 2.5% per transaction

- Debit cards: 0.75% plus 7 cents per transaction

Processing Fees for Online Transactions

- Between 2.8% plus 30 cents and 3.3% plus 15 cents per transaction, depending on the payment method

Processing Fees for Remote Transactions

- 3.3% plus 15 cents per transaction

Businesses processing more than $250,000 in annual credit card sales may be eligible for custom pricing. Square also offers advanced features such as detailed reporting, marketing tools, and management integrations, available for an additional monthly fee.

Shopify Payments

If you sell online through Shopify, Shopify Payments is a natural fit. It integrates directly into your store’s checkout, allowing customers to pay seamlessly without leaving your site. This integration also helps lower transaction costs compared to using third-party gateways. For Canadian e-commerce businesses, Shopify’s strong analytics, reporting features, and bilingual support make it an excellent choice for managing both online and in-person sales.

For businesses using Shopify Payments on the Basic plan, processing fees remain competitive and easy to understand. As of 2025, Shopify charges 2.6% per transaction for in-person sales, 2.8% plus 30¢ CAD for online transactions, and a 2% fee when using third-party payment providers. These transparent rates make it simple for small business owners to estimate costs and choose the payment setup that best fits their operations.

Stripe

Stripe is a favourite among online-first businesses and tech-savvy entrepreneurs. Known for its flexibility, it offers a wide range of developer tools and APIs that allow you to customize your checkout experience. Stripe supports recurring billing, subscriptions, and global payments in multiple currencies, making it ideal for digital products, SaaS companies, and international e-commerce stores. While setup may be more technical, the platform’s scalability and automation features make it worth the effort for growing online businesses.

Stripe’s pricing is straightforward and designed to suit a wide range of small businesses. For domestic cards, the standard rate is 2.9% plus 30¢ CAD per successful transaction. Manually entered card payments include an additional 0.5% fee, while international cards incur an extra 0.8% charge. If a currency conversion is required, Stripe applies an additional 2% fee. Businesses with high volumes or unique processing needs can also access custom pricing to better align with their transaction mix and sales model.

PayPal

PayPal remains one of the most trusted names in online payments. It’s simple to set up and easy for customers to use, which helps boost checkout conversions. Many freelancers, service providers, and small online shops prefer PayPal because it doesn’t require a full e-commerce setup. While its transaction fees can be slightly higher than competitors’, the brand recognition and built-in buyer protection add value that many customers appreciate.

As of 2025, PayPal’s domestic transaction fees vary depending on how customers choose to pay. For standard commercial transactions, the rate is 2.9% plus a fixed fee. Payments made using PayPal Pay Later options are charged 4.9% plus a fixed fee. For QR code transactions, the rate is 1.9% plus a fixed fee for payments of $10.01 CAD or more, and 2.4% plus a fixed fee for payments of $10.00 CAD or less. These options give small business owners flexibility in how they accept payments while maintaining transparency around processing costs.

Moneris

Moneris is one of Canada’s largest payment processors, jointly owned by RBC and BMO. It offers dependable service and a wide range of hardware options for in-person payments, including terminals and POS systems. Moneris is a great choice for established brick-and-mortar businesses that value local support and the credibility of a bank-backed provider. However, it often requires a term contract and may have higher fees than more flexible options.

Moneris provides flat rate pricing options designed to keep transaction costs simple and predictable for fast-growing startups and small Canadian businesses. For in-person payments via a POS terminal or card reader, Moneris offers a rate of 2.65% plus $0.10 per successful credit-card transaction, and $0.10 for successful Interac® debit payments. For online or card-not-present transactions (such as payments made via a website or phone), the rate sits at 2.85% plus $0.30 per credit-card transaction, with Interac debit set at $1.00 per transaction.

Helcim

Helcim is a proudly Canadian company known for its transparent, interchange-plus pricing and excellent customer service. It’s an especially strong choice for cost-conscious businesses that want clear, predictable rates. Helcim supports both online and in-person payments, with built-in invoicing, recurring billing, and reporting tools. It’s a trusted option for small and midsize businesses that want fair pricing without hidden fees.

Helcim takes a unique and transparent approach to payment processing by adjusting fees based on the amount of credit card sales a business processes each month. This tiered pricing model rewards growth by lowering rates as transaction volumes increase. For in-person payments, rates start at interchange plus 0.40 percent and 8 cents per transaction for businesses processing up to $50,000 per month. As sales grow, fees gradually decrease to 0.35 percent plus 7 cents $50,000 and $100,000, 0.25 percent plus 7 cents for amounts between $100,000 and $500,000, 0.20 percent plus 6 cents for amounts between $500,000 and $1 million, and 0.15 percent plus 6 cents for businesses processing over $1 million monthly. This structure makes Helcim especially attractive for small businesses that expect to scale, since costs naturally become more competitive as sales increase.

Clover

Clover stands out for its sleek POS hardware and robust management features. It’s ideal for restaurants, cafés, and retail stores that need an all-in-one system for processing payments, tracking sales, and managing staff. Clover’s terminals come with user-friendly software that syncs easily with accounting and inventory systems, helping streamline day-to-day operations.

Clover offers straightforward pricing for its basic payment package, making it easy for small business owners to estimate costs. For in-person transactions where a card is tapped, swiped, or inserted, the rate is 2.5 percent plus 10 cents per transaction. For payments where card details are manually entered, the fee increases to 3.5 percent plus 10 cents per transaction. This simple structure allows businesses to manage costs effectively while taking advantage of Clover’s intuitive hardware and built-in business management tools.

Scotiabank’s Chase Payment Solutions

Scotiabank’s Merchant Services program, powered by Chase Payment Solutions, offers Canadian businesses a seamless, full-service solution for accepting payments in-store, online, or on the go. With this partnership, businesses get access to Scotiabank’s trusted banking services combined with Chase’s payment-processing infrastructure. The service supports next-business-day deposits into a Scotiabank account, advanced reporting through the Chase Commerce Centre, and 24-hour bilingual support. This makes it an excellent choice for businesses looking for a reliable, integrated banking and merchant services solution in Canada.

When it comes to pricing, Chase Payment Solutions offers transparent and competitive rates for Canadian merchants. The terminal fee is $34.95 per month for each terminal with a charging base. For credit card transactions, businesses pay 2.45 percent per transaction on contactless, swiped, or card-inserted payments, and 2.75 percent per transaction for manually keyed-in transactions. Interac Debit card fees are set at 8 cents per sale transaction and 11.5 cents per contactless transaction. These straightforward rates make it easier for small business owners to anticipate costs while benefiting from fast deposits, reliable hardware, and the backing of two trusted financial institutions, Scotiabank and Chase.

Lightspeed

Founded in Canada, Lightspeed is a strong option for retail and hospitality businesses that want a fully integrated system. It combines POS functionality with inventory management, staff scheduling, and customer insights. Because it’s cloud-based, you can access your data anytime and from anywhere, which is particularly helpful for multi-location operations. Lightspeed’s local roots and strong customer support make it a reliable choice for Canadian businesses.

Lightspeed Payments offers a competitive rate for card-present transactions at 2.6 percent plus 10 cents per transaction on its basic plan. While its pricing information can be a little harder to locate compared to other providers, Lightspeed remains a popular choice for businesses that want advanced POS functionality. The platform’s monthly software costs are on the higher end, but the system’s powerful tools for inventory tracking, reporting, and employee management make it a strong option for retailers and restaurants looking for an all-in-one solution that integrates payments with everyday operations.

Global Payments

Global Payments specializes in supporting larger or high-volume businesses that operate internationally. It provides multi-currency processing and advanced reporting tools, helping businesses manage cross-border transactions with ease. While it’s typically used by bigger companies, some small businesses choose Global Payments for its reliability and wide range of services.

Each processor has its own strengths, and the right one will depend on your sales model, budget, and customer needs. Whether you value transparency, flexibility, or advanced integrations, understanding your options helps you choose with confidence.

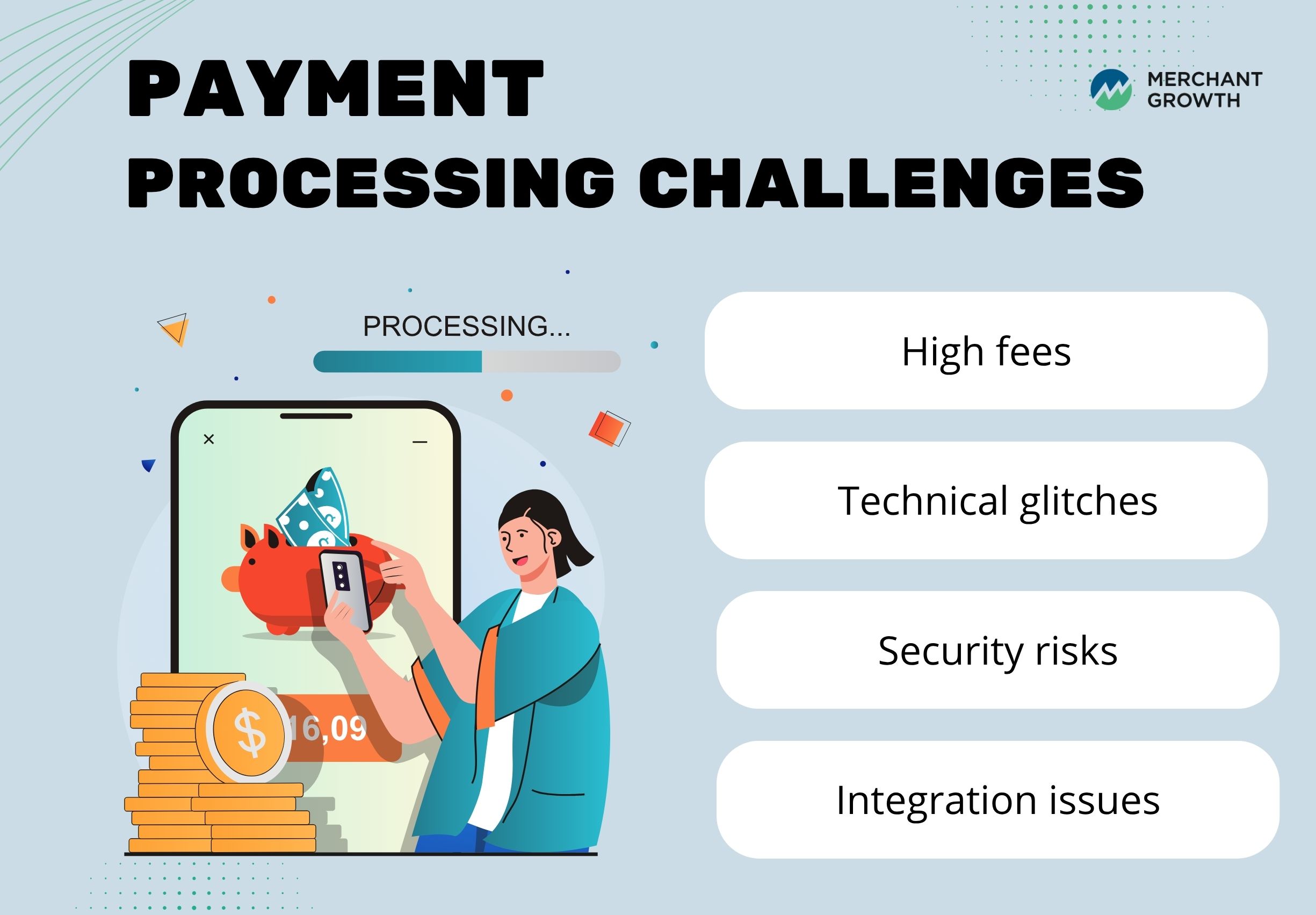

Overcoming Common Payment Processing Challenges

Even with the right payment system in place, small businesses often run into a few common roadblocks. From unexpected fees to technical hiccups, these challenges can slow down operations and affect cash flow. The good news is that most issues can be solved or even prevented with a bit of planning and the right partner.

High Fees

Processing costs are one of the biggest frustrations for small business owners. Fees can vary widely between providers, so it pays to compare your options carefully. Look at the full picture, including interchange, transaction, and monthly fees. Do not hesitate to negotiate, especially if your business has a steady sales volume. Many providers are willing to offer lower rates to keep a reliable client.

A smart strategy is to look for interchange plus pricing, which breaks down exactly what portion of each fee goes to the card network versus the processor. This model is often more transparent and can help you save money over time.

Technical Glitches

Few things are more stressful than a system outage when customers are ready to pay. Choose a processor known for reliable uptime and responsive customer support. It is also wise to have a backup payment option, such as a mobile reader or virtual terminal, so you can continue serving customers even if your main system experiences an issue.

Regularly updating your software and hardware can also help prevent technical problems before they start.

Security Risks

Protecting customer data is critical. A single security breach can damage trust and cost a business thousands of dollars. Always use processors that are PCI compliant and offer tools for encryption, tokenization, and fraud detection. Encourage your staff to follow best practices for handling card data, such as never writing down customer information or storing it unencrypted.

Staying vigilant and compliant not only protects your customers but also builds confidence in your brand.

Integration Issues

Many small businesses use several different systems for accounting, inventory, and sales. When these tools do not communicate with each other, it can lead to extra manual work and errors. Choosing a processor that integrates with your existing POS or e-commerce platform makes life much easier.

If you are expanding your business, look for payment systems that scale with you and can add new integrations as your operations grow. Seamless connections between your tools save time and keep your financial data accurate.

FAQs About Payment Processing

What’s the difference between a payment gateway and a processor?

A gateway securely transmits card data; the processor actually handles the transaction and funds transfer.

How long does it take to receive funds after a sale?

Usually within 1–3 business days, depending on your provider and bank.

Are there hidden fees I should watch for?

Yes, look for PCI, batch, or early termination fees in contracts.

What’s PCI compliance, and why does it matter?

It’s a security standard protecting customer payment data — essential for preventing fraud.

Can I use more than one payment processor?

Yes. Many businesses use different systems for in-person and online sales.

How Merchant Growth Supports Canadian Businesses

Choosing the right payment processor is just one piece of building a successful business. The next step? Making sure you have the capital to grow.

Merchant Growth helps Canadian small businesses fund essential upgrades, from new POS systems to expanded inventory and marketing. Whether you’re opening a second location or modernizing your checkout, Merchant Growth can help finance the next stage of your success.

Talk to Merchant Growth today to learn how easy, flexible financing can keep your business and your payments running smoothly.