How to Start a Small Business in Canada: A Step-by-Step Guide for Entrepreneurs

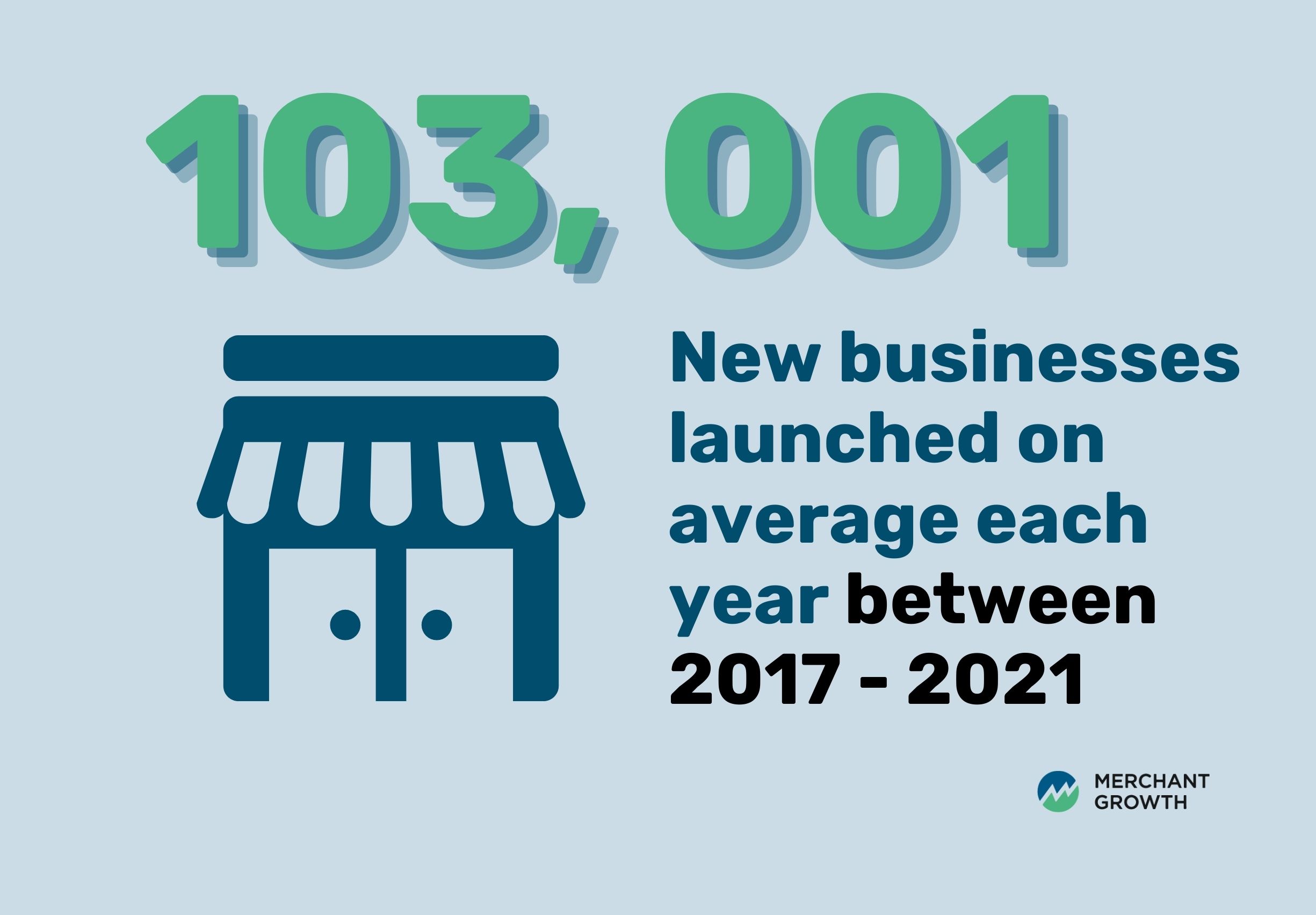

Thinking about starting a small business in Canada? You’re in good company. Between 2017 and 2021, an average of 103,001 new small businesses were launched each year, showing that Canadians are constantly turning ideas into reality.

Of course, starting a business comes with its challenges—figuring out the right idea, understanding your customers, navigating regulations, and finding the funding to get off the ground. That’s exactly what this guide is here for. Step by step, we’ll walk you through everything you need to know to start your small business, from shaping your idea and planning your budget to registering your business, securing funding, and launching with confidence. With practical tips and real Canadian resources along the way, you’ll have the roadmap you need to turn your vision into a thriving business.

Key Takeaways

- Business Planning: A detailed plan maps your goals, strategy, and finances, and serves as a guide for decision-making.

- Business Registration: Choosing a name and registering your business legally is crucial for compliance and credibility.

- Licensing & Permits: Ensure you have all the required licenses to operate without interruptions.

- Funding Options: Grants, loans, and alternative financing options can provide the capital you need to start strong.

- Growth Strategy: Budgeting for future growth ensures you can scale without financial stress.

How to Start a Small Business in Canada

Turning your business idea into a reality takes more than passion—it takes planning, smart decisions, and a clear roadmap. Canada offers plenty of resources to help new entrepreneurs, but you’ll still need to navigate things like choosing the right business structure, understanding regulations, managing taxes, and securing funding. Let’s break down each step in a practical, easy-to-follow way, starting with understanding your market and finding the right audience for your product or service.

Conduct Market Research

Before investing time and money, understanding your market is critical. Market research helps identify who your ideal customers are, what they need, and how your business can meet those needs better than competitors. Let’s look at four simple ways you can dig into the market and gather the insights you need to make smart decisions.

Understand Your Target Audience:

Start by getting clear on who you’re trying to serve. Think beyond just age and gender—consider lifestyle, habits, motivations, and pain points. Create a simple customer profile or persona:

- Who are they?

- What problems do they face that your business can solve?

- Where do they spend their time online and offline?

Once you have this profile, you can tailor your marketing, product development, and even pricing to match their expectations. Tools like surveys, social media polls, or even casual conversations with potential customers can give you real insight into what they want.

Analyze Competitors:

Understanding your competition is more than knowing their prices—it’s about uncovering their strengths and weaknesses. Look at local businesses and online competitors offering similar products or services. Check their websites, read customer reviews, follow them on social media, and see what people like or dislike about them. Take notes on their marketing approach, customer experience, and product offerings. The goal isn’t to copy them, but to find ways to differentiate your business and offer something uniquely valuable.

Identify a Gap in the Market

Once you understand your target audience and your competitors, the next step is spotting opportunities where your business can stand out. Look for areas where competitors’ products or services don’t fully meet customer needs—maybe they’re inconvenient, outdated, or missing features that your audience wants.

Ask yourself:

- What are customers frustrated with in current offerings?

- Is there a way to make a product or service simpler, faster, or more enjoyable?

- Are there groups of people whose needs aren’t being addressed at all?

Pinpointing these gaps gives your business a competitive edge and increases the chances of success. By offering something unique that solves real problems, you’re not just entering the market—you’re filling a space that customers have been waiting for.

Stay Updated on Industry Trends:

Markets are always changing, and staying ahead of trends can give your business an edge. Subscribe to industry newsletters, follow key influencers, and check government or trade association reports for insights. For example, the Government of Canada offers industry-specific data and reports that can help you spot opportunities or potential challenges in your sector. By understanding trends, you can anticipate customer needs, adapt your offerings, and make more informed strategic decisions

Use Reliable Data:

There’s nothing like hearing straight from your potential customers. Try informal methods like chatting with people in your target market, conducting interviews, or sending out short surveys. Online platforms like Google Forms, Typeform, or social media polls make it easy to gather feedback quickly. Pay attention to recurring themes or concerns—these can guide everything from product design to pricing and marketing. The more you understand your audience from their own perspective, the better positioned your business will be to serve them effectively.

Conducting thorough market research ensures your business idea is viable and gives you the insights needed to make informed decisions. With a clear understanding of your customers, competitors, and industry trends, you’re ready to take the next step: planning your business and turning those insights into a concrete strategy for success.

Plan for Your Business

A solid business plan isn’t just a document—it’s your roadmap for turning an idea into a thriving business. It helps you clarify your vision, map out financial projections, and plan operational strategies. Most importantly, it gives you the confidence to make informed decisions and shows potential investors or lenders that you’ve thought things through. Let’s break down the first steps to building your business plan and shaping your idea into something real.

Coming Up with a Business Idea:

Every successful business starts with a strong idea, but not every idea is ready to become a business. Start by thinking about your skills, passions, and the needs you see in the market. Ask yourself:

- What problems can I solve?

- What gaps exist that my business could fill?

Once you have a few ideas, test them by talking to potential customers, getting feedback, and refining your concept. The goal is to land on an idea that excites you and has a clear market demand.

Choosing a Location vs. Working from Home:

Where your business operates can have a big impact on costs, accessibility, and customer reach. If you need foot traffic or local visibility, a physical storefront might make sense—but it comes with higher overhead. Running a business from home can reduce costs, but you’ll need to think creatively about reaching customers online or delivering your services. Consider a hybrid model or co-working spaces if you want flexibility while keeping some professional presence.

Deciding Between Employment Models

Before hiring anyone or setting your own role, think about how you want your business to operate. Do you plan to hire full-time staff, rely on contractors, or manage everything as a solo entrepreneur? Each option has implications for taxes, benefits, and operational workload. Map out the responsibilities and decide which model makes sense now—and how it might evolve as your business grows.

Set Goals:

Before you dive into writing your business plan, it’s important to get clear on your goals. Short-term goals—like landing your first customers or launching your website—help you focus on immediate priorities, while long-term goals—like reaching revenue milestones or expanding your offerings—give your business direction and purpose.

Make your goals SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of “I want more customers,” try “I want 50 new customers in the first six months through social media and local events.” Clear goals make your plan actionable and give you a roadmap for measuring progress as your business grows.

Writing Your Business Plan

Now it’s time to pull everything together into a cohesive plan. Your business plan should outline:

- Your business concept and goals

- Market research and target audience

- Marketing and sales strategies

- Operational plan and staffing

- Financial projections and budget

Be as detailed as possible, but keep it clear and readable. Remember, your plan is meant to guide you, not overwhelm you.

Pro Tip: To make this process easier, you can use our own business plan template—designed specifically for Canadian entrepreneurs—to structure your ideas and build a plan that’s ready for funding, growth, and long-term success.

Choosing Your Business’s Name

Your business name is often the first thing customers notice, so it’s worth taking the time to get it right. A great name captures what your business stands for, is easy to remember, and sets you apart from the competition. Let’s break down how to choose a name that works for your brand.

Brainstorm Meaningful Names:

Start by thinking about what your business represents and what makes it unique. Consider your products, services, target audience, and brand personality. Don’t be afraid to get creative—sometimes the best names come from wordplay, metaphors, or combining ideas. Write down everything that comes to mind, then narrow the list based on which names are memorable, clear, and resonate with your customers.

Check for Availability:

Once you have a shortlist, it’s crucial to make sure your name isn’t already taken. In Canada, you can use the NUANS database to check if your desired business name is registered or too similar to existing businesses. If your name is already in use, try slight variations or add a descriptive term that highlights what your business does. This step protects you from legal headaches and ensures your brand can stand out.

Consider Online Presence:

A business name is only as good as your ability to promote it. Check if the domain name is available for a website and whether social media handles match your name. Even if you’re starting small, securing your online identity early can save you headaches later and make marketing easier as your business grows.

Choosing the right name takes time, but it’s an investment that pays off in brand recognition and credibility. With a strong name in place, you’re ready to move on to picking the right business structure, which sets the foundation for your legal, tax, and operational decisions.

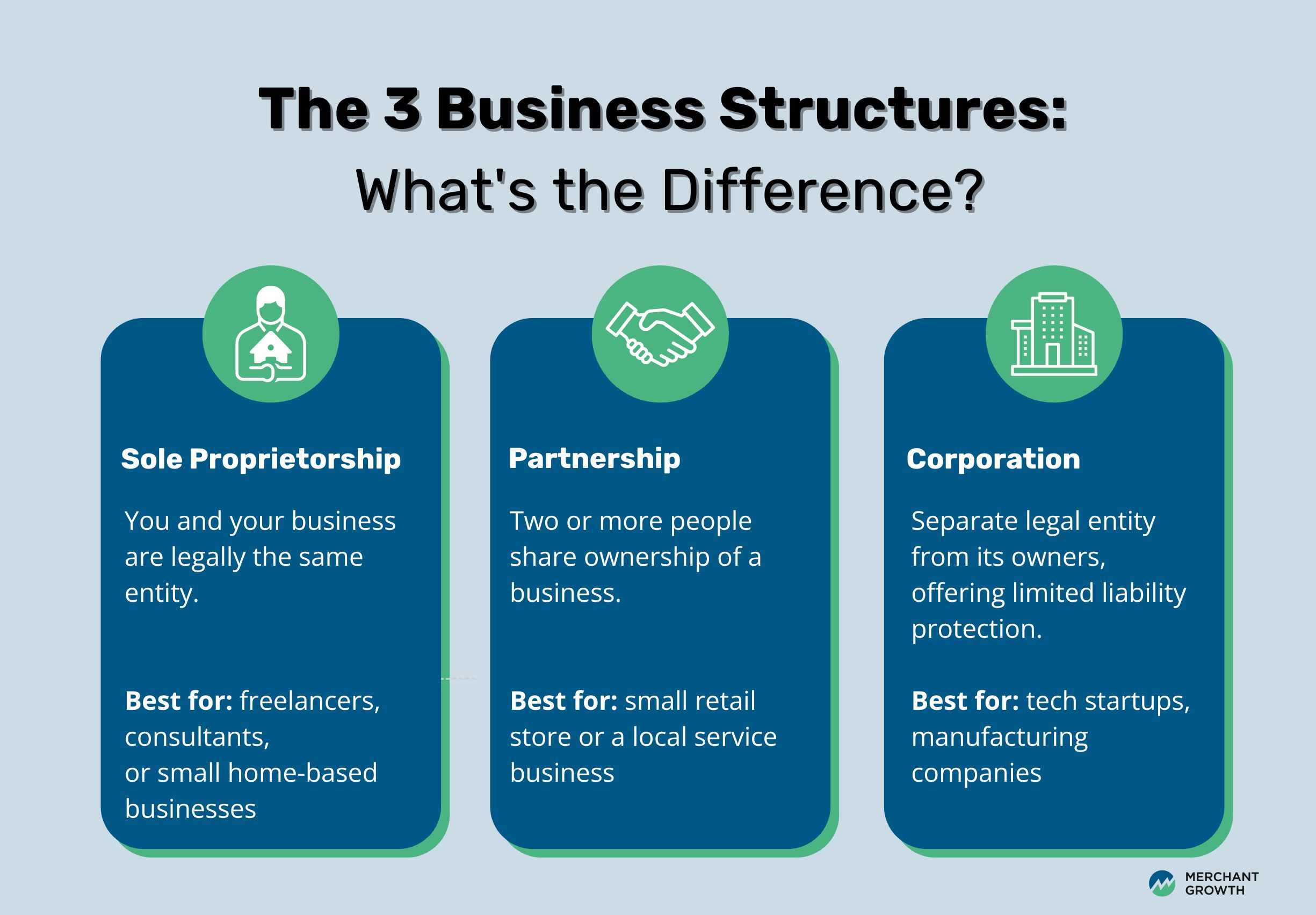

Select the Appropriate Business Structure

Choosing the right business structure is more than a formality—it shapes your taxes, liability, and day-to-day responsibilities. Picking the right model from the start can save you money, simplify operations, and protect you legally. In Canada, there are three main options:

Sole Proprietorship:

A sole proprietorship is the simplest and most common structure for small businesses. You and your business are legally the same entity, which means you report income on your personal tax return and have full control over decisions. The main trade-off is personal liability: if your business runs into debt or legal trouble, your personal assets are on the line.

This model works best for freelancers, consultants, or small home-based businesses just getting started. It’s easy to set up, low-cost, and gives you full control, making it perfect for solo entrepreneurs who want to test their ideas with minimal risk.

Partnership:

A partnership is when two or more people share ownership of a business. Partners share responsibility for decisions, profits, and debts. Partnerships can be general (where everyone is equally responsible) or limited (where some partners have limited liability).

This structure works well when you have trusted business partners and complementary skills. For example, a small retail store or a local service business might benefit from pooling expertise and resources. Clear agreements are essential to outline roles, responsibilities, and how profits are shared.

Corporation:

A corporation is a separate legal entity from its owners, offering limited liability protection. This means personal assets are generally safe if the business faces legal or financial challenges. Corporations also have potential tax advantages and can make it easier to raise investment capital.

Corporations are ideal for businesses with growth ambitions, like tech startups, manufacturing companies, or businesses looking to attract investors. Keep in mind that corporations involve more paperwork, legal compliance, and ongoing reporting requirements than other structures, so they’re best for those ready to commit to the extra effort.

Each structure has different tax and legal implications, so it’s worth reviewing your options carefully. The Canada Business Network offers detailed guidance to help you decide which structure fits your business goals.

Registering Your Business

Now that you’ve picked a business name and chosen your structure, you’re ready to make it official. Legal registration is a critical step—it ensures your business is recognized by the government, can open bank accounts, enter into contracts, and access funding. Thankfully, you’ve already completed some of the groundwork with the decisions you made in the previous steps, which makes the registration process much smoother.

- Decide on your business name

- Choose your structure (sole proprietorship, partnership, corporation)

- Register your business federally or provincially using the Canada Business Registrations Portal

- Keep copies of registration documents for tax and legal purposes

Once you start the online registration, you’ll notice the process is fairly straightforward but still requires careful attention. You’ll enter details about your business, confirm your structure, and submit your chosen business name for approval. Depending on your location and the type of registration, the process can take anywhere from a few hours to a few days, especially if you need name approval or additional permits. Most of the time, you can complete everything online through the Canada Business Registrations Portal, but having all your information ready in advance—like your structure, business address, and ownership details—will make the process much smoother.

Registering your business officially is a milestone: it turns your idea into a legal entity, sets the stage for growth, and opens the door to funding, banking, and other essential services.

Business Licenses and Permits

Once your business is legally registered, the next step is ensuring it meets all the rules and regulations that apply. Depending on your industry, location, and the services you provide, you may need one or more licenses or permits to operate legally. These aren’t just bureaucratic hurdles—they protect your business, your customers, and your employees, while keeping you compliant with the law. Let’s break down the main types of permits and licenses you might need in Canada, and where to obtain them.

Municipal or City Licenses

Municipal licenses are issued by your city or town and are required to operate within a specific municipality. They ensure that your business meets local zoning and safety regulations.

Examples: A retail shop, daycare, or hair salon typically needs a municipal business license.

Obtaining a municipal license: Visit your city or town’s business licensing office or website to review requirements and submit applications. Many municipalities allow online applications, which can simplify the process.

Health and Safety Permits

If your business involves handling food, providing healthcare services, or offering personal care services, you’ll need health-related permits to ensure your operations meet provincial or federal health regulations.

Examples: Restaurants, food trucks, tattoo studios, and physiotherapy clinics all require specific health permits.

Obtaining health permits: Contact your provincial health authority or local public health office for guidance on the necessary inspections, certifications, and compliance steps.

Specialized Industry Permits

Certain industries are more heavily regulated and require additional specialized permits to operate. These can include environmental, construction, retail, or childcare permits, depending on the business type.

Examples: Construction companies may need building permits, retail stores may need alcohol or tobacco licenses, and childcare centers require provincial approvals.

Obtaining specialized permits: Check with the relevant provincial or federal department overseeing your industry. Tools like BizPaL can help identify exactly which permits are required for your business.

Federal Permits and Licenses

Some businesses require federal-level permits, especially if they involve transportation, broadcasting, banking, or interprovincial operations.

Examples: Import/export companies, financial services, or national delivery services.

Obtaining federal permits: These are issued by specific federal departments. Start with the Canada Business Network or BizPaL to determine which federal agency administers the required permits for your business.

Navigating licenses and permits might feel overwhelming at first, but having them in place is essential for smooth operations and avoiding fines or shutdowns. With your business registration complete, you now have the foundation to identify exactly what you need and apply efficiently.

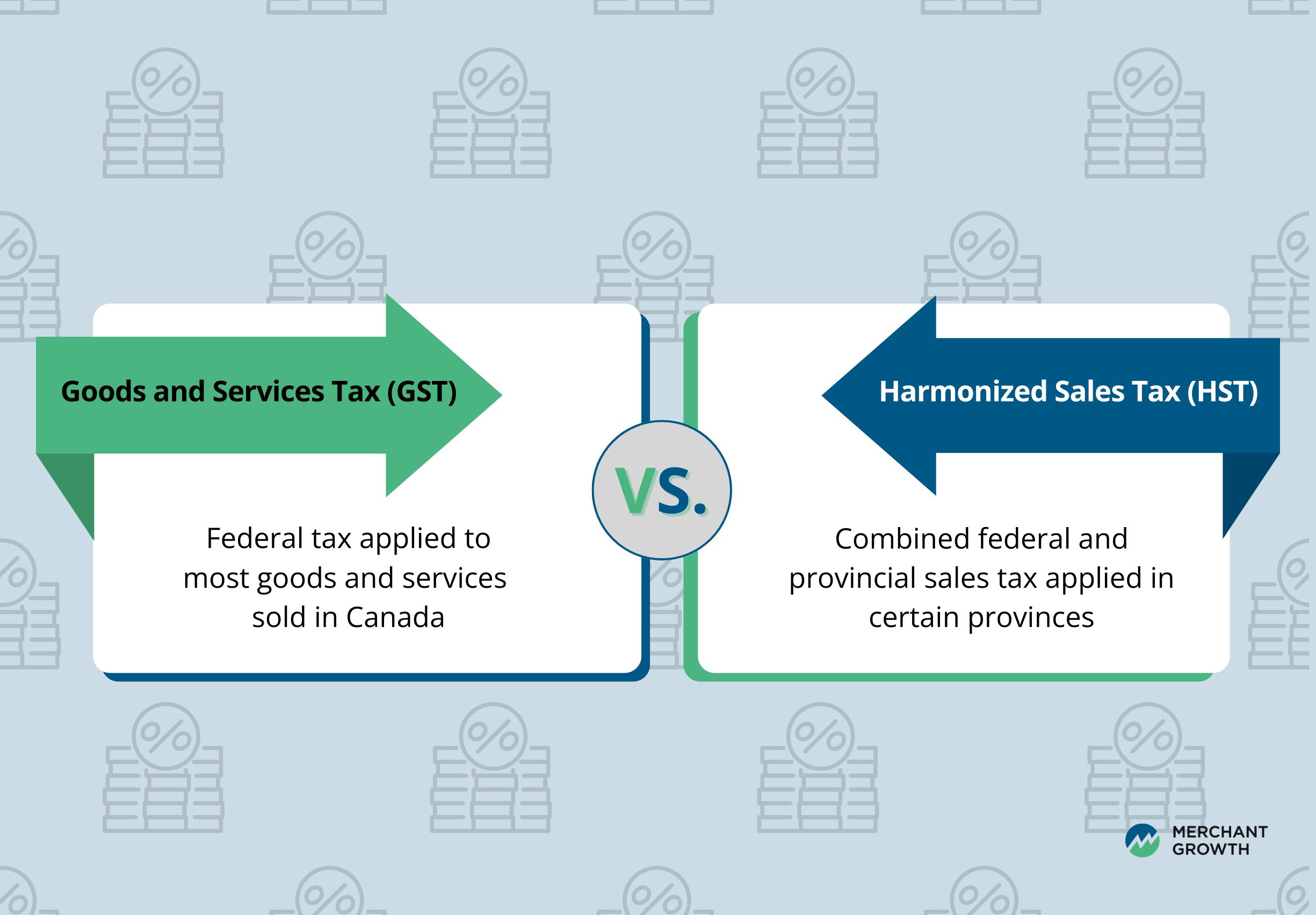

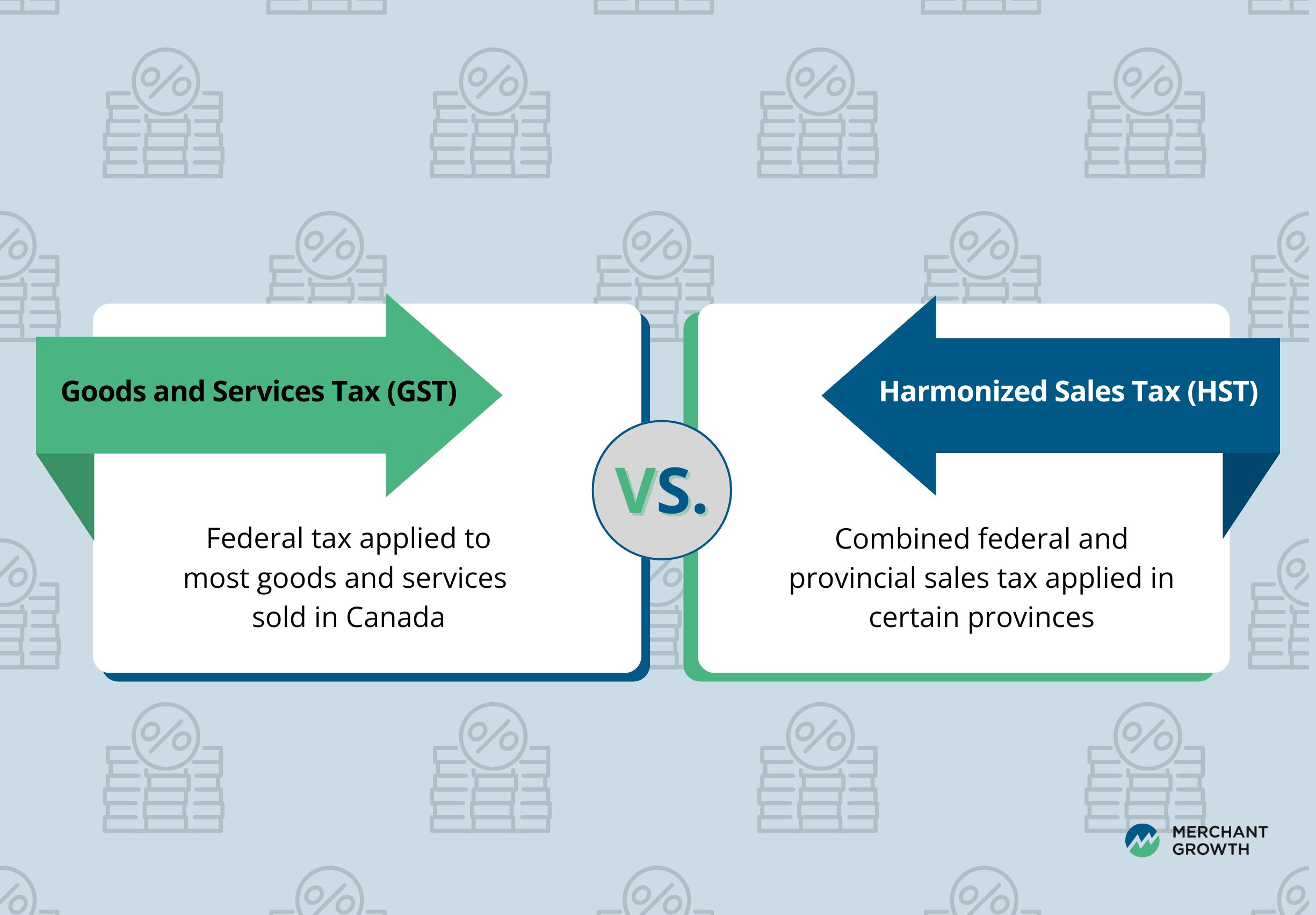

GST/HST Registration

When you start a small business in Canada, understanding taxes early is crucial. If your business generates more than $30,000 in annual revenue, you’re required to register for GST (Goods and Services Tax) or HST (Harmonized Sales Tax). Registering ensures you comply with federal and provincial tax laws and can claim input tax credits on business expenses.

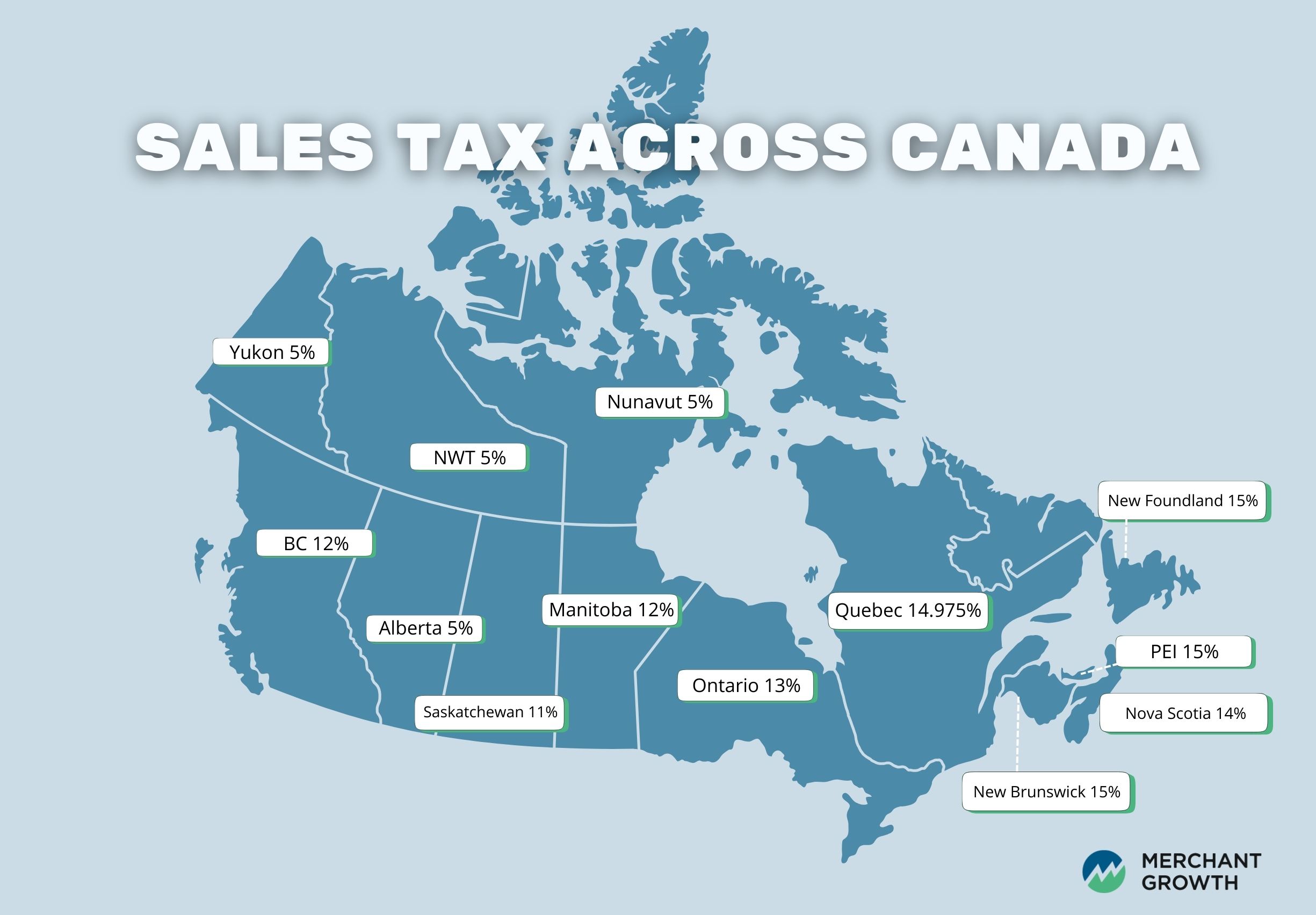

Understanding GST and HST

GST (Goods and Services Tax): A 5% federal tax applied to most goods and services sold in Canada.

HST (Harmonized Sales Tax): A combined federal and provincial sales tax applied in certain provinces, replacing the separate GST and provincial sales tax. The HST rate varies depending on the province:

| Province | HST Rate |

|---|---|

| Ontario | 13% |

| New Brunswick | 15% |

| Newfoundland and Labrador | 15% |

| Nova Scotia | 14% |

| Prince Edward Island | 15% |

Provinces not listed above (e.g., British Columbia, Manitoba, Saskatchewan, Quebec) charge GST at 5% plus separate provincial sales tax (PST) where applicable. Here is a breakdown of PST for the applicable provinces:

| Province | PST Rate |

|---|---|

| British Columbia | 7% |

| Manitoba | 7% |

| Quebec | 9.975% |

| Saskatchewan | 6% |

Alberta, Northwest Territories, Nunavut and the Yukon all simply charge GST for a sales tax rate of 5% total. Understanding the right tax rate for your location ensures you charge customers correctly and remain compliant.

How to Register and File Your GST/HST

Getting started with registration: The easiest way to register for GST/HST is through the Canada Revenue Agency’s Business Registration Online portal. You’ll need your business number, legal business name, and contact information. Registration is straightforward and usually completed within a few minutes online.

Filing your returns:

Once registered, you’ll need to collect GST/HST from customers and submit periodic returns to the CRA. Most small businesses file either quarterly or annually, depending on revenue and preference. Filing can be done through CRA’s online services, by mail, or through your accounting software if it supports GST/HST reporting. Keeping accurate records of all sales and expenses will make filing much easier and help ensure you claim eligible input tax credits to reduce your net tax payable.

Registering for GST/HST might feel like a big step, but once in place, it’s simply a part of your ongoing financial routine—and one less worry as you focus on growing your business.

Budgeting for Your Business & Future Growth

A budget is more than just numbers on a spreadsheet—it’s a tool that keeps your business financially healthy and helps you make smart decisions. Without a clear picture of your income and expenses, it’s easy to overspend, miss opportunities, or struggle when unexpected costs pop up.

Start with Startup and Operating Costs

Begin by outlining all your startup costs (equipment, inventory, marketing, website development, and any professional fees. Then, factor in ongoing expenses like rent, utilities, payroll, insurance, and supplies. Being thorough here helps you understand exactly how much you need to get your business off the ground and keep it running smoothly.

Plan for Growth and Unexpected Expenses

Budgeting isn’t just about today—it’s about tomorrow. Set aside funds for unexpected expenses, like equipment repairs or temporary drops in revenue, and think ahead to future growth. Whether you plan to expand your product line, hire additional staff, or open a new location, incorporating these plans into your budget ensures you’re ready when opportunities arise. For more guidance, check out our business budgeting template and article on planning for expansion—they’ll help you map out both short-term and long-term goals.

Staying on Top of Your Budget

A budget is only useful if it’s actively managed. Track your income and expenses regularly using tools like QuickBooks Canada or Wave Accounting, and review your budget at least monthly. Compare your projections to actual spending to spot trends, adjust your forecasts, and make informed decisions. Small adjustments now can prevent bigger problems later.

Budgeting might sound tedious, but it gives you confidence. When you know where your money is going and how to plan for growth, you can focus on what matters most: building a business that thrives.

Be Aware of Tax Requirements

Budgeting and managing cash flow go hand in hand with understanding your tax obligations. Taxes can feel complicated, but getting a handle on them from the start will save you time, stress, and potential penalties. Knowing what you owe, when to pay, and what deductions you can claim helps keep your business financially healthy and compliant.

Filing Obligations

How often you file your taxes depends on both your business structure and your annual revenue:

- Sole Proprietorships and Partnerships: Generally file once a year along with your personal income tax, but GST/HST filings depend on revenue. Small businesses under $30,000 annual revenue can usually file annually, while those above may need to file quarterly or monthly.

- Corporations: Must file a corporate tax return every year, regardless of income. Larger corporations may have additional installment payments throughout the year.

Regularly reviewing your filing schedule ensures you’re never caught off guard and helps you plan your cash flow accordingly.

Payroll Taxes

If you have employees, you’re responsible for deducting and remitting several payroll taxes at both the federal and provincial levels:

- Canada Pension Plan (CPP) Contributions: Deducted from employee pay and matched by the employer.

- Employment Insurance (EI) Premiums: Deducted from employee wages and matched by the employer, with rates varying slightly by province.

- Income Tax Withholding: Deducted based on the employee’s income and province of residence.

These contributions must be remitted to the CRA on a regular schedule—monthly or quarterly, depending on your payroll size. Missing deadlines can result in penalties, so setting up reliable payroll software or consulting an accountant is highly recommended.

Incentives and Deductions

The Canadian government offers several programs and deductions designed to support small businesses:

- Small Business Deduction (SBD): Lowers the corporate tax rate for Canadian-controlled private corporations.

- Provincial Tax Credits: Programs like Ontario’s Innovation Tax Credit or British Columbia’s Small Business Venture Capital Tax Credit can help offset expenses related to research, development, or investment.

- Other Deductions: You can also deduct legitimate business expenses such as home office costs, vehicle expenses, and professional fees.

Exploring these programs early can reduce your overall tax burden and free up cash to reinvest in growth. The CRA’s Small Business section provides comprehensive guidance to help you identify eligible programs and ensure compliance.

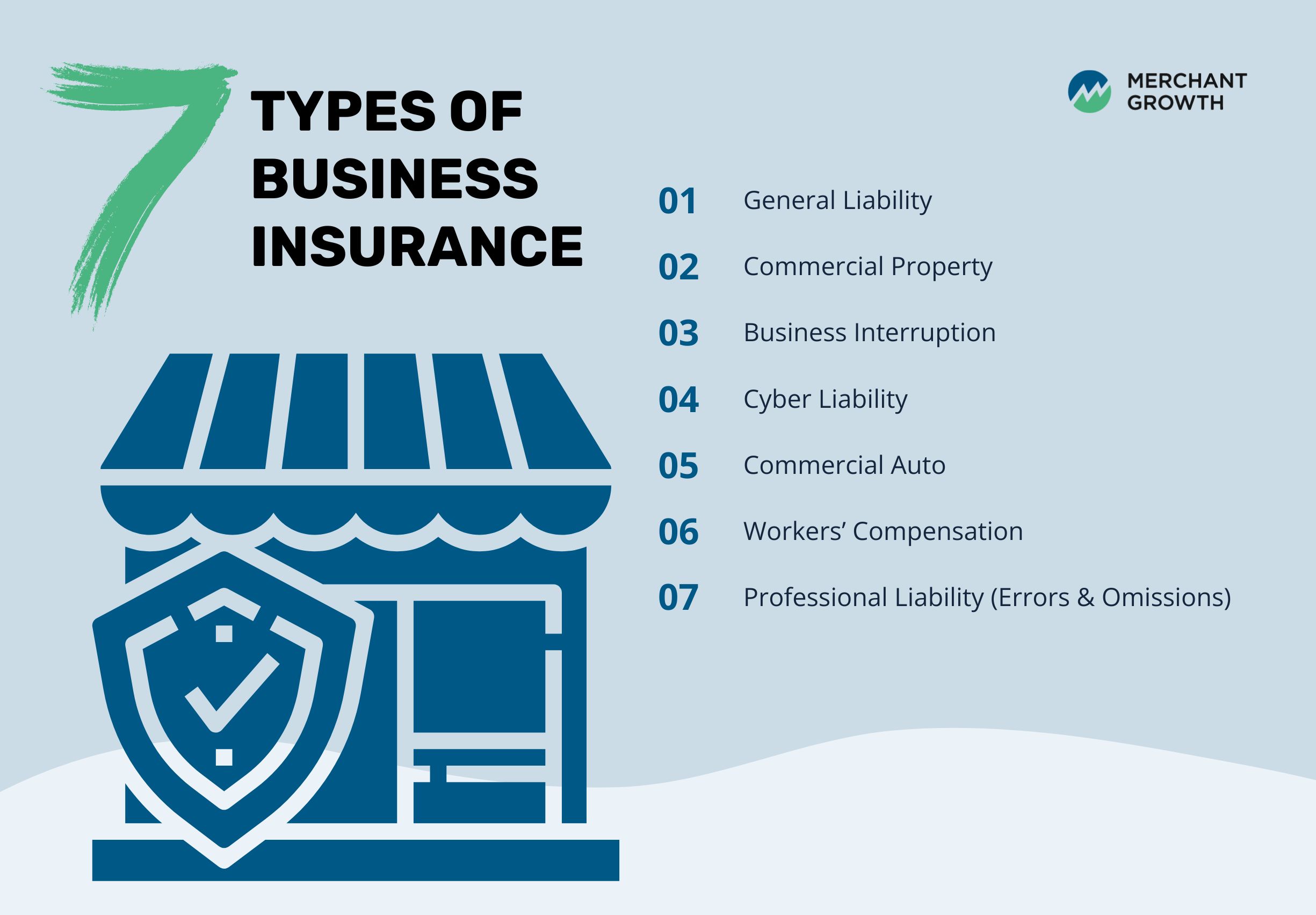

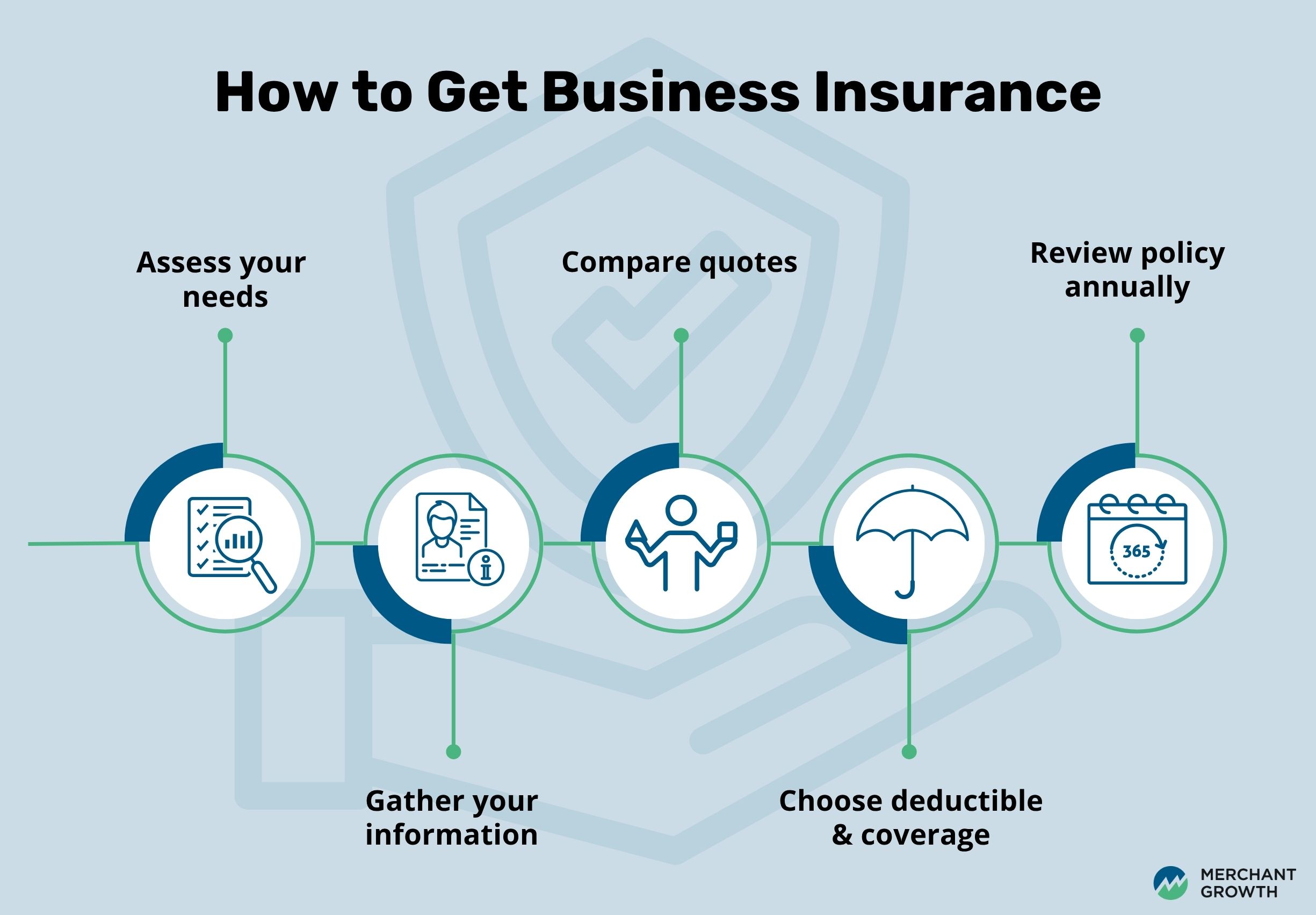

Confirm if You Will Need Insurance

Almost every business faces some level of risk—whether it’s property damage, an accident involving a client, or an error in the services you provide. That’s why understanding your insurance needs early is essential. While not all types of coverage are mandatory, having the right insurance can protect your business, your finances, and your peace of mind. Let’s break down the main types of insurance you may need.

- General Liability: Covers third-party injuries or property damage.

- Property Insurance: Protects your assets and equipment.

- Professional Liability: Important for consultants, designers, and advisors.

- Workers’ Compensation: Mandatory if hiring employees.

Not every business requires all of these coverages, and some industries have specialized insurance requirements. The Insurance Bureau of Canada provides guidance and tools to help identify which types of insurance apply to your business. Consulting with a licensed insurance broker can also help ensure you have adequate protection without paying for unnecessary coverage.

Identify Industry Regulations

Running a business in Canada comes with responsibilities beyond making sales or providing services. Depending on your industry and location, you’ll need to comply with a range of laws and regulations designed to protect employees, customers, and the public. Understanding these rules early can save you time, money, and legal headaches. Below are the key areas most small businesses need to consider:

Health and Safety Laws

Health and safety regulations are essential for protecting employees and customers. Any business with a physical workspace—offices, stores, restaurants, or manufacturing facilities—must follow provincial and federal workplace safety standards. This includes providing proper training, safety equipment, emergency procedures, and reporting any workplace incidents. For example, a construction company must follow strict occupational health guidelines, while a restaurant must maintain hygiene and food safety protocols.

Zoning Laws

Before choosing your business location, it’s important to verify that your intended operations are allowed in that area. Zoning laws dictate where certain types of businesses can operate, such as retail stores, manufacturing facilities, or home-based offices. Checking with your municipal zoning office can prevent costly relocations or fines later on. For instance, a small café may not be allowed to operate in a strictly residential zone without a special permit.

Employment Standards

Employment laws govern minimum wage, working hours, overtime, and other labor requirements. These standards ensure fair treatment of employees and vary by province. If you hire staff, you must comply with these rules and provide things like vacation pay, breaks, and termination notice. Here’s a snapshot of the current minimum wages across Canada:

| Province/Territory | Minimum Wage (2025) |

|---|---|

| Alberta | $15.00 |

| British Columbia | $17.85 (Increase June 1 annually) |

| Manitoba | $15.80 (Increase to $16.00 October 1, 2025) |

| New Brunswick | $15.65 |

| Newfoundland & Labrador | $16.00 |

| Nova Scotia | $15.70 (Increase to $16.50 October 1, 2025) |

| Ontario | $17.20 (Increase to $17.60 October 1, 2025) |

| Prince Edward Island | $16.00 (Increase to $16.50 October 1, 2025) |

| Quebec | $16.10 |

| Saskatchewan | $15.00 (Increase to $15.35 October 1, 2025) |

| Northwest Territories | $16.95 |

| Nunavut | $19.75 |

| Yukon | $17.94 |

Minimum wage as of September 1, 2025, Source: Wagepoint

Intellectual Property (IP)

Protecting your business ideas, brand, and creative work is critical. IP laws cover trademarks, patents, copyrights, and trade secrets. For example, if you’ve developed a unique product, applying for a patent can prevent competitors from copying it. A distinctive brand name or logo can be protected as a trademark, and original content, like websites or marketing materials, is automatically protected by copyright. Understanding IP rules helps maintain your competitive advantage.

The Canadian Government offers detailed guidance on industry regulations, ensuring your business stays compliant with federal, provincial, and municipal laws. Taking the time to understand these requirements now makes future growth smoother and avoids costly legal issues.

Secure Funding for Your Small Business

Turning your business idea into reality usually requires some capital. Whether it’s covering startup costs, purchasing inventory, or marketing your new venture, having access to the right funding can make all the difference. Fortunately, Canada has a variety of financing options for entrepreneurs, ranging from traditional loans to government-backed programs and alternative lenders. Understanding your options early helps you choose the best path for your business and ensures you can grow sustainably.

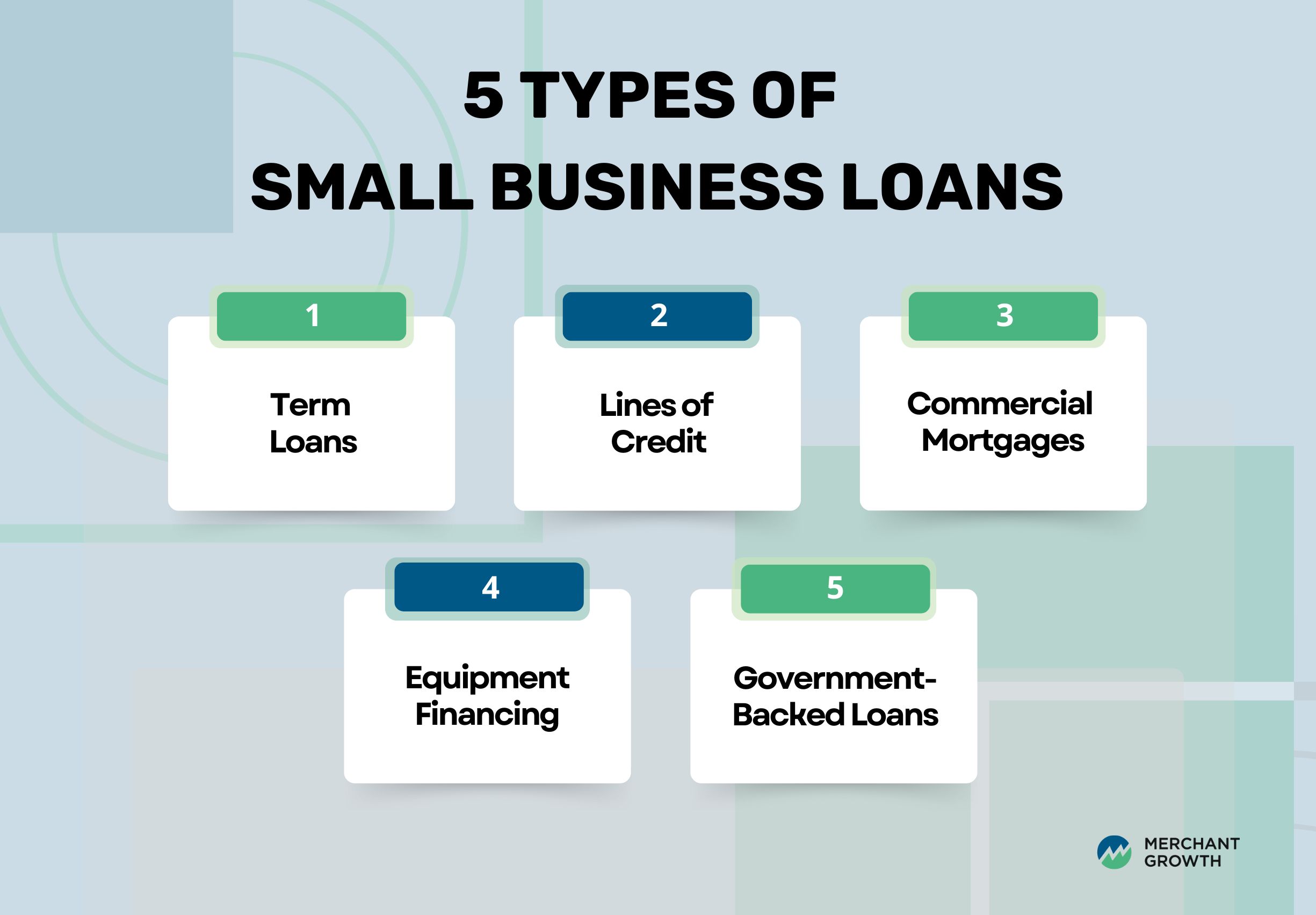

- Small Business Loans: Traditional banks and credit unions offer loans designed specifically for startups. These loans often come with structured repayment plans and competitive interest rates, making them a reliable option for businesses that need larger upfront capital.

- Grants: Government programs, like the Canada Small Business Financing Program or provincial-level grants, provide non-repayable funding for eligible businesses. Grants are typically aimed at specific sectors, growth initiatives, or innovation projects.

- Alternative Lenders: Online lenders, peer-to-peer platforms, and microloan programs offer more flexible financing options, often with faster approval times. These can be a good solution if you don’t meet traditional lending criteria.

Having a clear business plan is critical when seeking funding—it demonstrates to lenders or grant providers that you’ve carefully considered your expenses, revenue projections, and growth strategy. Later, we’ll dive deeper into each funding type, including tips for applying, eligibility criteria, and strategies to improve your chances of approval. With the right funding in place, you’ll be better positioned to bring your business vision to life and tackle the challenges that come with growth.

How Much Does it Cost to Open a Small Business?

The costs of starting a business in Canada can vary significantly depending on your industry, location, and the scale of your operations. While some businesses can start with just a few thousand dollars, others may require substantial upfront investment. Understanding the different types of expenses and planning for them carefully is key to keeping your business financially healthy.

Business Registration

Registering your business is one of the first legal steps to operating in Canada. It officially recognizes your business, allows you to open a business bank account, and is required if you want to access funding, grants, or government programs.

The cost of registration varies depending on your business structure and whether you register provincially or federally. For example, sole proprietorships typically have lower registration fees, while corporations involve higher costs due to more complex filings and compliance requirements. Provincial registration fees usually range from $60 to $500, depending on the province and the type of business. Keep in mind that these are base fees—additional costs may apply for extra filings, name searches, or specialized business licenses.

Equipment and Inventory

Equipment and inventory costs depend heavily on the type of business you’re launching. A home-based online store may only need a computer, printer, and initial stock, while a café or retail shop will require commercial-grade equipment, furniture, and larger inventory.

Examples of startup equipment and inventory:

- Retail: Shelving, point-of-sale systems, initial stock

- Food services: Kitchen appliances, utensils, refrigeration units

- Office-based services: Computers, software, desks, office supplies

Startup costs can range widely—from a few hundred dollars for home-based operations to tens of thousands for brick-and-mortar businesses. Planning carefully helps ensure you don’t overspend while still investing in what’s essential.

Marketing and Website

Marketing is an essential cost to attract and retain customers. Initial expenses can include branding, logo design, website setup, social media advertising, and printed materials. While small businesses can sometimes start with lower-cost marketing strategies, investing in a professional online presence and brand identity can make a significant difference.

Examples of marketing activities and materials:

- Website domain and hosting

- Social media campaigns and content creation

- Flyers, business cards, and signage

- Email marketing platforms and customer relationship management (CRM) tools

Expect marketing costs to vary depending on your approach—some businesses may spend a few hundred dollars initially, while others may invest thousands to create a polished brand presence.

Operational Expenses

Ongoing operational expenses are essential to keep your business running smoothly. These include:

- Rent or lease for physical locations

- Salaries and wages for employees

- Utilities such as electricity, water, internet, and phone

- Software subscriptions, insurance, and supplies

- Maintenance or shipping costs

Even small businesses need to budget for at least several months of operational expenses before they start turning a profit. Factoring in unexpected costs or growth plans ensures your business remains resilient in the early stages.

Careful budgeting across all these areas—registration, equipment, marketing, and operations—sets a strong foundation for your business and helps you invest strategically in growth.

Small Business Grants in Canada

Grants are one of the most attractive ways to fund a startup because they don’t need to be repaid. However, they often come with specific eligibility requirements, including your business sector, location, and ownership structure. Many grants also require a detailed business plan, financial projections, and clearly defined objectives to demonstrate how the funds will be used effectively.

Canada offers a variety of grants at both the federal and provincial levels. Federal programs, such as those listed on Innovation Canada, provide support for research, technology adoption, and growth initiatives. Provinces often have their own programs, incubators, and industry associations that provide targeted funding for local businesses. Taking the time to research and apply for the grants relevant to your business can give you a financial boost without adding debt to your balance sheet.

Small Business Loans in Canada

While grants are ideal, loans are often the backbone of small business funding, providing the capital you need to get started or expand. Banks and traditional lenders require documentation such as a solid business plan, financial statements, and a good credit history. To improve your chances of approval, show realistic financial projections, demonstrate your ability to repay, and highlight any early signs of profitability.

Canada has several options for small business loans, including government-backed loans like the BDC Start-Up Loan and financial institutions offering small business products. These loans are generally more structured than alternative funding and often offer lower interest rates, making them a reliable option for businesses that meet the lender’s requirements.

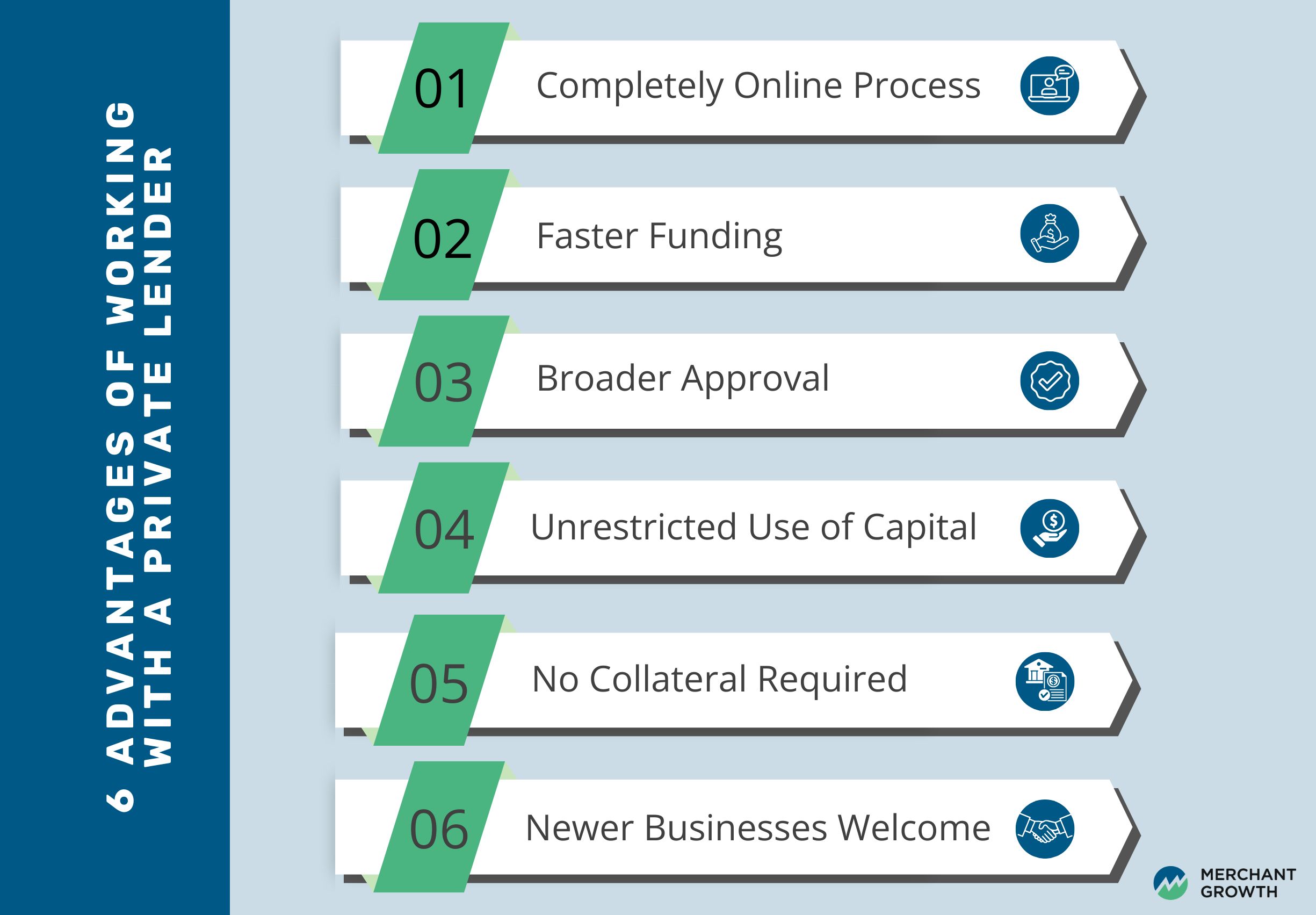

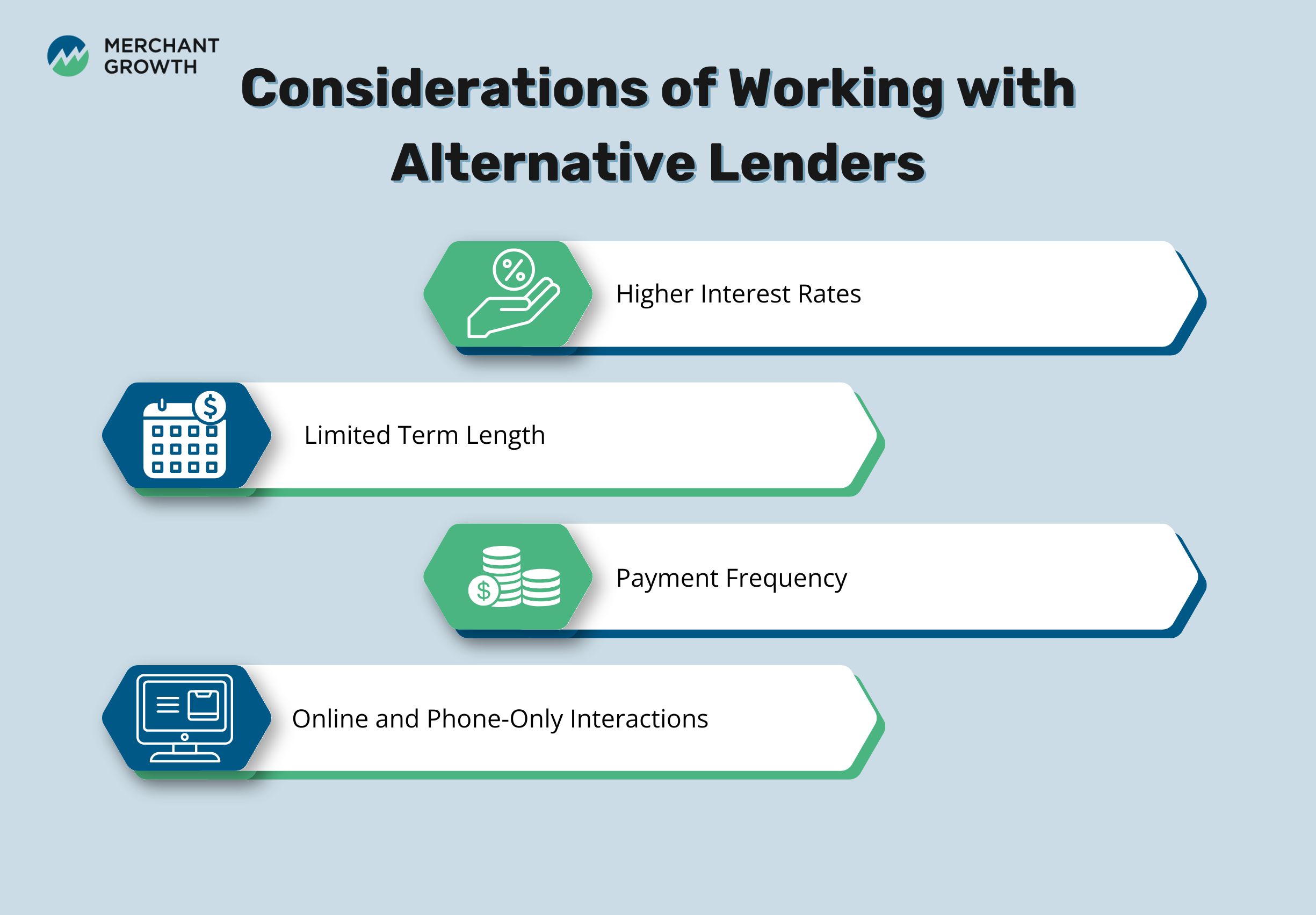

Alternative Lenders to Support Your Small Business

For entrepreneurs who need faster, more flexible access to capital, alternative lenders have become a popular choice. These include online lenders, peer-to-peer lending platforms, and microloans offered through local development agencies. These funding sources often approve applications more quickly and offer flexible repayment terms, but they may come with higher interest rates than traditional loans.

Alternative financing is particularly useful for businesses with a proven track record but less access to traditional credit. If your business has been operating for at least six months and generates revenue above $10,000, you may be eligible for Merchant Growth term financing, which offers a streamlined application process tailored for small businesses ready to scale. Applying for funding through Merchant Growth can help you invest in growth initiatives, hire staff, or expand your operations with confidence.

Starting a small business in Canada requires more than just a great idea—it takes careful planning, compliance, and smart financial decisions. By exploring grants, traditional loans, and alternative financing options, you can find the funding that fits your business needs. Combining these resources with a clear plan, organized budgeting, and the right support can set you on the path to building a thriving business.

Ready to get started? Check out our free How to Start a Business Checklist ➡️ Download Here today.

How to Set Business Goals: A Step-by-Step Guide for Canadian Small Businesses

Running a small business in Canada comes with big opportunities—but without clear goals, it’s easy for your team to lose direction and momentum. Setting clear business goals is essential for keeping everyone aligned, motivated, and working toward the same objectives. Yet research shows that only 20% of businesses complete 80% of their strategic goals, and many employees and managers don’t even know what the primary goals of the business are. Without alignment, it’s easy to lose focus, slow progress, and miss opportunities for growth.

This guide will help you fix that. Step by step, we’ll show you how to define and categorize your business goals, apply the SMART framework to make them actionable, and track progress so your team stays on the same page. You’ll also learn practical tools, templates, and strategies to celebrate wins along the way—helping your business stay focused, your team motivated, and your growth sustainable.

Key Takeaways

- Goals give your business focus and measurable benchmarks

- Use the SMART framework: Specific, Measurable, Achievable, Relevant, Time-bound

- Align goals with your business mission and vision

- Track, adapt, and celebrate progress

- Tools like worksheets, software, and templates make goal-setting easier

What Are Business Goals?

Business goals are the specific outcomes your company wants to achieve within a set timeframe. They act as a roadmap for growth, helping you allocate resources efficiently, measure success, and stay motivated. Without clear goals, your business risks stagnation, missed opportunities, and inconsistent results.

Think of goals as signposts—they guide decisions, prioritize actions, and give your team something concrete to work toward. When everyone knows what the business is aiming for, it becomes easier to align efforts, set priorities, and celebrate progress. Goals also give employees a sense of purpose and clarity, helping them see how their day-to-day work contributes to the bigger picture. In fact, employees with clear goals are 8.1 times more likely to take initiative and independently seek ways to improve their work.

Now that you know why goals are so important, it helps to look at the different types of business goals. Each type focuses on a specific area—whether it’s day-to-day operations, long-term growth, or strategic priorities—and understanding them makes it easier to set goals that actually move your business forward.

What Are the Different Types of Business Goals?

Not all goals are meant to be measured in the same way or achieved on the same timeline. By breaking goals into different types, you can make sure your business is tackling both the day-to-day tasks that keep operations running smoothly and the bigger, long-term objectives that drive growth. Understanding these categories gives you a clearer picture of where to focus your energy and how to involve your team in meaningful ways.

Strategic Goals

Strategic goals are your long-term targets that define the overall direction of your business. They’re big-picture objectives that shape decisions, guide resource allocation, and help set priorities across teams. Having well-defined strategic goals ensures that every action taken in your business moves you closer to your vision.

Examples:

- Expand into new Canadian provinces

- Launch a new product line

- Increase market share in your niche

Operational Goals

Operational goals focus on the day-to-day processes that keep your business running efficiently. They are practical targets designed to improve workflows, reduce bottlenecks, and make your operations more predictable and consistent. Meeting these goals helps your team work smarter, not harder, and sets the foundation for achieving bigger ambitions.

Examples:

- Reduce order processing time by 20%

- Automate monthly reporting tasks

- Streamline customer service response times

Stretch Goals

Stretch goals are ambitious objectives that push your team beyond their comfort zone. These targets may feel challenging or even audacious, but they inspire innovation, motivate high performance, and encourage creative problem-solving. While not every stretch goal will be fully achieved, the pursuit itself often drives significant growth.

Examples:

- Triple revenue in one year

- Acquire 10,000 new customers in 12 months

Financial Goals

Financial goals center on the numbers that keep your business sustainable and profitable. They provide a measurable way to track growth, manage costs, and make informed investment decisions. Clear financial goals help your team understand how their work directly contributes to the company’s bottom line.

Examples:

- Achieve $250,000 in annual sales

- Reduce operational costs by 15%

- Increase profit margins by 10%

Marketing Goals

Marketing goals focus on connecting with your customers and building your brand presence. They help drive awareness, engagement, and loyalty, which in turn fuels revenue growth. With measurable marketing targets, your team can track campaigns, refine messaging, and identify the strategies that deliver results.

Examples:

- Grow Instagram followers by 5,000 in six months

- Increase repeat purchase rate by 20%

- Launch a referral program for new clients

Growth Goals

Growth goals are about expanding your business—whether through new products, markets, or service offerings. These goals often overlap with strategic objectives, but they specifically highlight areas of opportunity for scaling operations, increasing revenue, or reaching more customers. Setting clear growth goals keeps your team focused on sustainable expansion rather than short-term gains.

Examples:

- Open a new storefront in Toronto

- Launch an e-commerce platform for national sales

- Expand service offerings to new industries

Now that you know the different types of business goals, you can see how each one shapes the way your business operates and grows. From day-to-day tasks to big-picture ambitions, clear goal categories help your team stay focused and motivated. The next step is ensuring these goals are realistic and achievable—because well-defined, attainable goals are what truly drive progress and keep your business moving forward.

Why Setting Realistic Goals Matters

Setting realistic goals isn’t just about targets—it’s about giving your team clarity and confidence. When goals are achievable, employees know what’s expected, can focus their efforts, and feel motivated to contribute. Unrealistic or poorly defined goals, on the other hand, can cause stress, reduce productivity, and lead to burnout.

Tips for realistic goal-setting:

- Break larger objectives into smaller, manageable steps

- Regularly check progress and adjust as needed

- Celebrate every win, no matter how small

Achievable goals help maintain morale, strengthen teamwork, and create momentum for steady growth. Teams that understand what success looks like are more engaged and proactive, taking ownership of their work and driving results. That’s why structured frameworks like SMART goals are so valuable—they provide a clear, practical approach to setting objectives, ensuring your business stays on track.

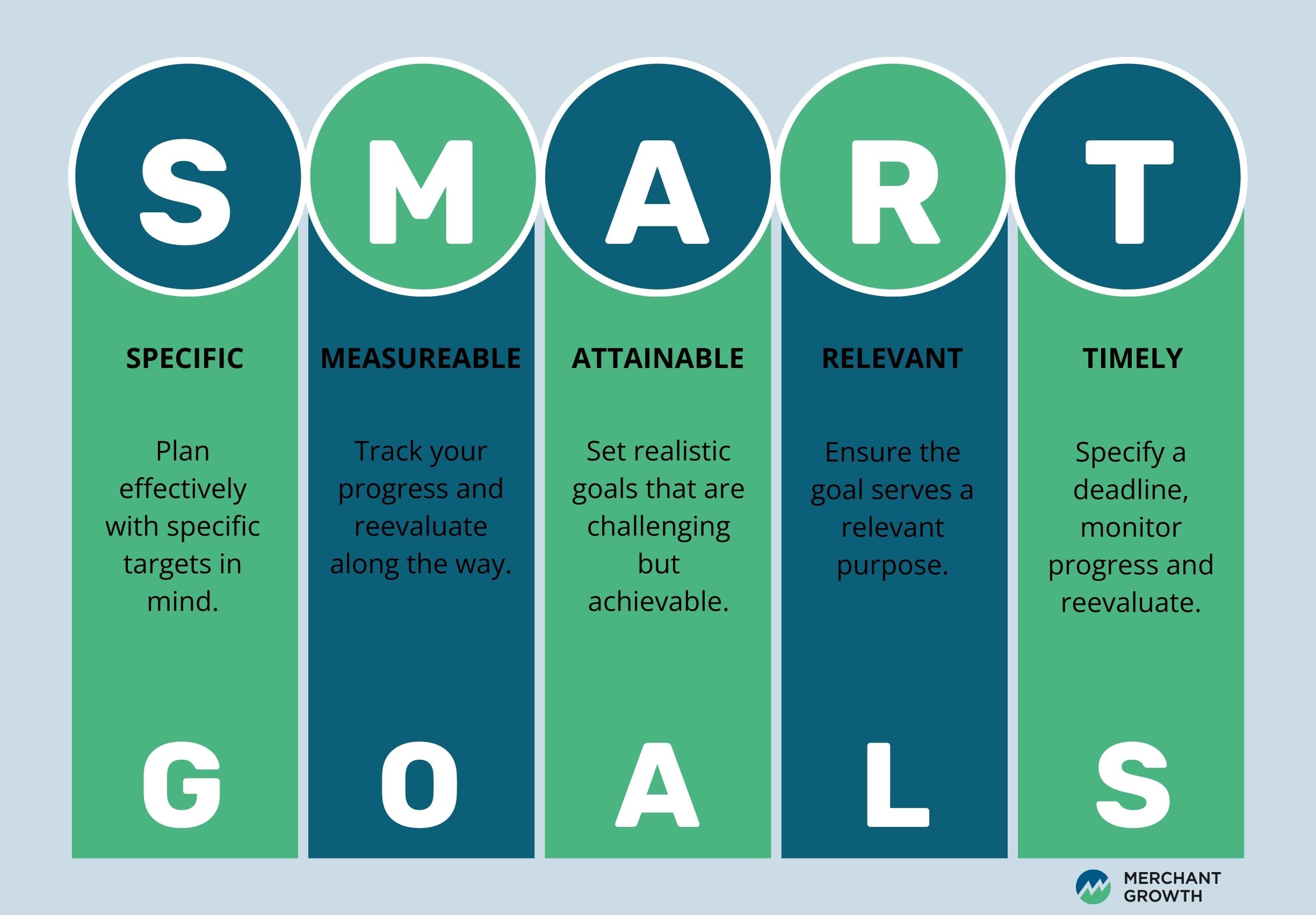

The SMART Framework for Business Goals

Setting goals is one thing—achieving them is another. The SMART framework provides a simple, practical structure to turn ambitions into actionable, measurable outcomes. By making your goals Specific, Measurable, Achievable, Relevant, and Time-bound, you ensure every objective is clear, realistic, and aligned with your business priorities. This approach helps Canadian small business owners focus their efforts, track progress, and keep their teams motivated along the way. However, even with SMART goals, urgency can be lacking—research from Leadership IQ found that only 30% of 12,801 participants felt a strong drive to achieve their objectives, showing that well-structured goals still need thoughtful application to be effective

Specific

A specific goal clearly defines what you want to accomplish, leaving no room for confusion. Vague goals like “grow my business” can be difficult to act on because the target isn’t clear. Specific goals provide direction and clarity, helping your team understand exactly what’s expected.

Example: Instead of saying, “Increase online sales,” set a goal like, “Increase online sales of product X by 15% in Q3.”

Measurable

Measurable goals allow you to track progress using data and key performance indicators (KPIs). When success is quantifiable, it’s easier to see how your actions are contributing to the goal, celebrate milestones along the way, and adjust strategies if needed.

Example: Monitor weekly revenue, new leads, or customer engagement rates to see whether your marketing efforts are driving results.

Achievable

Achievable goals are realistic and consider your current resources, team capacity, and timeframe. Goals that are too ambitious can demotivate employees, while attainable goals inspire confidence and encourage action. Assess your capabilities before setting targets to ensure they’re challenging but realistic.

Example: Don’t aim to double revenue in a month if your infrastructure can’t support it. Instead, plan incremental growth that your team can realistically achieve.

Relevant

Relevant goals align with your overall business vision and strategic priorities. This ensures your team is focusing on what matters most, rather than being pulled in multiple directions. Every goal should contribute to the bigger picture of your company’s growth.

Example: Focus on increasing sales in your core market rather than launching side projects that don’t support your long-term objectives.

Time-Bound

Time-bound goals include a clear deadline, creating urgency and helping maintain focus. Without a timeframe, it’s easy for projects to lose momentum or priorities to shift. Setting deadlines also provides a way to evaluate progress and celebrate achievements on schedule.

Example: Complete the marketing campaign by October 31st to ensure you hit seasonal sales targets.

Pro Tip: Use the SMART framework to evaluate every goal and avoid vague objectives that aren’t actionable. This small step can make a big difference in keeping your team aligned and accountable.

When your goals are structured using SMART principles, it becomes easier to prioritize and plan the work that will get you there. Clear, actionable goals create a roadmap for both immediate actions and bigger-picture objectives. In the next section, we’ll break down short-term and long-term goals, showing how to balance daily progress with your strategic vision for growth.

Short-Term vs Long-Term Goals

Goals come in different timeframes, and understanding the difference between short-term and long-term objectives helps you prioritize daily actions while keeping an eye on your bigger vision. Both types of goals are essential: short-term goals create momentum and quick wins, while long-term goals guide the overall direction of your business. Balancing the two ensures your team stays productive and aligned, without losing sight of the bigger picture.

Short-Term Goals

Short-term goals are immediate, actionable targets you can achieve in weeks or months. They help keep your team motivated by providing tangible milestones and a sense of accomplishment along the way. Short-term goals are ideal for tracking progress on specific projects, testing new strategies, or addressing areas of improvement.

Example: Increase website traffic by 20% in Q2 by publishing two blog posts per week and running a targeted social media campaign.

Long-Term Goals

Long-term goals are strategic objectives aligned with your vision for growth, often spanning one to five years or more. They provide direction and focus for your business, helping ensure that daily operations and short-term projects contribute to bigger-picture success. Long-term goals often require careful planning, resources, and patience, but they are key to sustained growth and competitive advantage.

Example: Become the top e-commerce retailer in your niche within three years by expanding product offerings, enhancing customer experience, and growing your digital marketing presence.

By linking short-term goals to your long-term vision, you create a roadmap that guides daily decisions and ensures every action contributes to the future of your business. Next, we’ll walk through practical steps to set business goals, so you can turn these ideas into a clear, actionable plan that drives results.

Steps to Set Business Goals

Now that you understand the difference between short-term and long-term goals, it’s time to translate that knowledge into actionable steps. Setting business goals isn’t just about writing down what you want to achieve—it’s about taking a structured approach that ensures your goals are realistic, aligned with your vision, and achievable. The following steps provide a roadmap to help you define, organize, and track your business objectives, so your team can stay focused and make measurable progress.

Step 1: Examine Your Business with a SWOT Analysis

Before setting goals, it’s important to understand your starting point. A SWOT analysis—assessing your Strengths, Weaknesses, Opportunities, and Threats—provides a clear picture of where your business excels, where improvements are needed, and where potential opportunities lie. By taking a close look at internal capabilities and external market conditions, you can identify areas where your efforts will have the greatest impact and anticipate challenges that could slow progress.

- Strengths: What you do better than competitors

- Weaknesses: Areas needing improvement

- Opportunities: Market gaps or emerging trends

- Threats: Challenges from competitors or industry changes

Step 2: Identify a Market Gap

A critical part of goal-setting is understanding the market you operate in. Spotting opportunities that competitors have overlooked can give your business a real edge. Consider whether customers are asking for a product or service that isn’t currently available, or if there are inefficiencies in existing offerings that you could solve. By identifying and targeting these gaps, you can develop goals that not only drive growth but also position your business as a solution provider, increasing customer loyalty and long-term success.

Examples to explore:

- Are customers requesting services that competitors don’t provide?

- Is there a process or experience you could make easier or more efficient?

Step 3: Brainstorm and Prioritize Goals

Once you’ve examined your business and the market, it’s time to brainstorm potential goals. Include everything that could make a meaningful impact, but don’t worry about feasibility yet. After compiling a list, prioritize your goals based on three key factors: the potential impact on revenue or growth, the feasibility with current resources, and alignment with your strategic vision. This ensures your team focuses on goals that matter most and avoids spreading effort too thin.

Step 4: Assign Tasks, Responsibilities, and Deadlines

Clear ownership is essential for turning goals into action. For each goal, assign tasks to team members, define responsibilities, and set measurable milestones. Deadlines create urgency and accountability, helping ensure that progress is consistent and visible. When everyone knows who is responsible for what and by when, it reduces confusion, encourages collaboration, and keeps your business on track.

Step 5: Track Progress and Adjust

Goal-setting doesn’t end once targets are written down. Regularly reviewing your goals, measuring results, and making adjustments is key to staying on course. Use dashboards, spreadsheets, or project management tools to track performance, identify areas that need attention, and celebrate successes along the way. Being flexible and responsive allows your business to adapt to changes, learn from setbacks, and keep your team motivated.

By following these steps, you’re not just setting goals—you’re creating a clear, actionable roadmap for growth. The next step is making sure every goal you set is structured to be achievable and measurable, which is where the SMART framework comes in.

Tools and Resources for Managing Goals

Setting clear goals is only part of the process—tracking progress and staying organized is equally important. Fortunately, there are a variety of tools and resources that can help you keep your goals on track, whether you prefer spreadsheets, apps, or project management platforms. The right tools make it easier to assign responsibilities, monitor milestones, and adjust plans as needed, saving time and keeping your team aligned.

- Worksheets: Google Sheets or customizable templates allow you to create simple, visual tracking systems for your business goals. They’re flexible, easy to share, and ideal for smaller teams. Check out our free business goals worksheet here. ➡️ Download Here - Merchant Growth - Business Goal Setting Worksheet

- Project Management Software: Platforms like Trello, Asana, and Monday.com help organize tasks, assign responsibilities, and monitor progress. These tools provide a clear overview of who is working on what and when, reducing confusion and improving accountability.

- Goal-Tracking Apps: Apps like GoalsOnTrack and Strides provide reminders, progress tracking, and analytics to ensure goals stay on course. They’re particularly useful for individual or team objectives that need regular monitoring.

- Canadian-Specific Resources: Business owners in Canada can take advantage of government and industry resources, such as BDC Planning Tools, to guide strategic planning and goal-setting. These resources provide templates, guides, and advice tailored to the Canadian business environment.

Using the right combination of tools ensures that your goals don’t just live on paper—they become actionable, trackable, and achievable. With systems in place to organize, measure, and celebrate progress, you’re ready to take the next step.

How Merchant Growth Can Help You Achieve Your Goals

Achieving your business goals often requires more than planning and tracking—it sometimes comes down to having the financial resources to bring your strategies to life. Merchant Growth offers tailored financing solutions for Canadian small businesses, helping you fund expansion, hire key team members, or invest in operational improvements that directly support your strategic objectives. With flexible term financing, you can implement initiatives that align with your goals, whether it’s launching a new product, expanding into new markets, or upgrading technology to improve efficiency. Take the next step in growing your business and apply for financing today.

GST/HST for Business: Simplifying Your Tax Obligations in Canada

Understanding GST and HST is a must for every Canadian small business owner. These taxes don’t just affect how you price your products or services—they also impact your cash flow, your accounting, and ultimately, the growth of your business. Ignore them, and you could face penalties, interest, or even audits.

In 2022 alone, over 3 million Canadian businesses filed GST/HST, with Ontario accounting for 1.5 million of those filings. If you’re running a small business, there’s a very real chance you’ll need to charge, collect, and remit GST or HST. Knowing how these taxes work isn’t just about compliance—it’s about keeping your business running smoothly and avoiding surprises that could hurt your bottom line.

This guide is designed to cut through the confusion. From registering for a GST/HST number, to filing returns, to paying taxes online, you’ll learn everything you need to manage your obligations confidently—and keep your focus on growing your business.

Key Takeaways

- GST/HST Registration: Know when and how to register for a GST/HST number to stay compliant.

- Tax Filing: Learn how to file GST/HST returns on time and avoid penalties.

- HST vs. GST: Understand the difference between GST and HST and when each applies to your business.

- Payment Methods: Familiarize yourself with the various methods of paying HST online and using Netfile for businesses.

- Avoid Common Mistakes: Learn about common GST/HST mistakes businesses make and how to avoid them.

What is GST/HST?

Once you understand why GST and HST matter, the next step is knowing exactly what they are. The Goods and Services Tax (GST) is a federal tax of 5% applied to most goods and services sold in Canada. Some provinces, however, have chosen to combine their provincial sales tax with GST, creating the Harmonized Sales Tax (HST).

- GST applies across Canada at 5% in provinces that don’t participate in HST.

- HST applies in provinces like Ontario (13%), Nova Scotia (14%), and New Brunswick (15%), combining the federal and provincial portions into a single, simplified tax.

The key difference is that HST streamlines tax collection for businesses operating in provinces that harmonize their sales tax with GST. Which tax you charge depends on where your business is located and where your customers are based—so getting this right from the start keeps your pricing, invoicing, and reporting smooth and compliant.

How to Register for a GST/HST Number

Now that you understand what GST and HST are, the next step is knowing if and how your business should register. In Canada, businesses with annual revenues over $30,000 are required to register for a GST/HST number. This registration gives you the legal ability to charge, collect, and remit GST/HST, ensuring your business stays compliant with federal and provincial tax laws.

Even if your revenue is below the $30,000 threshold, registering voluntarily can provide benefits, such as the ability to claim input tax credits (ITCs) for GST/HST paid on business expenses—a smart move for many growing businesses.

Here’s a step-by-step guide to get registered:

Step 1: Determine if Your Business Exceeds the $30,000 Threshold

The $30,000 limit applies to your gross revenue over the last four consecutive calendar quarters or in a single calendar quarter. Include revenue from all related businesses under your ownership. If your business earns above this amount, GST/HST registration is mandatory.

Tip: Even if you’re under the threshold, consider registering voluntarily if you have significant business expenses, as this allows you to recover GST/HST through input tax credits.

Step 2: Gather Required Documents

Before registering, ensure you have the necessary information ready:

- Your business number (BN) issued by the CRA (if you don’t have one, you can request it during registration).

- Legal business name as registered federally or provincially.

- Contact information including mailing address, phone number, and email.

- Business structure details (sole proprietorship, partnership, or corporation), since this affects registration options and tax obligations.

Step 3: Register Online or by Phone

You can register for your GST/HST number online via the CRA’s Business Registration Online (BRO) portal or by calling the CRA directly. Online registration is generally faster and allows you to get your GST/HST number immediately.

During registration, you’ll also provide information on your business activities, fiscal year-end, and intended filing frequency (monthly, quarterly, or annually), which depends on your revenue and business type.

Step 4: Receive and Use Your GST/HST Number

Once registration is complete, you will receive a unique GST/HST number, which identifies your business to the CRA. Use this number on:

- Invoices and receipts for sales or services charged

- GST/HST filings and remittances

- Claiming input tax credits for business expenses

Properly using your GST/HST number ensures smooth compliance and helps avoid potential audits or penalties.

Once you have your GST/HST number, you’re officially set up to charge, collect, and remit taxes—but registration is just the first step. The next crucial part of staying compliant is filing your GST/HST returns on time, which ensures your business avoids penalties and keeps your finances in order. Let’s walk through how to handle filing, what forms you’ll need, and tips for making the process as simple as possible.

Filing GST/HST Returns

Once you’ve registered for a GST/HST number, the next step is filing your returns. How often you need to file depends largely on your annual revenue, and knowing your filing schedule helps you stay compliant, manage cash flow, and avoid penalties. Let’s walk through the typical filing frequencies and what they look like in practice.

Annual Filing

For smaller businesses with annual revenue under $1.5 million, filing is usually done once a year. This is common for local boutiques, freelance consultants, or independent service providers who have a manageable volume of transactions. Your return is typically due within three months of your fiscal year-end, so while you only file once, it’s important to keep accurate records throughout the year. Tracking sales, invoices, and receipts will make your annual filing smoother and ensure you claim all eligible input tax credits (ITCs).

Quarterly Filing

As your business grows and your revenue reaches between $1.5 million and $6 million, you’ll likely move to quarterly filings. This applies to mid-sized operations such as established retail stores, regional service providers, or small distribution companies. Filing every three months helps businesses avoid a large lump-sum payment at the end of the year and allows for more regular cash flow planning. Deadlines typically fall one month after the end of each quarter, so consistent bookkeeping is essential. Staying organized ensures you correctly report the GST/HST you’ve collected and claim ITCs without errors.

Monthly Filing

For larger businesses earning over $6 million annually, monthly filing is the standard. High-volume operations like large e-commerce businesses, franchise chains, or manufacturing companies fall into this category. Filing every month might seem like extra work, but it prevents large tax liabilities from building up and keeps your accounts aligned with CRA requirements. Returns and payments are usually due by the end of the following month, and frequent, organized record-keeping is key to avoiding mistakes. Accounting software or a dedicated accountant can save time and reduce the risk of errors.

Once you’ve determined your filing frequency—annual, quarterly, or monthly—you’ll report the GST/HST you’ve collected and subtract any input tax credits. Filing can be done easily online using CRA’s Netfile for businesses, making the process straightforward and efficient. With your returns ready, the next step is paying HST online, ensuring your remittances reach the CRA securely and on time.

Paying HST Online

Paying your HST online is the next step after filing, and the CRA has made the process simple and secure. Once your return is ready, you can quickly remit the taxes you owe without leaving your office, helping you stay compliant and avoid late fees.

- Online banking:Pay directly through your bank’s website.

- Credit card payments: Available via third-party providers.

- Pre-authorized debit: Set up automatic payments for recurring filings.

Pro Tip: Schedule reminders before payment due dates to avoid penalties and interest. Late payments can result in charges starting from 1% per month.

With your HST collected, reported, and remitted, it’s also important to understand how rates differ across provinces and which businesses are required to charge GST/HST, ensuring you remain compliant wherever you operate in Canada.

How Much is GST/HST Across Canada?

Understanding the GST and HST rates in your province is key to charging the correct amount and keeping your business compliant. While the federal GST is consistent at 5%, provinces that participate in the Harmonized Sales Tax combine this with their provincial portion, resulting in different HST rates across the country. Knowing which rate applies to your business location—and where your customers are—ensures accurate pricing and helps you avoid costly mistakes. Below is a breakdown of the current GST and HST rates across Canada:

| Province/Territory | GST/HST Rate |

|---|---|

| Alberta | 5% GST |

| British Columbia | 5% GST + 7% PST |

| Manitoba | 5% GST + 7% PST |

| Ontario | 13% HST |

| Nova Scotia | 14% HST |

| New Brunswick | 15% HST |

| Newfoundland & Labrador | 15% HST |

| Prince Edward Island | 15% HST |

| Quebec | 5% GST + 9.975% QST |

| Saskatchewan | 5% GST + 6% PST |

| Northwest Territories | 5% GST |

| Nunavut | 5% GST |

| Yukon | 5% GST |

By understanding the GST and HST rates that apply to your business, you can ensure you’re charging the correct amount and claiming any input tax credits you’re eligible for. Staying on top of these rates helps prevent errors and keeps your business compliant. Next, we’ll look at some of the most common GST/HST mistakes small businesses make—and how you can avoid them—to protect your business from penalties and audits.

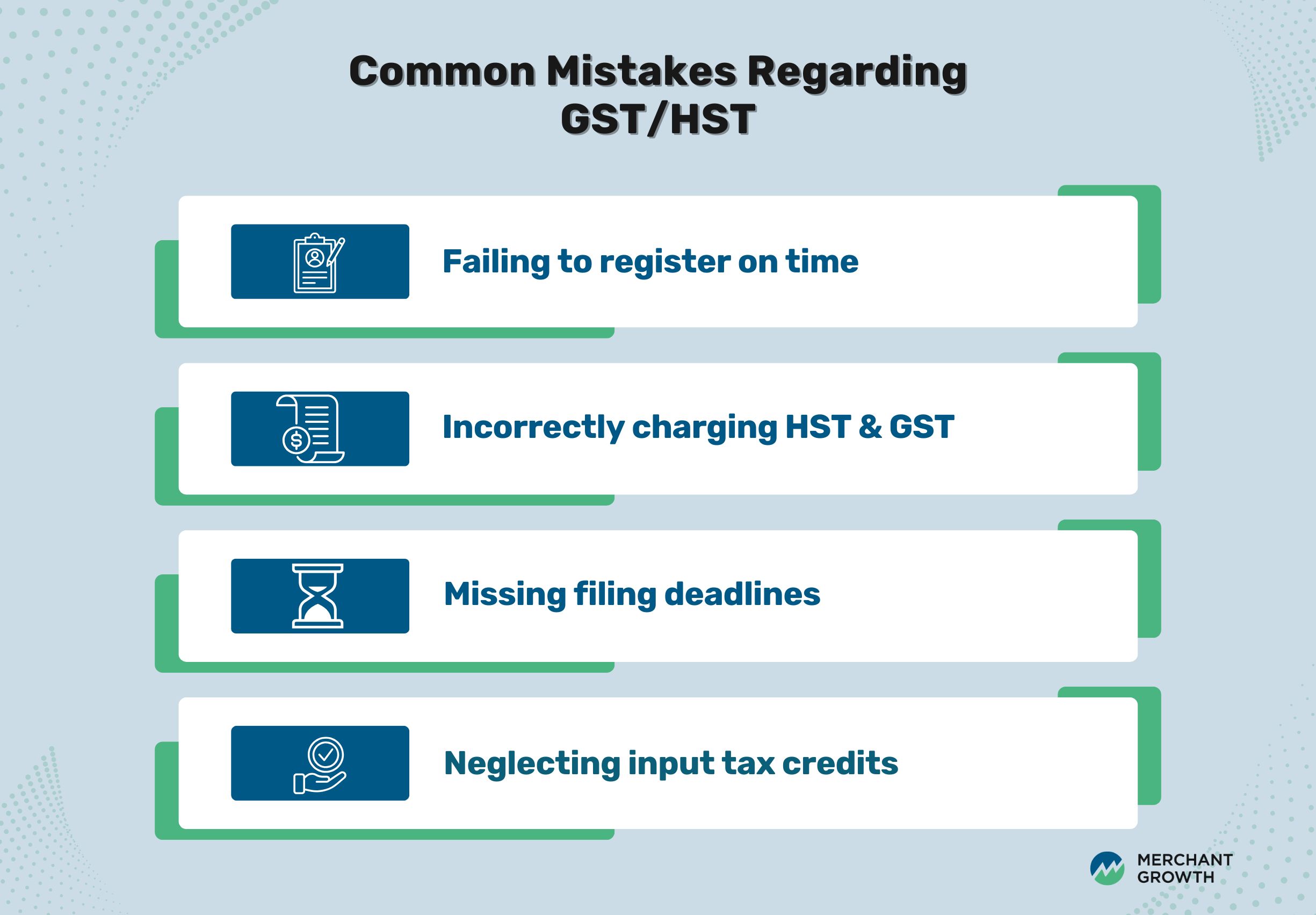

Common GST/HST Mistakes to Avoid

Even small oversights with GST/HST can lead to penalties, interest, or even audits. Many small business owners struggle with compliance simply because these tasks can feel complex or easy to forget. Understanding the most common mistakes and taking steps to prevent them will save time, money, and stress in the long run.

Failing to Register on Time

Not registering for a GST/HST number when your business exceeds the $30,000 threshold is a common mistake. Late registration can lead to owing back taxes and potential penalties. To avoid this, monitor your revenue closely and register promptly once you meet the requirement.

Incorrectly Charging GST or HST

Charging the wrong tax rate—whether GST instead of HST, or an incorrect provincial HST rate—can create compliance issues and upset customers. Always check your customers’ location and confirm the correct rate before invoicing. Keep updated with CRA resources or provincial guidelines to ensure accuracy.

Missing Filing Deadlines

Even if you’re registered correctly, filing late can trigger interest charges and penalties. Filing deadlines vary depending on your revenue (monthly, quarterly, or annually), so make sure you know your schedule and set reminders to avoid missing due dates.

Neglecting Input Tax Credits (ITCs)

Many businesses fail to claim the GST/HST they’ve paid on business expenses. Input tax credits can significantly reduce your net tax payable. Keep clear records of all business-related purchases and ensure you’re claiming eligible ITCs on each filing.

By understanding these common GST/HST mistakes, you can proactively prevent errors that lead to penalties, interest, or audits. Awareness of the pitfalls—from late registration to misapplied tax rates—lays the foundation for strong tax practices. With these lessons in mind, the next step is learning practical tips and strategies to stay fully compliant with GST/HST regulations while keeping your business running smoothly.

Tips to stay compliant:

Staying on top of GST/HST obligations doesn’t have to be overwhelming. With the right habits and tools, you can simplify tax management, avoid costly mistakes, and ensure your business stays in good standing with the CRA. Here are some practical tips to help you remain compliant:

Maintain Detailed Records of All Sales and Purchases

Accurate and thorough record-keeping is the backbone of GST/HST compliance. Keep track of all invoices, receipts, and financial transactions. This ensures you can correctly report taxes collected, claim input tax credits, and provide evidence in the event of an audit. Well-organized records save time and reduce stress when filing returns.

Use Accounting Software That Tracks GST/HST Automatically

Modern accounting tools can automatically calculate and track GST/HST on sales and purchases. Software like QuickBooks or Wave Accounting can help you generate reports, monitor tax obligations, and ensure your filings are accurate. This reduces human error and frees up time to focus on growing your business.

Consider Consulting a Tax Professional, Especially During the First Year

A tax professional can guide you through the complexities of GST/HST registration, filings, and payments. They can help you avoid mistakes, optimize your tax strategy, and provide peace of mind, particularly when you’re just starting. Even occasional consultations can prevent costly errors and ensure compliance.

By maintaining organized records, leveraging accounting software, and seeking professional advice when needed, you can confidently manage your GST/HST obligations. These practices make it easier to stay compliant while focusing on growing your business, reducing the risk of penalties, and keeping your finances in order.

Do I need to charge GST if I earn under $30,000?

No. If your business earns less than $30,000 per year, you’re considered a “small supplier,” which means you’re not required to register for or charge GST/HST. That said, you can choose to register voluntarily. Doing so can be beneficial because it allows you to claim input tax credits (ITCs) to recover the GST/HST paid on business-related expenses—helpful for reducing costs as your business grows. Voluntary registration is often a smart move for new businesses planning to expand or make significant purchases early on.

Managing Your GST/HST with Confidence

Understanding GST/HST is crucial for Canadian entrepreneurs. While it may seem complex at first, following a structured approach—registering properly, filing on time, and paying accurately—ensures smooth operations and avoids penalties.

Beyond understanding your GST/HST obligations, managing cash flow is key. Merchant Growth provides flexible financing to help cover tax payments, manage business operations, and support expansion.

If your business has over $10,000 in revenue and has been operational for at least six months, you may qualify for term financing to help with cash flow or tax obligations.

Focus on running your business while Merchant Growth supports your financial needs. Apply today to secure funding and keep your business on a path to growth with confidence.

How to Write a Business Plan

Starting and growing a small business requires more than just a great idea—it requires a well-thought-out plan. A solid business plan is one of the most important tools you can have when launching or scaling your business. Not only does it serve as a blueprint for your business’s success, but it’s also essential for securing funding and attracting investors. In fact, businesses with a formal plan are 2.5 times more likely to secure funding compared to those without one.

A business plan outlines your company’s mission, vision, and goals, while providing a clear path for reaching them. It serves as a roadmap for your business and a tool for communicating your vision to investors, banks, and other stakeholders. Whether you're looking for funding or simply mapping out your business strategy, a business plan is crucial for turning your ideas into action and growing your business successfully.

In this post, we’ll guide you through the steps of creating a compelling business plan and provide a basic template to help you get started.

Key Takeaways

- Business Plan Structure: A comprehensive business plan includes key sections such as the executive summary, company description, market analysis, and financial projections.

- Customization: Tailor your business plan to reflect the unique aspects of your business, industry, and goals to make it relevant and specific.

- Clarity & Focus: Write your business plan clearly and concisely, avoiding jargon, to ensure it’s easily understood by stakeholders and investors.

- Use of Templates: Templates and samples can be helpful as a starting point, but be sure to personalize the content to fit your business’s needs.

- Strategic Goal Setting: Incorporate short-term and long-term goals into your business plan to align with your business’s growth strategy and provide clear milestones for success.

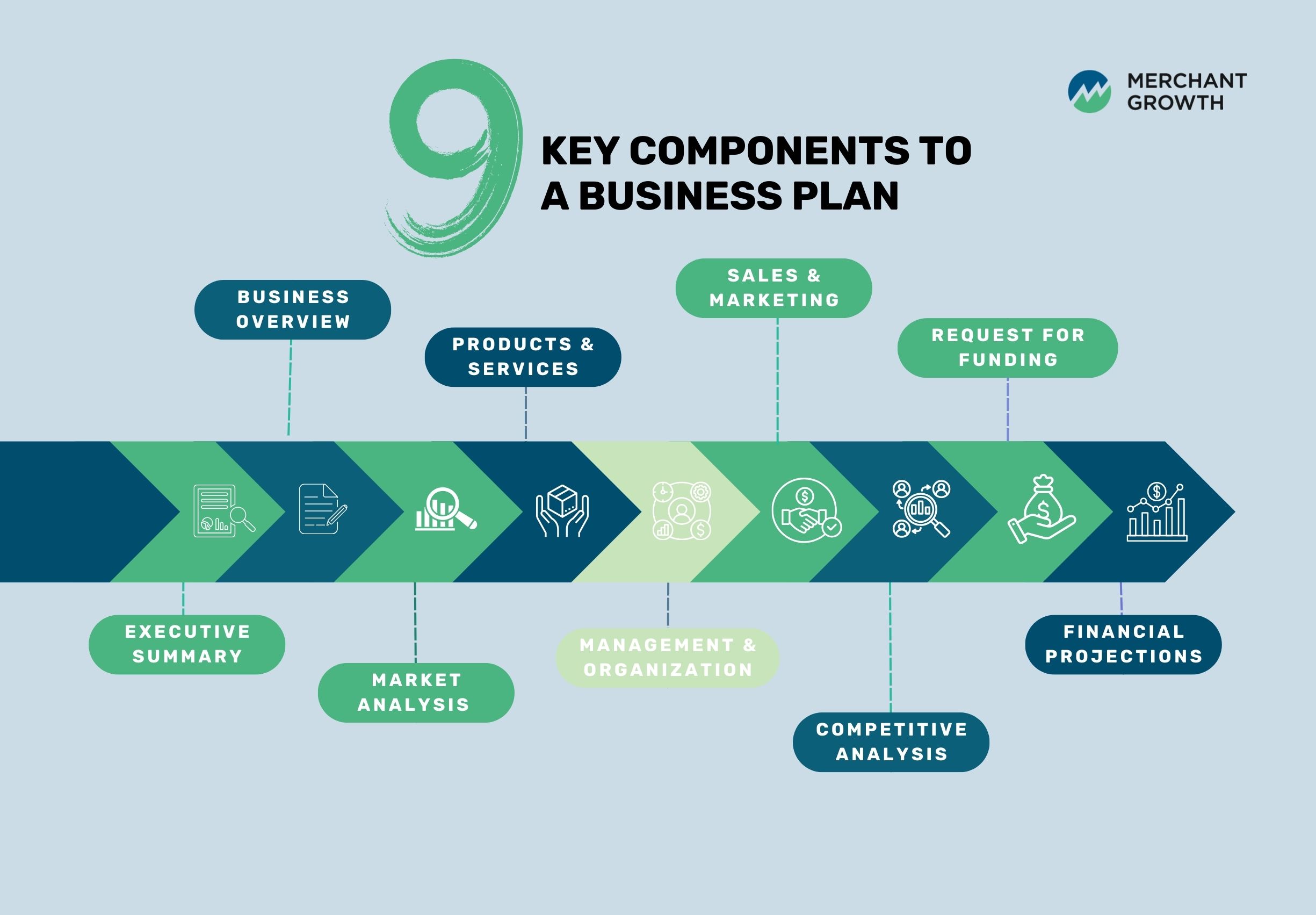

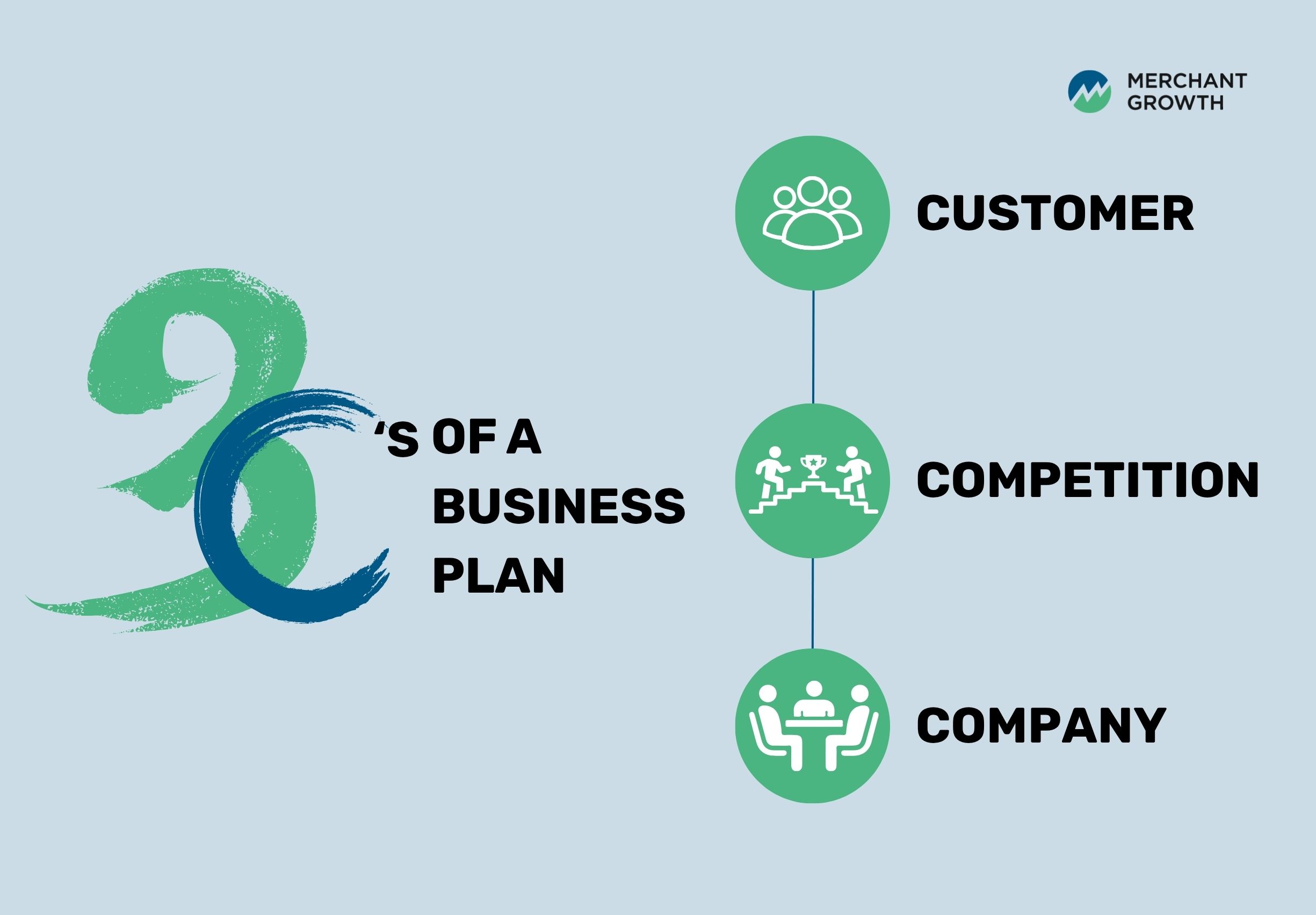

9 Key Components of a Business Plan

Creating a business plan can seem overwhelming, but breaking it down into key components makes the process more manageable. Each section of your business plan plays a crucial role in telling the story of your business, from your goals and strategies to the financial projections that back them up. Here are the nine essential components every business plan should include:

1. Executive Summary

The executive summary is the first and most important section of your business plan. While it’s typically only 1-2 pages long, it provides a concise and clear overview of your entire business plan. This section is your opportunity to grab the reader’s attention, highlighting what makes your business unique and why it has the potential to succeed.

An effective executive summary should cover key aspects of your business, such as your mission, values, and competitive advantages. While this section may come first, it’s often best to complete it last. Doing so ensures that you can confidently present your plan, knowing exactly how each part supports your overall strategy.

Here’s a helpful checklist to guide you as you write your executive summary:

Executive Summary Checklist

- Company Name and Address: Clearly state the name of your company and where it’s located.

- Product or Service Offering: Briefly describe what your business offers and what makes it stand out in the market. For example, "XYZ Bakery will offer premium organic pastries, catering to health-conscious consumers in downtown Toronto."

- Company’s Core Values: What principles guide your business decisions? This could be sustainability, innovation, or customer-centricity.

- Mission Statement: Define your company’s purpose. A great mission statement could be, "To provide high-quality, eco-friendly products that support sustainable living."

- Marketing Strategy Overview: Summarize how you plan to reach your target audience, such as through digital marketing or community partnerships.

- Objectives: Clearly define what you want to achieve in the next 1-3 years (e.g., expanding to a second location, reaching $500,000 in revenue, etc.).

By using this checklist, you’ll ensure that your executive summary covers all the essential elements in a clear and impactful way, helping to set the tone for the rest of your business plan.

2. Business Overview

The business overview section is a foundational part of your business plan. It provides a clear snapshot of your business, outlining key elements like your mission, vision, and what you offer to your target market. This section is designed to give readers an understanding of your business operations, goals, and long-term potential, setting the stage for the rest of your plan.

In this section, you’ll want to describe the market you’re entering, explain what makes your business stand out from competitors, and highlight any important achievements that demonstrate your capacity for success. By focusing on these aspects, you’ll help readers see both your current position and the growth opportunities that lie ahead.

Business Overview Checklist

- Business Description: Outline your company’s mission, vision, and values.

- Products and Services: Clearly explain what your business offers and how it serves your target audience.

- Target Market: Define your target market, including key trends, demographics, and opportunities.