Contract vs Full-Time Work in Canada: Which Career Path Is Right for You?

The way Canadians work is changing quickly. Remote and hybrid work are now mainstream, digital tools make it easier to work independently, and the gig economy continues to grow across nearly every industry. Today, more Canadians are actively weighing the pros and cons of flexible contract work versus the stability of full-time roles, and for many, the answer is no longer obvious.

According to Statistics Canada, nearly 2.7 million Canadians were self-employed as of early 2025, reflecting a steady shift toward contract, freelance, and independent work. Some professionals are drawn to the autonomy, earning potential, and variety that contract work can offer. Others still value the predictability, benefits, and structure of traditional full-time employment. As inflation, cost-of-living pressures, and workplace expectations evolve, choosing the right work model has become an important financial and lifestyle decision.

This choice matters more than ever because it affects far more than your paycheque. Your employment structure influences job security, taxes, benefits, work-life balance, and long-term financial planning. Whether you are early in your career, transitioning out of a corporate role, returning to the workforce, or considering self-employment, understanding how contract, freelance, and full-time work differ can help you make a decision that aligns with your goals.

Choosing how you work is not just about employment status. It is about designing a career that supports the way you want to live, grow, and build financial confidence over time.

Key Takeaways

- Contract work offers flexibility, higher short-term pay, and project variety, but may lack long-term stability.

- Freelance and contract work are not the same; freelancers are typically self-employed with multiple clients.

- Career planning helps you get the best of any path; understanding the trade-offs is key.

- Industries like tech, healthcare, and marketing are especially lucrative for contractors.

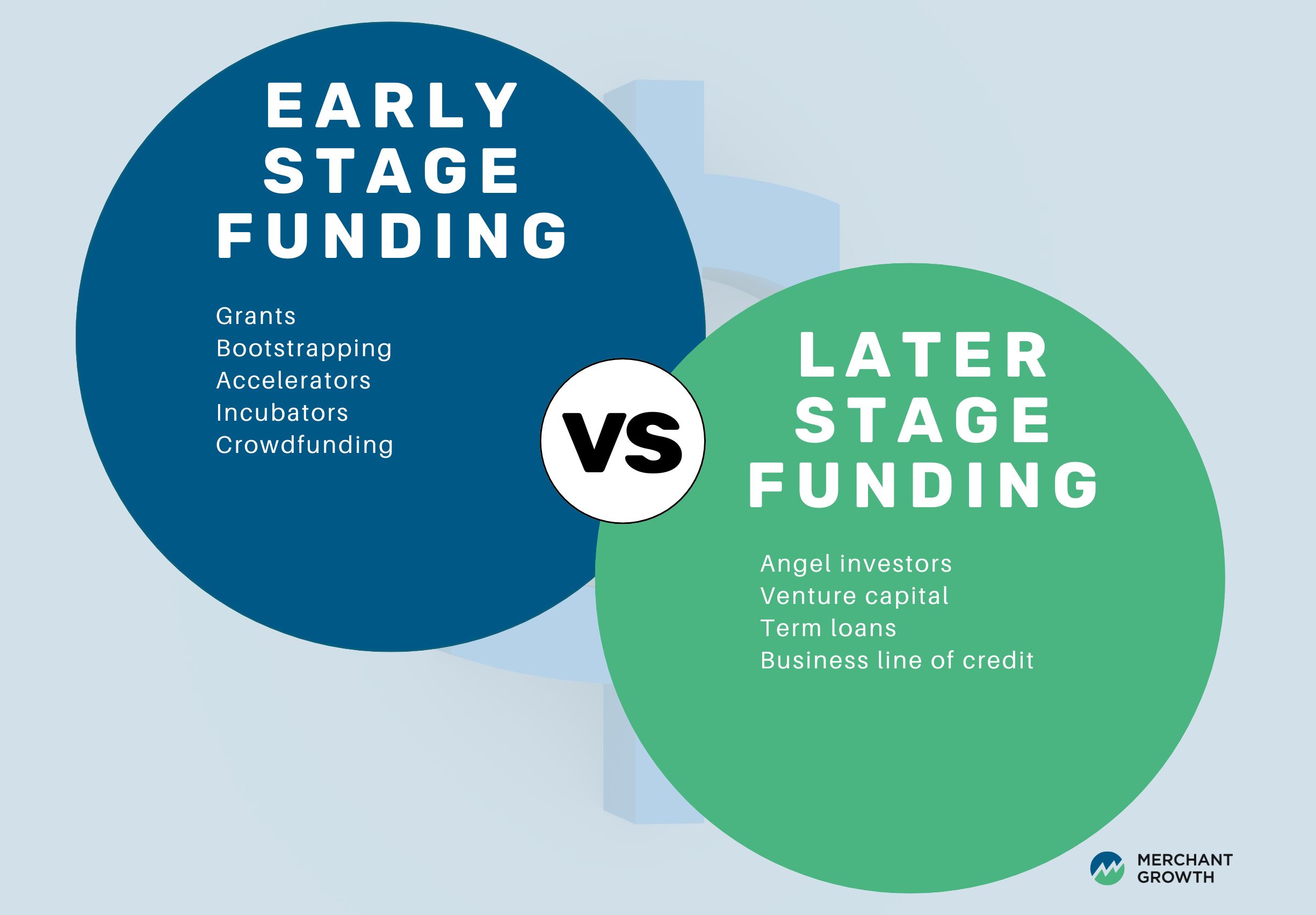

Understanding Today’s Work Models in Canada

Before weighing the pros and cons, it helps to clearly understand how full-time employment, contract work, and freelancing differ. These terms are often used interchangeably, but they represent very different working arrangements with distinct expectations around pay, security, taxes, and independence.

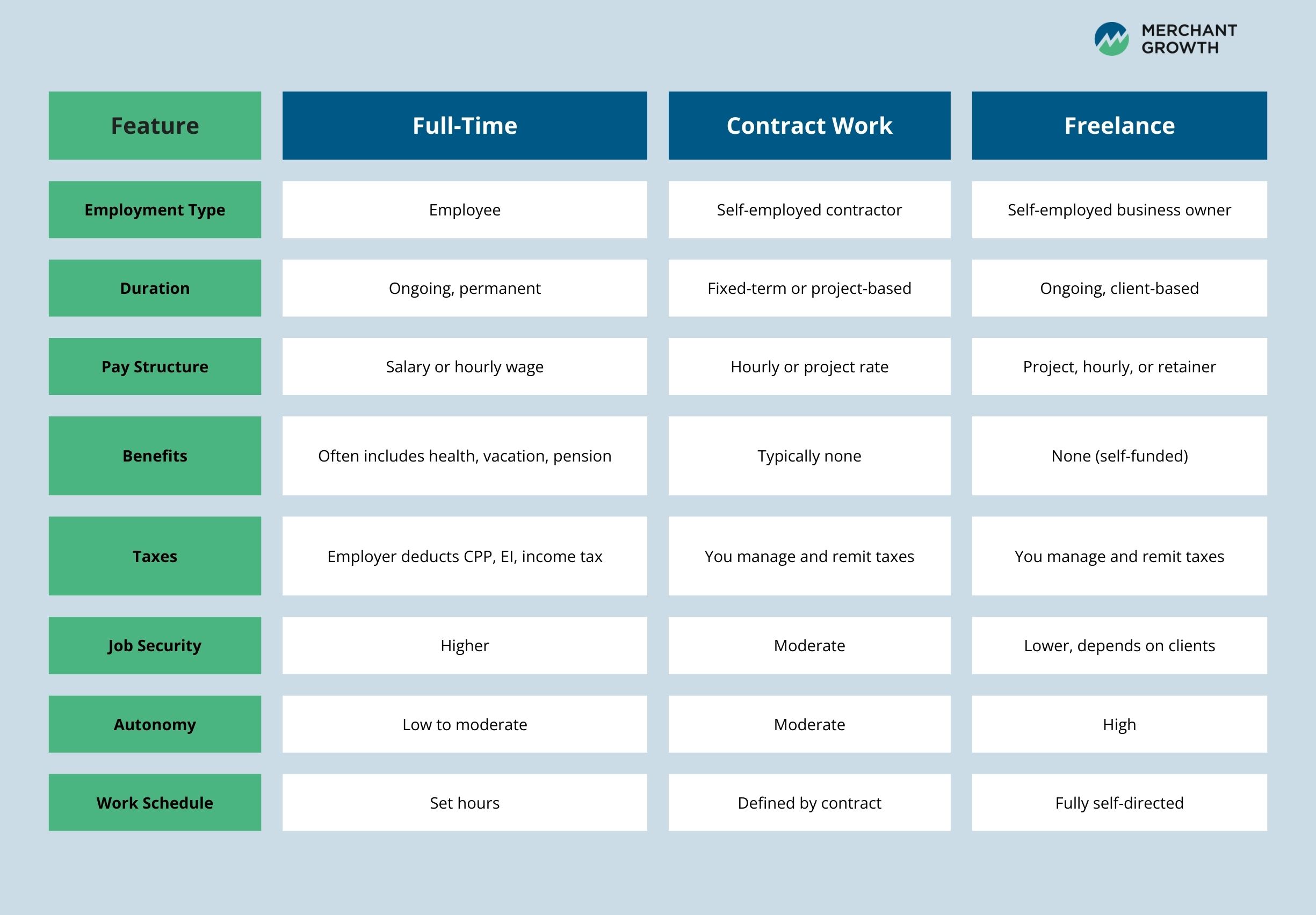

Full-Time employment

Full-time employment is the most traditional path. You work for one employer on an ongoing basis, receive a consistent paycheck, and usually have access to benefits such as extended health coverage, paid vacation, and sometimes retirement plans. This option appeals to people who value stability, predictable income, and clear career progression within an organization.

Contract work

Contract work sits between full-time employment and freelancing. Contractors are typically hired for a specific role, project, or time period. While you may work similar hours to full-time employees, you are paid a higher hourly or project rate instead of receiving benefits. Contract work is common in industries like technology, healthcare, engineering, and marketing, and it often appeals to professionals who want flexibility while still working with established organizations.

Freelancing

Freelancers operate as independent businesses. You work with multiple clients, set your own rates, and control when and how you work. This model offers the greatest flexibility and variety, but also comes with more responsibility. Freelancers handle their own marketing, invoicing, taxes, and expenses, and income can fluctuate from month to month. Many Canadians choose freelancing for the autonomy it provides, especially in creative, digital, and professional service industries.

Full-Time, Contract, and Freelance Work Compared

How the CRA Defines Employees vs. Contractors

In Canada, the Canada Revenue Agency (CRA) determines whether someone is an employee or a contractor based on the actual working relationship, not the job title. The CRA looks at factors such as control (who decides how the work is done), ownership of tools, chance of profit and risk of loss, and how integrated the worker is into the business. Understanding this distinction matters because it affects taxes, deductions, and eligibility for benefits.

If you are considering contract or freelance work, reviewing the CRA’s guidance on employment classification can help you avoid misclassification issues and plan properly for taxes and financial obligations.

The Pros and Cons of Contract, Freelance, and Full-Time Employment

There is no single “right” way to work. The best option depends on what you value most at this stage of your career, whether that is stability, flexibility, income potential, or independence. Understanding the trade-offs of each work style can help you choose a path that supports both your professional goals and your personal priorities.

Below is a side-by-side comparison of the most common advantages and challenges associated with full-time employment, contract work, and freelancing in Canada.

| Work Type | Pros | Cons |

|---|---|---|

| Full-Time | – Reliable, steady income – May include employer-covered benefits (health, vacation, retirement) – Job security and career path opportunities |

– Less flexibility in schedule and location – Limited control over workload or projects |

| Contract Work | – Higher hourly or project pay – More control over work environment and schedule – Exposure to varied industries and roles |

– Typically no benefits or paid leave – Income depends on contract availability – Responsible for own taxes |

| Freelance | – Maximum flexibility and independence – Ability to choose clients and projects – Opportunity to build a personal brand |

– Irregular income – Must self-manage taxes, insurance, and retirement – Requires constant self-promotion |

When reviewing these options, it helps to think beyond just income. Consider how much flexibility you want, how comfortable you are with financial uncertainty, and whether you prefer structure or autonomy in your day-to-day work. Many Canadians move between these models over time, starting in full-time roles, transitioning into contract work, and eventually freelancing or running a business of their own. The goal is not to pick a permanent label, but to choose the model that best fits your current needs and long-term plans.

Top Industries for Contract Work in Canada

Contract work has become a core part of the Canadian labour market, particularly in industries where demand fluctuates, projects are time-bound, or specialized skills are required. In fact, 70% of employers report plans to increase their use of contract workers and freelancers, reflecting a long-term shift toward more flexible workforce models. While contract opportunities exist across most sectors, some industries consistently rely on independent talent to stay agile and competitive.

Technology and IT

Technology continues to lead when it comes to contract work. Companies often bring in contract professionals to support software development, cybersecurity initiatives, system migrations, or short-term product launches. The fast pace of innovation makes flexible talent especially valuable, allowing businesses to scale expertise without long-term commitments. Roles such as software developers, UI and UX designers, and cybersecurity analysts remain in steady demand, particularly in areas related to cloud infrastructure, artificial intelligence, and data security.

Healthcare

Contract work plays a critical role in healthcare, especially where staffing shortages or regional demand create gaps. Travel nurses, locum physicians, and medical coders are frequently engaged to ensure continuity of care in hospitals, clinics, and long-term care facilities. These roles often require specific licensing and certifications, but they offer professionals the ability to work across locations while maintaining a flexible schedule.

Marketing and creative services

Marketing and creative fields have long embraced contract and freelance models. Businesses often hire specialists for campaign launches, rebrands, website projects, or content creation rather than building permanent in-house teams. Writers, graphic designers, video producers, and digital marketers are commonly engaged on a project basis, with demand particularly strong for professionals who understand digital channels and brand storytelling.

Finance and consulting

In finance and consulting, contract roles are frequently tied to audits, budgeting cycles, system implementations, or strategic initiatives. Accountants, financial analysts, and business consultants may be brought in to provide targeted expertise during peak periods or times of change. These roles are often well-compensated but require strong credentials and the ability to deliver results within defined timelines.

Together, these industries highlight why contract work continues to grow. Businesses gain flexibility and specialized expertise, while professionals gain access to varied projects, income opportunities, and career mobility.

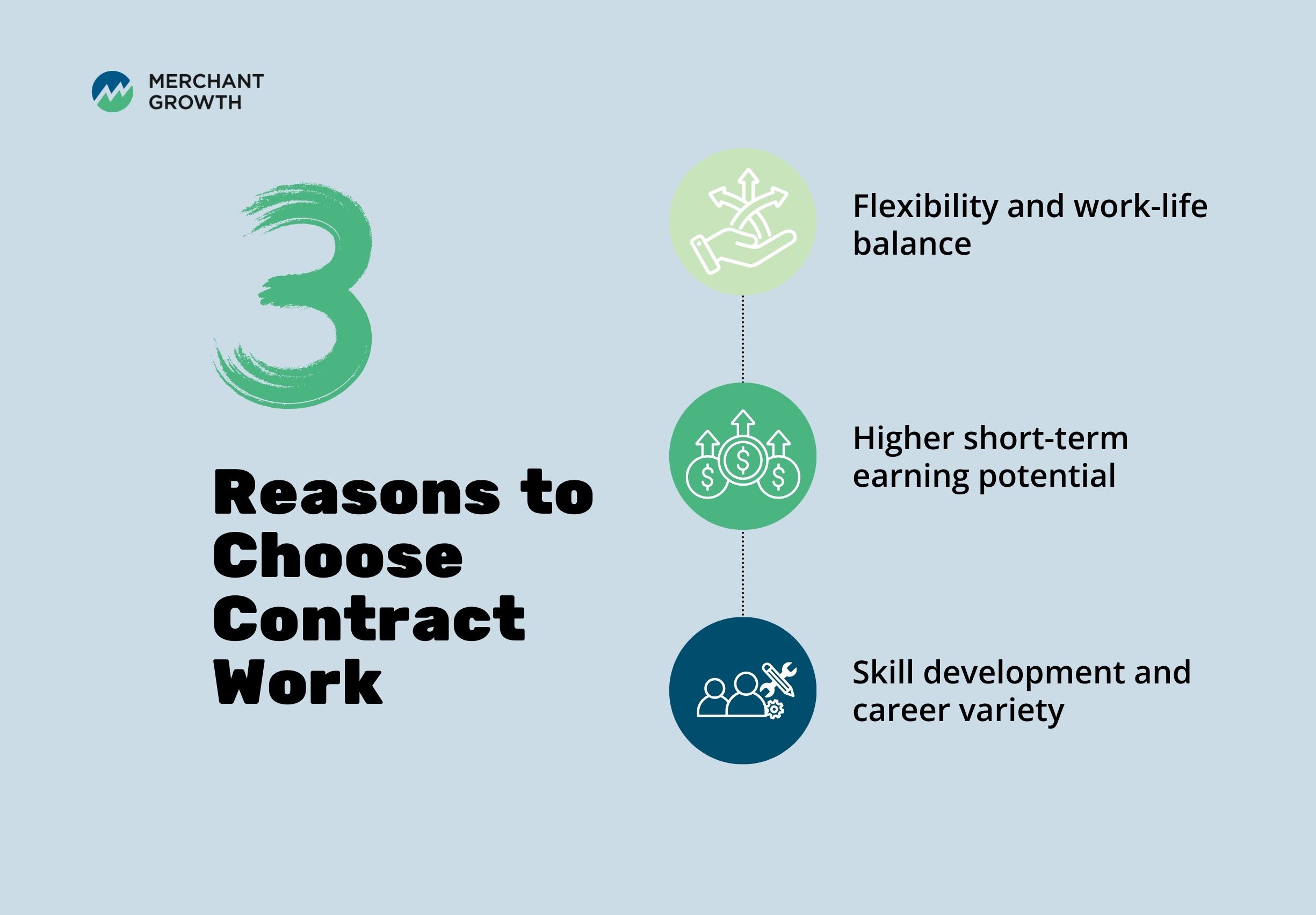

Why Many Canadians Choose Contract Work Over Full-Time Roles

Contract work is not simply an alternative to full-time employment. For many Canadians, it is a deliberate choice shaped by lifestyle goals, career priorities, and changing expectations about work. While it is not the right fit for everyone, contract roles offer advantages that traditional employment may not provide at certain stages of life.

Flexibility and work-life balance

One of the most common reasons people move into contract work is flexibility. Contractors often have greater control over their schedules, locations, and workloads. This can be especially valuable for parents, caregivers, or individuals seeking better balance between personal and professional responsibilities. Remote and hybrid contract roles also reduce commute time, giving people back hours each week.

Higher short-term earning potential

In many industries, contract professionals earn higher hourly or project-based rates than salaried employees performing similar work. For individuals focused on accelerating savings, paying down debt, or building a financial cushion, contract work can provide a faster path toward those goals. This model works particularly well for people whose benefits are covered elsewhere or who prefer to manage them independently.

Skill development and career variety

Contract work exposes professionals to different teams, tools, and challenges in a shorter time frame. This variety accelerates learning and builds a diverse skill set that can increase long-term career value. For example, a marketing consultant may work with a startup on brand positioning, then support an established company with digital campaigns, gaining insights that would take years to acquire in a single role.

Ultimately, many people choose contract work because it aligns more closely with how they want to live and grow. Whether the goal is flexibility, income growth, or professional variety, contract roles offer an alternative path that can evolve alongside changing personal and career priorities.

Flexible Work Models: Contract vs. Freelance Explained

Contract and freelance work are often grouped together because both offer more flexibility than traditional employment. However, the day-to-day realities, responsibilities, and risks are quite different. Understanding these differences is especially important if you are considering independent work for the first time.

Compensation and pay structure

Contract workers are typically hired for a defined role or project and are paid an agreed hourly or project rate. That rate is often higher than a salaried position because it accounts for the lack of long-term security. Freelancers also set their own rates, but income can vary significantly month to month depending on how many clients they secure and how consistently work flows in.

Benefits and expenses

Contractors usually do not receive benefits like health coverage, paid vacation, or retirement contributions. Freelancers face the same reality, but with added responsibility. Freelancers must also cover business expenses such as software, equipment, insurance, and marketing costs. In both cases, planning ahead for benefits and time off is essential.

Flexibility and control

Freelancers have the highest level of control. They choose their clients, set their schedules, and decide which projects to accept. Contractors typically have more structure. While contracts are temporary, contractors often work set hours and follow company processes during the contract period. This can feel closer to full-time work, just without permanence.

Job security and stability

Full-time roles offer predictability, while flexible work trades stability for opportunity. Contracts can end when projects wrap up or budgets change. Freelancers face even more variability, as they are responsible for continuously finding new work. The upside is freedom and growth potential, but it requires strong financial planning and comfort with uncertainty.

Choosing between contract and freelance work is less about titles and more about how much responsibility you want to carry. Contract work can be a stepping stone into flexible employment, offering independence without fully running a business. Freelancing suits those ready to manage income swings, taxes, and client relationships in exchange for maximum autonomy.

Taxes, Deductions, and Legal Responsibilities in Canada

How you work doesn’t just affect your schedule and income. It also changes how you’re taxed, what you’re responsible for legally, and how much planning you need to do throughout the year. Understanding these differences upfront can help you avoid surprises and stay onside with the Canada Revenue Agency.

How taxes work for full-time employees

If you are a full-time employee, taxes are relatively straightforward. Your employer automatically deducts income tax, Canada Pension Plan contributions, and Employment Insurance premiums from each paycheque. At year end, you receive a T4 summarizing your earnings and deductions, which you use to file your personal tax return. Most employees do not need to worry about setting money aside or making installment payments because those obligations are handled at the payroll level.

How taxes work for contractors and freelancers

Contractors and freelancers are treated as self-employed individuals in most cases. This means taxes are not deducted at source. You are responsible for calculating and remitting your own income tax, Canada Pension Plan contributions, and, in some situations, Employment Insurance if you opt in voluntarily.

If your annual revenue exceeds the small supplier threshold, you must also register for and charge GST or HST, collect it from clients, and remit it to the CRA on schedule. Because nothing is withheld automatically, many independent workers set aside a portion of every payment to avoid cash flow strain at tax time.

One advantage of self-employment is the ability to deduct legitimate business expenses. Common deductions include home office costs, software subscriptions, professional fees, equipment, marketing, and a portion of phone or internet expenses used for work. Keeping detailed records and receipts is essential.

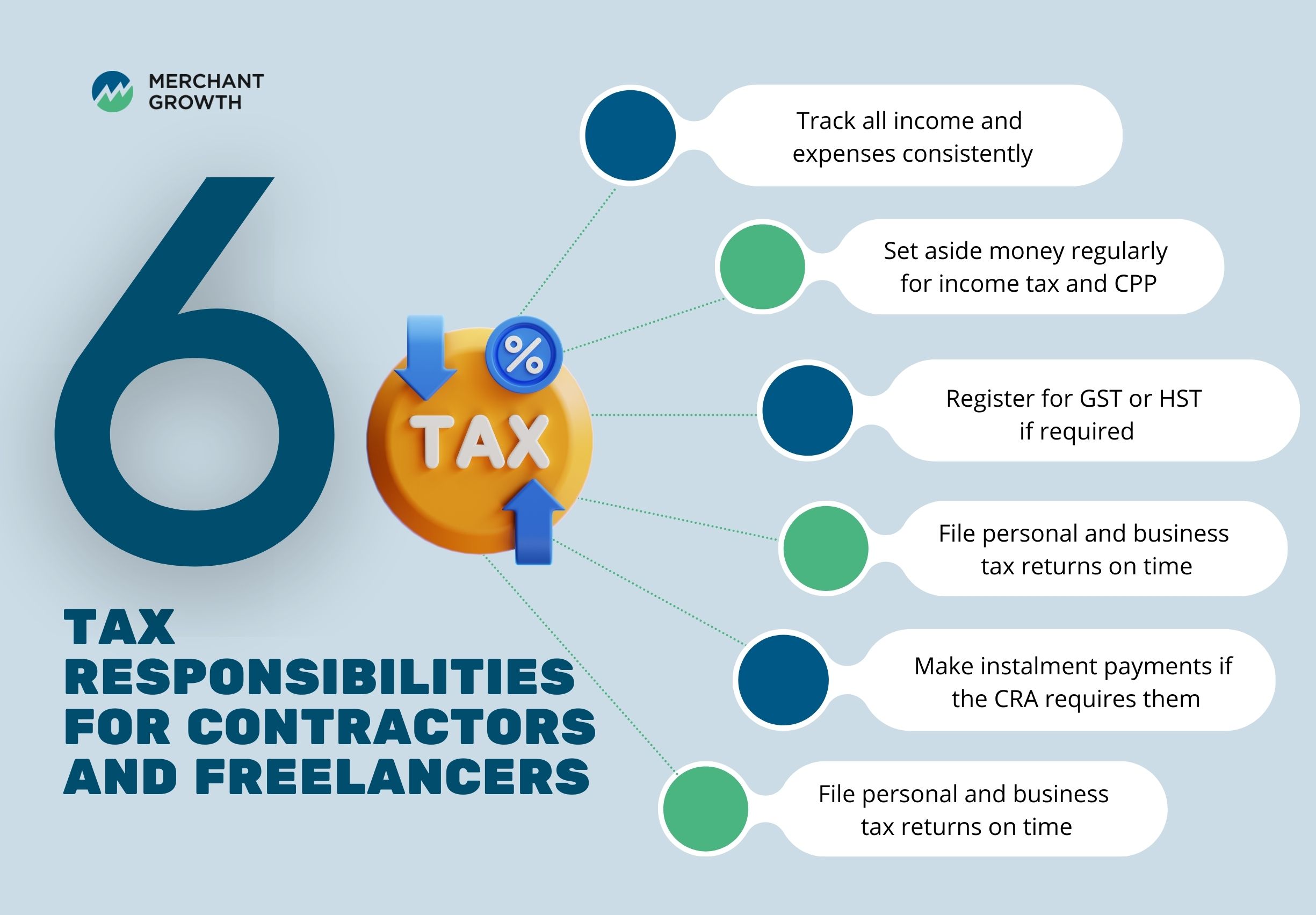

Tax responsibilities for contractors and freelancers

If you are working independently, this checklist can help you stay organized:

- Track all income and expenses consistently

- Set aside money regularly for income tax and CPP

- Register for GST or HST if required

- File personal and business tax returns on time

- Make instalment payments if the CRA requires them

- Keep records and receipts for at least six years

CRA classification and misclassification risks

The CRA distinguishes between employees and independent contractors based on factors such as control over work, ownership of tools, financial risk, and integration into the business. Misclassification can create serious issues. If a worker is treated as a contractor but should be considered an employee, the hiring company may be liable for unpaid payroll taxes, penalties, and interest.

For workers, misclassification can affect eligibility for benefits, tax deductions, and legal protections. If your work arrangement feels unclear, it is worth reviewing CRA guidance or speaking with a tax professional to confirm your status.

Understanding your tax and legal obligations early allows you to plan with confidence, protect your income, and choose the work structure that best supports your long-term goals.

Career Growth and Lifestyle Considerations

Beyond pay and taxes, the way you work has a real impact on how your career develops and how your day-to-day life feels. Full-time, contract, and freelance roles each offer different paths for growth, learning, and work-life balance. Understanding these differences can help you choose an option that supports both your professional goals and your personal priorities.

Career growth and skill development

Full-time roles often provide a more structured approach to career development. Employees typically have access to formal training programs, mentorship, performance reviews, and clearly defined promotion paths. Working within a single organization also makes it easier to build long-term relationships, gain institutional knowledge, and move into leadership roles over time. For people who value stability and a clear trajectory, this structure can be a major advantage.

Contractors, by contrast, tend to build their skills through variety rather than hierarchy. Working across multiple projects, teams, or industries can accelerate learning and broaden expertise quickly. However, professional development is largely self-directed. Contractors need to actively pursue certifications, networking opportunities, and new challenges if they want to continue advancing.

Freelancers experience growth differently again. Because they are effectively running their own businesses, skill development often includes both technical expertise and business skills like pricing, negotiation, marketing, and client management. This can be incredibly empowering, but it requires initiative and ongoing investment in learning.

Lifestyle and work-life balance

Lifestyle considerations are often the deciding factor for many professionals. Full-time employment offers predictability. Set hours, steady income, and defined time off make it easier to plan family commitments, vacations, and long-term financial goals. For some, this consistency reduces stress and supports a healthier work-life balance.

Contract and freelance work provide greater flexibility but come with trade-offs. Independent workers often have more control over when and where they work, which can be ideal for parents, caregivers, or people who value autonomy. At the same time, they must manage administrative tasks like invoicing, contracts, taxes, and client communication.

For example, a freelance developer may enjoy choosing projects that align with their interests and working remotely, but they are also responsible for finding clients, negotiating rates, and ensuring they get paid on time. That freedom can be rewarding, but it requires discipline and strong organizational habits.

Ultimately, there is no universally “better” option. The right choice depends on how you want to grow, how much structure you prefer, and how you want work to fit into your life.

Risks and Financial Management for Contractors

Contract and freelance work offer flexibility and income potential, but they also come with financial realities that full-time employees rarely have to manage on their own. Without a guaranteed paycheck or employer-provided safety net, independent workers need to be more intentional about planning, cash flow, and risk management.

One of the biggest challenges contractors face is income variability. Some months may be highly profitable, while others are slower or unexpectedly quiet. Contracts can end with little notice, clients may delay payments, and work can be seasonal depending on your industry. This unpredictability makes financial discipline especially important, not just for covering day-to-day expenses, but for maintaining peace of mind.

Managing Irregular Income Like a Pro

Successfully navigating irregular income starts with building strong financial habits. Setting aside money for taxes is critical, as contractors are responsible for remitting income tax, CPP, and potentially GST or HST themselves. A separate savings account for tax obligations can prevent unpleasant surprises at filing time.

An emergency fund is equally important. Many independent professionals aim to save three to six months of essential expenses to cover gaps between contracts or slower periods. This buffer gives you flexibility to choose better opportunities instead of feeling pressured to accept any work that comes along.

Using accounting and budgeting tools can also make a significant difference. Tracking income, expenses, and upcoming invoices helps you understand cash flow patterns and plan ahead. When you can clearly see which months tend to be slower or which clients take longer to pay, it becomes easier to adjust spending or prepare in advance.

Even with careful planning, there may be times when cash flow gaps arise. This is where financing can play a strategic role. Term financing, such as the options offered by Merchant Growth, can help contractors smooth income between contracts, cover short-term expenses, or invest in tools and training that support long-term earning potential. Used thoughtfully, financing provides breathing room without disrupting your momentum or forcing you to pause your work.

Independent work rewards flexibility and initiative, but it also requires a proactive approach to financial management. By planning for variability and using the right tools and resources, contractors can reduce risk and create a more stable, sustainable way of working.

How to Succeed as a Contractor or Freelancer

Choosing contract or freelance work is only the first step. Long-term success depends on how well you position yourself, manage your workload, and plan for growth. Independent work rewards initiative, but it also requires structure. Contractors and freelancers who treat their work like a business, even when they are just starting out, tend to be more resilient, confident, and financially stable over time.

Build a strong portfolio and personal brand

Your portfolio is often your first impression, and in many cases, it replaces a traditional resume. A simple website that highlights your services, past projects, and client results helps establish credibility. Keeping your LinkedIn profile up to date, sharing insights related to your field, and collecting testimonials from satisfied clients all reinforce your expertise. Even early in your journey, documenting real work, side projects, or pilot contracts can make a meaningful difference.

Create consistent visibility for new opportunities

Contract work rarely comes from a single source. Many professionals combine online platforms, referrals, networking, and direct outreach to keep their pipeline active. Staying visible means regularly letting people know what you do and what problems you solve. This could be as simple as posting updates on LinkedIn, attending industry events, or reconnecting with former colleagues. Over time, this consistency reduces the stress of finding your next contract.

Set rates with clarity and confidence

Pricing is one of the most common challenges for independent workers. Strong rates are based on market research, experience, and the value you deliver, not just hours worked. Whether you charge hourly or per project, clear pricing sets expectations and builds trust. As demand for your skills grows, revisiting your rates ensures your income keeps pace with your expertise and workload.

Success as a contractor or freelancer does not come from doing everything at once. It comes from building solid habits, refining your positioning, and making thoughtful decisions that support sustainable growth.

Hybrid Models and Modern Work Trends

Work is no longer a simple choice between full-time employment and independent contracting. Many businesses and professionals are now meeting in the middle through hybrid work models that offer flexibility without fully committing to one structure. These arrangements are becoming increasingly common across Canada as companies adapt to remote work, talent shortages, and project-based demands.

One popular option is the contract-to-hire model. In this setup, a professional is brought on as a contractor for a defined period, with the possibility of transitioning into a full-time role if the fit is right. This allows both the worker and the employer to assess skills, culture fit, and long-term needs before making a permanent commitment.

Part-time contracting is another growing trend. Professionals may work on a reduced schedule for one or more companies, balancing steady income with flexibility. This model is common in roles like marketing, IT support, finance, and HR, where businesses need ongoing expertise but not a full-time presence.

Many Canadian employers are also adopting mixed workforce structures. These teams combine full-time employees with contractors and freelancers to scale up or down as needed. For example, a tech company might rely on full-time developers for core products while hiring contract specialists for cybersecurity audits or short-term development sprints. Retail and e-commerce businesses often use contractors during peak seasons, while professional service firms bring in freelance designers, writers, or analysts for specific client projects.

At the same time, freelance platforms and remote work tools are making it easier than ever to connect talent with opportunity. Professionals can now work with companies across provinces or internationally, while employers gain access to a broader talent pool without geographic limitations. These shifts reflect a larger move toward flexibility, adaptability, and outcome-focused work rather than rigid employment structures.

Employer Perspective: Choosing the Right Hire

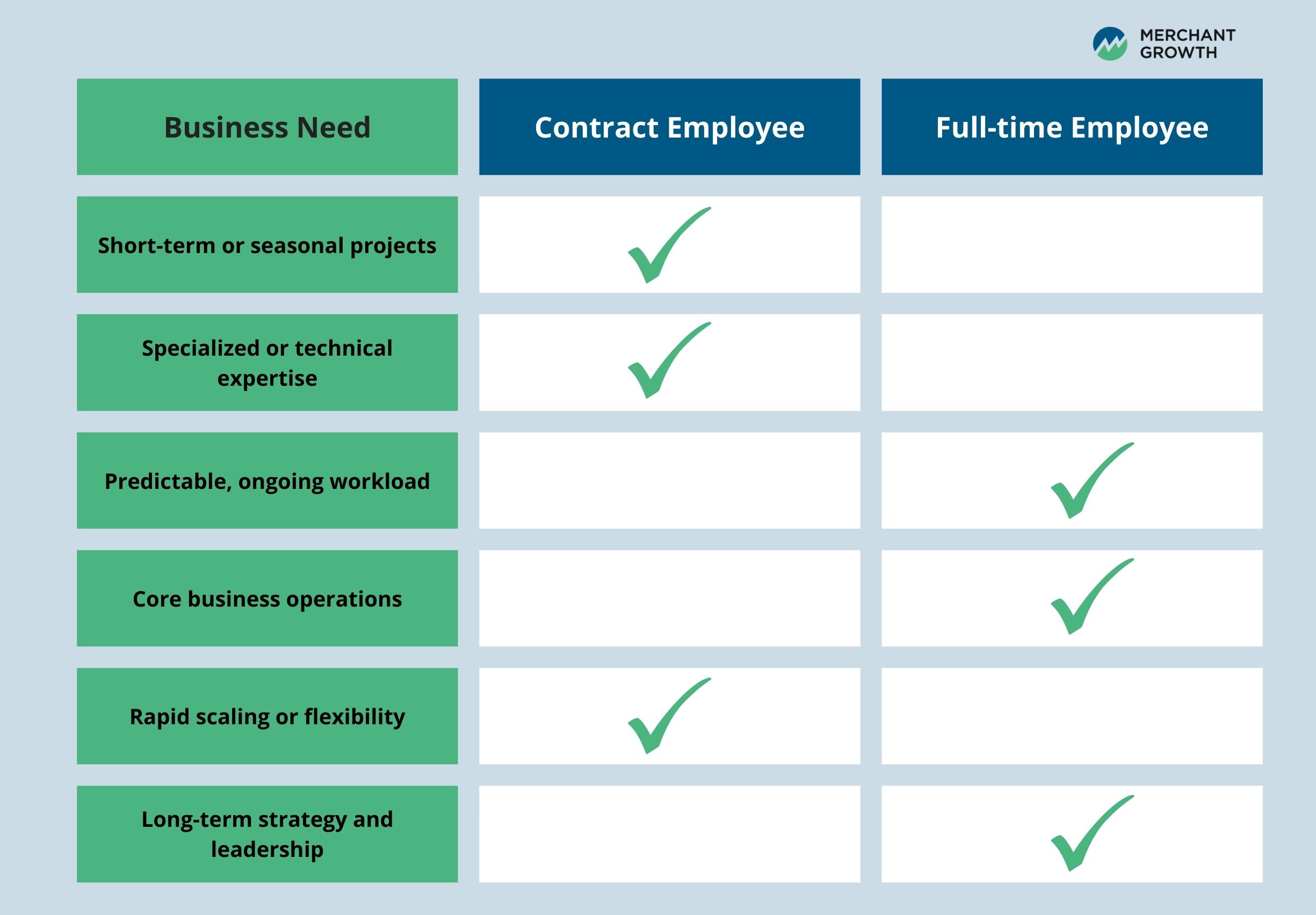

For business owners, the decision between hiring a full-time employee or engaging a contractor is both strategic and financial. Each option offers distinct advantages, and the right choice depends on your operational needs, budget, and long-term goals.

Contractors provide flexibility. They can be brought in quickly, scaled up or down, and hired for specialized skills without long-term commitments. This makes them ideal for seasonal demand, short-term projects, or highly technical work that is not needed year-round. However, contractors typically come at a higher hourly or project cost and offer less control over schedules and workflows.

Full-time employees, on the other hand, offer stability and continuity. They are more deeply integrated into the business, understand internal systems, and contribute to long-term growth and culture. Hiring full-time also reduces the risk of turnover during critical projects and helps build institutional knowledge. The trade-off is higher fixed costs, including salaries, benefits, payroll taxes, and onboarding time.

Compliance is another important factor. Misclassifying workers can lead to penalties, back taxes, and legal issues. Employers must ensure contractors meet CRA criteria for self-employment, including control over work, ownership of tools, and independence from the organization. When in doubt, seeking professional advice can help avoid costly mistakes.

When to Hire a Contractor vs. a Full-Time Employee

Many businesses use a blend of both to stay agile while maintaining a strong core team. By matching the type of work to the right hiring model, employers can control costs, reduce risk, and build teams that support sustainable growth.

These decisions also tie closely to cash flow and planning. Flexible workforce models often work best when businesses have access to financing that helps manage payroll, project costs, or growth periods. In this way, workforce strategy and financial strategy go hand in hand, supporting both operational stability and long-term success.

Take the quiz to see what type of hire is best for your business.

Ready for Flexible Work? Find Out If Contract or Freelance Life Fits You

Thinking about contract or freelance work is exciting, but it’s also a big shift in how you earn, plan, and manage your career. Before making the leap, it’s worth taking a moment to reflect on what this kind of work really demands day to day.

Ask yourself a few honest questions:

- Do you enjoy variety, independence, and taking on new challenges regularly?

- Are you comfortable with income that may fluctuate from month to month?

- Can you stay organized when it comes to invoicing, taxes, and budgeting?

- Do you feel motivated working on your own without a traditional team or manager?

There’s no right or wrong answer. Contract and freelance work can be incredibly rewarding for the right person, but it works best when your lifestyle, financial habits, and career goals are aligned.

To help you decide with confidence, download our free worksheet. It walks you through practical considerations around income stability, taxes, lifestyle priorities, and long-term goals so you can determine whether flexible work is the right next step for you — or whether a hybrid or full-time path makes more sense right now.

Download the worksheet and map out your next move with clarity.

This keeps the tone encouraging and practical, while giving readers a clear, actionable takeaway at the end of the article.

Choosing the Path That Fits Your Career and Life

There is no single “best” way to work. Full-time roles, contract work, and freelancing all offer meaningful opportunities, and the right choice depends on your priorities, risk tolerance, and long-term goals. For some Canadians, stability, benefits, and predictable income matter most. For others, flexibility, autonomy, and control over how and when they work are worth the trade-offs.

As Canada’s job market continues to evolve, with more professionals moving toward contract, freelance, and hybrid models, understanding the financial and tax implications of each option is essential. Independent work can be rewarding, but it requires thoughtful planning around cash flow, taxes, and income variability. Taking time to assess your readiness and test different models can help you make decisions with confidence rather than pressure.

Ultimately, the most sustainable career is one that aligns with how you want to live and work. Whether you choose full-time employment, flexible contract work, or a mix of both, being informed and proactive puts you in control of your next step.

Top Home-Based Business Ideas in Canada (And How to Get Started)

More Canadians than ever are turning their homes into business headquarters—and for good reason. Running a business from home offers unmatched flexibility, low overhead, and the ability to launch with limited capital. Whether you’re freelancing, baking, tutoring, or building a product line, home-based entrepreneurship has become a powerful way to take control of your income and work-life balance.

According to Statistics Canada, over 2.5 million Canadians were self-employed in 2023, and a large portion of that figure includes home-based businesses. While the autonomy of being your own boss is a major draw, navigating the steps—from permits to promotion—can be overwhelming.

This guide will walk you through everything you need to get your home-based business started, from choosing a profitable idea to understanding zoning laws, marketing, and funding.

Key Takeaways

- Canada offers hundreds of viable home business ideas—online, creative, service-based, and more.

- Regulatory steps like permits and business registration vary by province but are essential.

- Low startup costs make home businesses accessible—especially with good planning.

- Local funding, training, and online marketing tools can accelerate success.

Why Home-Based Businesses Are Booming in Canada

Driven by post-pandemic lifestyle changes, rapid digital transformation, and a growing desire for flexibility, home-based entrepreneurship is gaining serious momentum across Canada. As remote work became the norm—rising from just 7% in 2016 to over 20% of Canadians working from home in 2023—many took it a step further by launching their own businesses. With no need for costly retail space and the freedom to set their own schedules, home-based businesses offer both practical and personal advantages.

While starting a business still takes planning and persistence, today’s digital tools and government resources make it more manageable than ever before.

Top Home-Based Business Ideas in Canada

When it comes to starting a business from home, most Canadian entrepreneurs gravitate toward one of two paths: digital services you can offer entirely online, or hands-on, locally-focused businesses that draw on your skills. Whether you're tech-savvy or creatively inclined, there’s a home-based business model that fits.

Online & Virtual Services

Digital services are among the easiest and most affordable home businesses to launch for Canadians. They require minimal overhead, can be done from anywhere with a reliable internet connection, and scale well as you grow your client base.

Virtual Assistant

Virtual assistants help businesses stay organized and efficient. With more small businesses outsourcing admin work, the demand continues to grow. You can offer scheduling, email management, customer service, or niche support like bookkeeping or marketing coordination. According to Ontario Business Central, entry-level VAs will start making anywhere from your provincial minimum wage - $25/hour, but as your experience increases, you can look to charge anywhere from $50/hour or more.

Why it’s appealing: Offers flexibility and the ability to specialize in administrative or industry-specific tasks.

Freelance Writing

Freelance writing is one of the most versatile home-based businesses you can launch in Canada. It offers complete control over your schedule and the freedom to work with a variety of clients—from blogs and startups to major corporations and government agencies. If you enjoy researching, storytelling, or simplifying complex topics, there’s likely a writing niche that fits your skills. Whether you're writing speeches, technical manuals, or social media copy, the pay scale varies widely based on the format, industry, and your experience level.

Here’s a look at the average hourly rates across different types of freelance writing:

| Writing Type | Hourly Rate ($/hour) |

|---|---|

| Speech Writing | $60 to $130 |

| Teaching/Instruction | $25 to $80 |

| Online/Website Writing | $60 to $100 |

| Government Writing | $50 to $125 |

| Newsletters | $50 to $80 |

| Advertising Material | $75 to $150 |

| Advertorials | $40 to $100 |

| Corporate/Business Writing | $50 to $125 |

Reference: Canada Freelance Guild

Why it’s appealing: Great for strong communicators with subject-matter expertise who enjoy working independently.

Social Media Management

Many small businesses need help managing their social channels. If you’re creative and savvy with platforms like Instagram and TikTok, this is a scalable business with strong income potential. Freelancers in Canada typically charge between $25 to $100 per hour for social media management, with monthly packages ranging from $500 to $2,000, depending on the scope of services, according to data from Jeff Social. With more experience and higher-profile clients, there’s also potential to earn significantly more, especially if you offer strategy, paid ad management, or content production in addition to day-to-day posting.

Why it’s appealing: Fast-growing demand, creative flexibility, and potential for recurring clients.

Bookkeeping

Bookkeepers are always in demand. This business offers stable, repeat work and allows for remote client relationships once trust is built—ideal for those who are detail-oriented and comfortable with numbers. According to the Canadian Job Bank, bookkeepers in Canada typically charge between $18.46 and $42.05 per hour. This wide range reflects varying levels of experience, certification, and specialization, so if you build strong relationships and perhaps expand into additional services like financial reporting or bookkeeping software support, you can command higher rates and build a reliable, home-based bookkeeping business.

Why it’s appealing: Recession-resistant, reliable work with a path to certification.

Online Tutoring

Online tutoring lets educators and bilingual professionals share their expertise in subjects like math, science, ESL, or standardized test prep. It’s flexible and in high demand among parents and adult learners. According to Tutor Lyft, the starting rate for tutoring through an agency is typically around $45 per hour, but this can rise to $80 or more depending on the subject, tutor qualifications, and delivery method. One-on-one sessions and in-person formats generally cost more than group or online tutoring, making virtual tutoring a particularly attractive and accessible business model for home-based educators.

Why it’s appealing: Makes use of existing teaching skills and offers a meaningful way to help others.

Graphic designer

Running a graphic design business from home gives you the freedom to be creative while keeping startup costs low. Whether you focus on branding, logos, packaging, web graphics, or social media content, there’s no shortage of demand. Most designers work remotely with clients, using digital tools to collaborate and deliver polished, professional work. In Canada, freelance designers typically earn between $19 and $50 per hour, with higher rates for specialized or complex projects. Building a strong online portfolio and actively reaching out to clients are both essential to growing a successful design business.

Why it’s appealing: High demand across industries, flexible hours, scalable workload, and a great fit for creative professionals who want to work independently.

Creative & Specialized Services

These businesses are rooted in hands-on skills or local service needs. They may require more upfront investment or licensing, but can be incredibly rewarding and profitable, especially when tailored to your community’s demand.

Esthetician/Beauty Services

From lash extensions and brow waxing to facials and spray tanning, beauty services are consistently in demand—and can be successfully run from a well-equipped home studio. Certified estheticians often specialize in specific services, which helps keep overhead costs low while building a loyal, returning client base. In Canada, estheticians typically earn around $18–$29 per hour, though rates can vary significantly depending on the service. For example, full lash sets may range from $80–$200, while brow services generally start around $15–$25. Many beauty professionals operate by appointment only, offering greater flexibility and control over their schedules.

Why it’s appealing: Low startup costs, high potential for repeat business, and the ability to specialize and grow within a thriving self-care market.

Hair Stylist

Hair styling is one of the most resilient personal service businesses in Canada, thanks to consistent demand and loyal clientele. Independent stylists operating from a home studio can avoid the overhead costs of renting a chair or commercial space, keeping more of their earnings. Most Canadian hairstylists begin with an hourly wage of $18/hour and with time can make more than $30 per hour, depending on experience and services offered. Many also develop long-term relationships with clients, leading to steady repeat visits and a reliable stream of income.

Why it’s appealing: Steady demand, strong potential for client loyalty, and a creative career path with room to grow.

Photography

Running a photography business from a home studio offers creative freedom and the flexibility to specialize in areas like portraits, branding, product shoots, or family sessions. While working from home can save significantly on studio rent, it’s still important to budget for insurance, equipment, and online marketing. In Canada, beginner photographers typically earn between $25–$75 per hour, while experienced professionals can charge anywhere from $250–$500 per hour, depending on the shoot type and expertise. Many home-based photographers also boost income by offering packages and seasonal mini sessions, which help generate steady, repeat business.

Why it’s appealing: Flexible scheduling, creative expression, and the potential to grow through referrals and repeat clients.

Therapy

Licensed therapists and counsellors can operate a professional practice from a dedicated home office, provided they meet provincial regulations and privacy standards. With increased demand for mental health services in Canada, therapists can charge between $90–$250 per session. Offering virtual appointments also expands reach and accessibility, especially for clients in rural areas.

Why it’s appealing: Meaningful, purpose-driven work with the flexibility of remote or in-home appointments and consistent client demand.

Dog Grooming

A home-based dog grooming setup can be a rewarding business for animal lovers. With minimal space and a few specialized tools, groomers can provide services like haircuts, bathing, nail trimming, and de-shedding treatments right from home. In Canada, grooming fees typically range from $50 to $100+ per dog depending on the breed, size, and complexity of services. Many pet owners become repeat clients, booking regular appointments and helping to create a stable, predictable income stream.

Why it’s appealing: A niche with loyal customers, repeat business, and the ability to scale with recurring appointments.

Pet Sitting

For animal lovers, pet sitting is a rewarding and flexible business you can run from home or by visiting clients. Whether offering overnight stays or day care, pet sitting is always in demand, especially in urban areas. In Canada, rates typically range from $17.50 –$28 per hour, depending on services and location.

Why it’s appealing: Low overhead, flexible scheduling, and the chance to build a loyal base of furry clients and their owners.

Daycare/Childcare

If you love working with children, running a daycare from home can be both personally fulfilling and financially stable. It’s also a business that meets a major need in communities across Canada, where affordable childcare is in high demand.

There are two primary models: licensed and unlicensed home daycare. Most provinces allow unlicensed childcare providers to care for a small number of children (often 2–5, depending on the province) without needing a license. This option has lower startup costs and fewer regulatory hurdles, making it more accessible for those just starting out.

Licensed home daycares, on the other hand, must meet stricter requirements around space, safety standards, staffing ratios, and daily operations. While becoming licensed can make your daycare more attractive to families—especially since many provincial childcare subsidies only apply to regulated care—it often requires a greater upfront investment. In some cases, this might mean renovating or purchasing a home to meet compliance standards, bringing it closer in cost and complexity to a commercial daycare setup.

In Canada, childcare providers typically charge between $20 and $58 per day, though this varies by region, child age, and the services offered.

Personal Trainer (Home or Virtual)

With the growing demand for fitness at home, certified personal trainers can run sessions from a home gym or virtually via video. Specializing in areas like strength training, mobility, or weight loss can help carve out a niche. Hourly wages in Canada typically start around $18/hour and extend beyond $30/hour, depending on experience and session type.

Why it’s appealing: Low equipment investment, flexible schedule, and the ability to build strong client relationships.

Private Pilates or Yoga Instructor

Teaching private yoga or Pilates sessions from a home studio—or virtually—is a calming and fulfilling career path for wellness-focused entrepreneurs. Instructors often offer one-on-one programs or small group packages, with rates typically ranging from $20–$120 per session, depending on experience and format. While session fees vary, the average take-home wage for Canadian instructors falls between $17 and $32 per hour. There’s also room to grow by expanding into workshops, retreats, or corporate wellness offerings.

Why it’s appealing: Combines wellness with entrepreneurship, builds community, and allows for creative program design in your own space.

Sustainable Product Maker

Eco-conscious products like reusable bags, soy candles, beeswax wraps, or natural skincare are growing in popularity as more consumers seek sustainable alternatives to everyday items. If you're crafty or already making these products as a hobby, turning your passion into a home-based business could be a natural next step. Profit margins in this space can vary widely depending on the type of product, material costs, and whether you sell directly to consumers or through retailers or online marketplaces. Handmade, small-batch goods with premium branding often command higher prices, while simpler or bulk items may rely on volume sales. Regardless, this niche allows for creativity, flexibility, and alignment with environmentally conscious values.

Why it’s appealing: Aligns with environmental values and allows for creative expression.

Profitable Mobile Business Ideas with a Home Base

Running a business from home doesn’t always mean staying home. Many Canadian entrepreneurs operate mobile businesses—where your home serves as your headquarters, but the work takes you out into the community. This model lets you keep overhead low, skip the storefront, and serve clients directly at their homes, job sites, or events. Whether you’re a creative professional, service provider, or consultant, there are countless ways to turn your skills into income with a flexible, home-based setup and a mobile service approach.

Home Cleaning

Home and office cleaning services are in steady demand, making this a reliable and scalable home-based business option. You can start solo with minimal equipment, then gradually expand by hiring staff or offering specialized services such as deep cleans, move-in/move-out packages, or post-renovation cleanup. One of the biggest advantages of this industry is flexibility—you set your hours, choose your clients, and determine your service area. Rates vary across the country, but here’s a general breakdown of average hourly cleaning rates by province:

| Province | Average Hourly Rate |

|---|---|

| Ontario | $25 – $35 |

| British Columbia | $20 – $30 |

| Alberta | $22 – $32 |

| Quebec | $18 – $28 |

| Nova Scotia | $20 – $30 |

Reference: No More Chores

Note: These rates are approximate and can vary based on factors such as property size, the number of rooms, and specific services provided. It’s always a good idea to check local rates to stay competitive.

Why it’s appealing: High demand, easy to start, and scalable with repeat clients.

Mobile Notary

Mobile notaries in Canada verify legal documents for individuals and businesses, often by travelling directly to clients’ homes or offices. Fees typically range from $50 to $199, including base travel costs and standard notarization charges. It’s a low-overhead, flexible business model ideal for those with a professional demeanour and attention to detail. To operate legally, you must be commissioned as a notary public or commissioner for oaths through your province or territory—requirements usually include being at least 18 years old, a Canadian citizen or permanent resident, and completing any necessary applications, training, or certifications.

Why it’s appealing: Professional, flexible, and needed across industries.

Personal Chef

If you love cooking, offering in-home meal prep or catering services is a fantastic business option. Busy families and individuals with dietary needs often seek out personal chefs, and the best part is, you don’t need formal culinary training to get started. Many chefs begin as passionate home cooks. The role offers flexibility, no late-night restaurant hours, and the chance to work closely with clients to create customized meals that fit their tastes and dietary needs. It’s a fulfilling business that blends creativity with personal connection.

Why it’s appealing: Great for food lovers who enjoy working one-on-one with clients and customizing meals.

Dog Walker

Dog walking is a simple, scalable business that combines exercise, fresh air, and reliable income. Popular in busy neighbourhoods and condo-dense cities, dog walkers can earn $15–$30 per walk (more for group outings or longer sessions). Apps like Rover or Pawshake can help you get started, but many successful walkers build direct relationships with clients.

Why it’s appealing: Great for active entrepreneurs, requires minimal startup costs, and offers consistent demand.

Event Planner

Whether it’s weddings, corporate functions, or milestone celebrations, event planning is an ideal business for detail-oriented, organized individuals. You can run most aspects of the business from home, managing timelines, vendor coordination, and budgets remotely. Canadian event planners typically charge between $25–$100+ per hour, depending on experience, or they may opt for a flat rate based on 10–15% of the total event budget. This flexible pricing structure allows planners to tailor services to a range of client needs while maintaining profitability.

Why it’s appealing: Offers creative freedom, the chance to work on exciting events, and high earning potential for experienced planners.

Property Manager

Managing rental properties on behalf of landlords—especially in vacation or long-term rental markets—can be a lucrative home-based business. Responsibilities may include tenant communication, maintenance coordination, and rent collection. In Canada, property managers can earn a flat fee or a percentage of monthly rental income (often 6–12%).

Why it’s appealing: Reliable monthly income, scalable with multiple properties, and ideal for those with admin or real estate experience.

Permits, Licenses & Business Structure: What You Need to Know

Before you mix your first batch of candles or log into your client dashboard, it’s important to ensure your business meets local regulations. Home-based businesses in Canada are subject to a range of requirements—some set federally, others provincially or municipally. Understanding these early can save you legal and financial headaches down the road.

Home-Based Business Permits & Licenses

Even a small, home-run operation needs to be properly licensed. Depending on your industry and location, this could include zoning permissions, health inspections, or operating licenses.

- Zoning: Your municipality may require a “home occupation” permit.

- Food/Childcare: Health inspections and safety standards may apply.

- Helpful Link: Ontario Ministry of Health Home-Based Food Business Guide

- National Info: Canada.ca Business Licensing

Check with your local municipality and province to determine what types of licenses or permits are required for your specific business type. Most home businesses need at least basic registration, and depending on what you offer—especially food, childcare, or personal services—you may need health inspections or special permissions to operate out of your home.

Choosing the Right Structure (Sole Proprietor vs Incorporation)

Your business structure affects everything from taxes and liability to how you register your business.

- Sole Proprietor: Easier and less expensive to set up; ideal for single-person businesses. Offers simplicity but no liability protection.

- Incorporation: Offers liability protection and potential tax advantages. It may involve more paperwork and ongoing compliance, but adds credibility and separates personal from business assets.

Tip: Check your province’s business registration page for detailed guidance on how to register and what’s required for each structure.

Costs, Profitability & Scaling Tips

Starting a business from home is often one of the most cost-effective ways to launch, particularly if you’re offering a digital or service-based solution. Many entrepreneurs can get started with relatively little investment, focusing instead on skills, time, and smart planning.

What to Expect

Startup Costs:

Home-based businesses typically require fewer resources than traditional brick-and-mortar ventures. Online services often have the lowest overhead, while creative or hands-on businesses may involve additional costs such as equipment, supplies, or regulatory compliance.

Time to Profit:

While some home-based businesses may start generating revenue early on, most small businesses take 2 to 3 years to become truly profitable. Long-term success often builds over time, with many businesses hitting their stride after 7 to 10 years. This timeline underscores the importance of patience and persistence in the early stages.

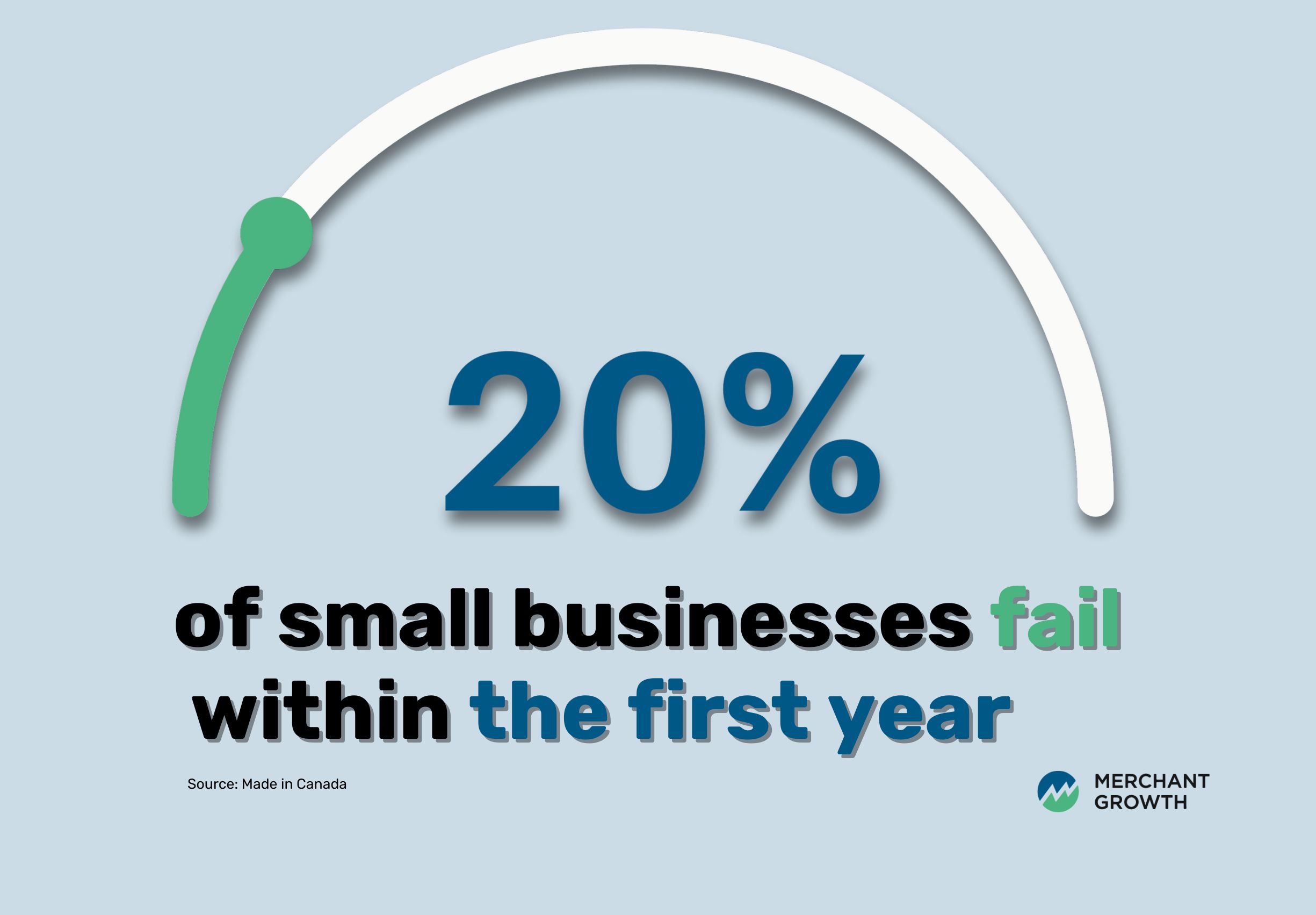

Risk Factors:

It’s important to be aware that around 20% of small businesses fail within their first year. Choosing a business model that aligns with your skills and lifestyle—and starting with a clear plan—can help you avoid common pitfalls.

Scaling Tips

- Reinvest early revenue into tools, automation, or marketing efforts to increase efficiency.

- Consider outsourcing or bringing in support (like a virtual assistant) as demand grows.

- Focus on customer feedback to evolve your offerings and stay competitive.

Some businesses—such as bookkeeping, freelance writing, or virtual assistance—can scale quickly with relatively low costs. Others, like product-based ventures or daycare services, may take longer to grow but can offer reliable, long-term returns once established.

Marketing Your Home-Based Business

Even with the best service or product, you’ll need a solid marketing plan to attract customers. Fortunately, there are several low-cost strategies that work well for home businesses.

Social Media Marketing

Use platforms like Instagram, Facebook, LinkedIn, and TikTok to promote your business visually, build trust, and connect with your audience. Tools like Canva or Later can help you design and schedule posts.

Local SEO (Search Engine Optimization)

Register your business with Google Business Profile to appear in local search results. Include keywords like “home-based bookkeeping in Toronto” or “custom candles in Vancouver” on your website to boost search visibility.

Community Boards & Groups

- Post on Facebook Marketplace and local buy/sell groups.

- Put up flyers in coffee shops or libraries.

- Join local entrepreneur groups or business associations.

Virtual Networking

Attend webinars, join Slack or Discord communities, and build referral partnerships with other small businesses.

Helpful Marketing Tools

No matter what kind of home-based business you run, smart marketing can make all the difference. Thankfully, you don’t need a big budget to promote your services effectively. There are plenty of free or low-cost tools available that can help you manage everything from design and email marketing to task planning and invoicing. Here are some of the most popular options to get you started:

- Canva – For creating marketing graphics.

- Mailchimp – For email campaigns.

- Google Business Profile – For local search visibility.

- Wave – For invoicing and financial tracking.

- Trello/Notion – For business planning and task management.

Resources & Support for Canadian Entrepreneurs

You don’t have to build your home business alone. Across Canada, entrepreneurs can tap into an impressive range of free and subsidized support programs—from funding to mentorship.

Government of Canada (Canada.ca)

The federal government offers a central hub of resources to help Canadians plan, register, and grow their businesses. Whether you're searching for funding or just figuring out where to begin, Canada.ca is a great place to start.

- Business Benefits Finder

- Guides for business registration, taxes, and structure

- Federal funding and grants directory

Business Development Bank of Canada (BDC)

BDC is Canada’s only bank devoted exclusively to entrepreneurs. From financing to expert advice, it offers tools designed to help home-based and small business owners thrive at every stage of growth.

- Offers financing and small business loans

- Free business planning tools and calculators

- Online courses and advisory services

➡️ Explore BDC’s small business tools

Small Business Centres (By Province)

Across Canada, provincial and municipal governments run small business centres that offer free services tailored to local entrepreneurs. These centres provide everything from licensing support to one-on-one mentorship.

- Ontario’s Small Business Enterprise Centres (SBECs) offer free mentorship, workshops, and help with licensing.

- Similar services are available in provinces like B.C., Alberta, and Nova Scotia.

FedDev Ontario & Other Regional Development Agencies

Regional development agencies are focused on boosting local economies by supporting small business innovation and expansion. Whether you're in Ontario, the Prairies, or the North, there's likely a regional agency ready to help you grow.

- FedDev Ontario provides grants and regional economic development support.

- Regional agencies across Canada (e.g., PrairiesCan, ACOA, CanNor) provide funding and business growth services.

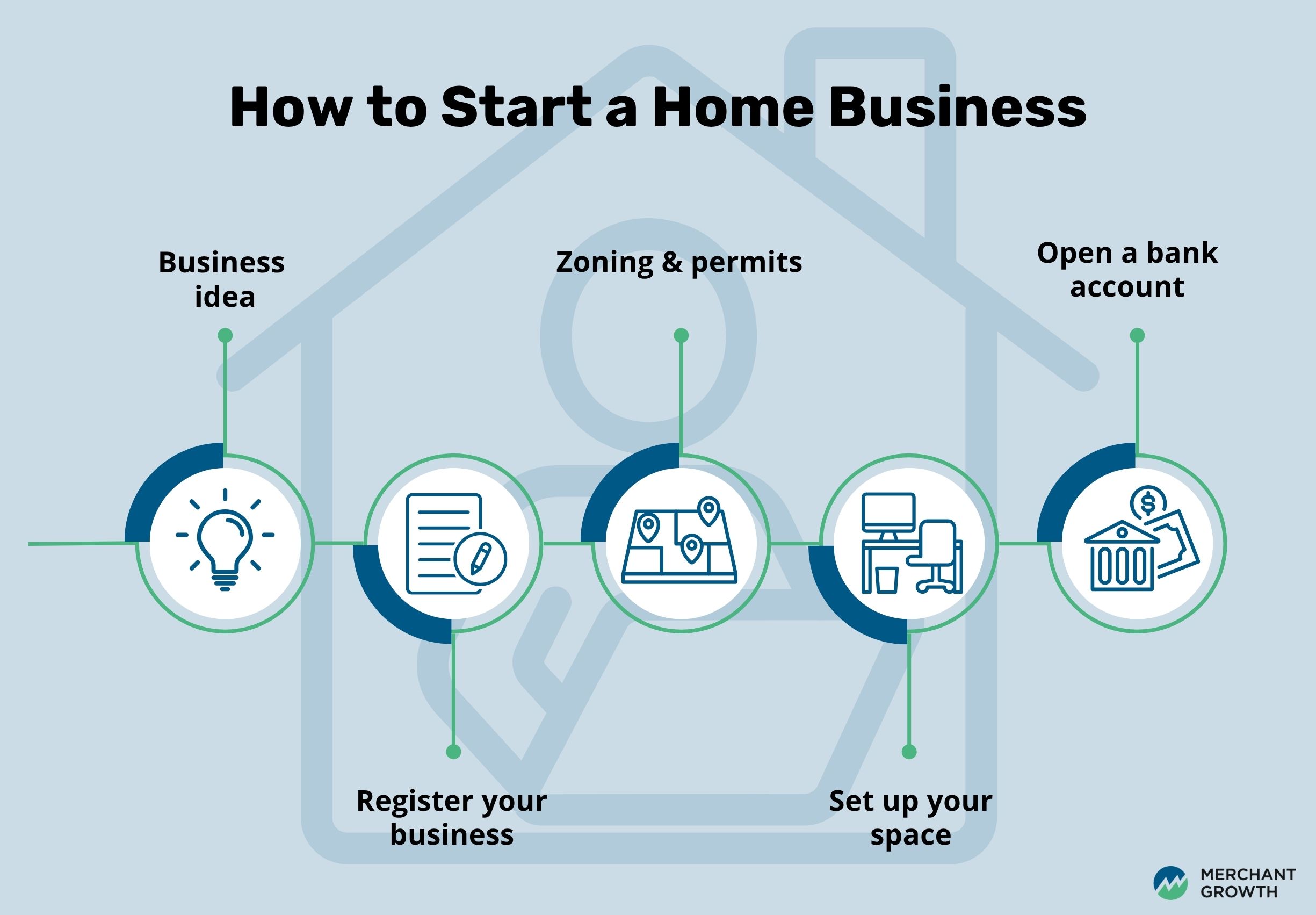

How to Start a Home-Based Business in Canada

Starting small is smart, but getting the foundations right is key. Here's how to go from idea to launch.

1. Choose a Business Idea That Fits Your Lifestyle & Skills

Select something you enjoy and are skilled at. Consider your available time, home space, and startup budget. Start part-time if you're unsure, and validate demand before investing heavily.

2. Register Your Business

Each province has its own registration portal. You'll need to check name availability, decide on a legal structure, and file any required documents.

3. Check Local Zoning & Permit Requirements

Some municipalities limit certain business types (like daycare or food sales) from being run at home. You may need a “home occupation” permit or specific zoning approval.

4. Set Up Your Business Space

Designate a specific area of your home for your business. Whether it’s a home office, kitchen, or garage workshop, make sure it’s safe, productive, and aligned with legal requirements (especially for childcare or food services).

5. Open a Business Bank Account & Track Finances

Separate your business finances from personal funds from day one. Use simple accounting software (like Wave, FreshBooks, or QuickBooks) to stay organized and ready for tax time.

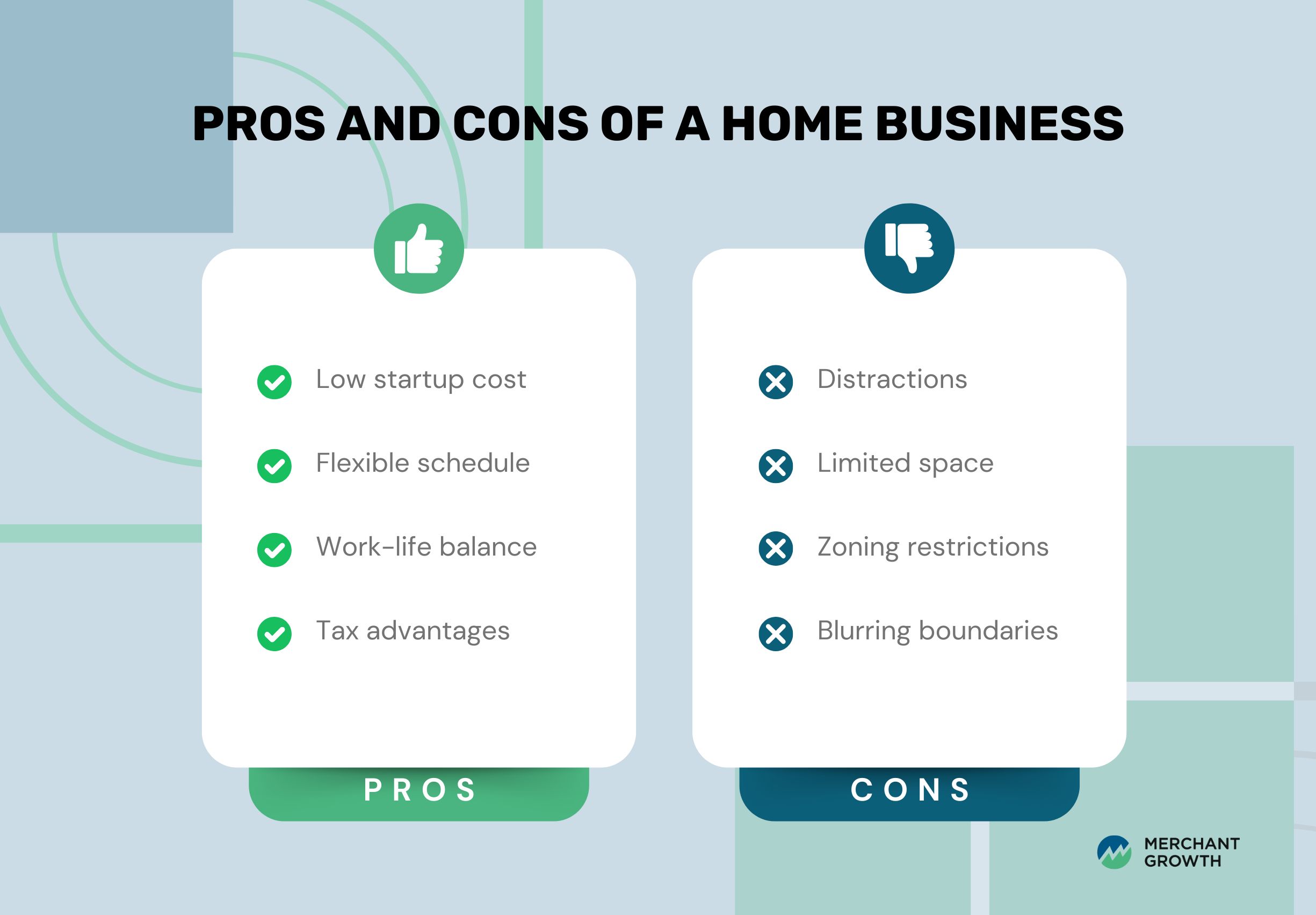

Pros and Cons of Starting a Home-Based Business

Running a business from home can offer significant rewards, but it also comes with its own set of challenges. Whether you're considering the move or are already in the planning stages, it’s important to weigh both sides to determine if a home-based model fits your goals, lifestyle, and work environment.

| Pros | Cons |

|---|---|

| Low Startup Costs: Avoid expensive leases and overhead. | Distractions: Family or roommates can disrupt focus. |

| Flexible Schedule: Work around family, caregiving, or other responsibilities. | Limited Space: Physical storage and work areas may be constrained. |

| Work-Life Balance: No commute and more control over your environment. | Zoning Restrictions: Certain business types may not be allowed. |

| Tax Advantages: Home office deductions, business expenses, and equipment write-offs. | Blurring Boundaries: It’s easy to let work spill into personal time. |

From Home to Growth: How Financing Can Support Your Next Step

While many home-based businesses are intentionally lean at the start, growth often brings new opportunities—and new expenses. Expanding your operations, investing in better equipment, or even hiring support can require more cash than your business has on hand. That’s where strategic financing comes in.

Why Financing Matters for Home Businesses

Even the most profitable home-based businesses encounter moments when access to capital is crucial:

- Unexpected expenses can stall progress and delay growth plans.

- Equipment upgrades or staffing often require an upfront investment.

- Seasonal income fluctuations can make it difficult to manage cash flow year-round.

Working capital gives you the flexibility to take on opportunities without sacrificing stability or dipping into personal savings.

How Merchant Growth Can Help

Merchant Growth specializes in small business financing that’s built to scale with your needs. Whether you’re looking to smooth over seasonal dips or fund a big next step, we offer options that align with your goals:

- Term Financing: Ideal for one-time investments like purchasing equipment or launching a new product.

- Lines of Credit: A flexible way to manage cash flow, cover payroll, or invest in marketing.

Once your business generates consistent revenue, our financing solutions can help you grow confidently, on your terms.

Ready to grow your business from home and beyond? Explore our small business financing options.

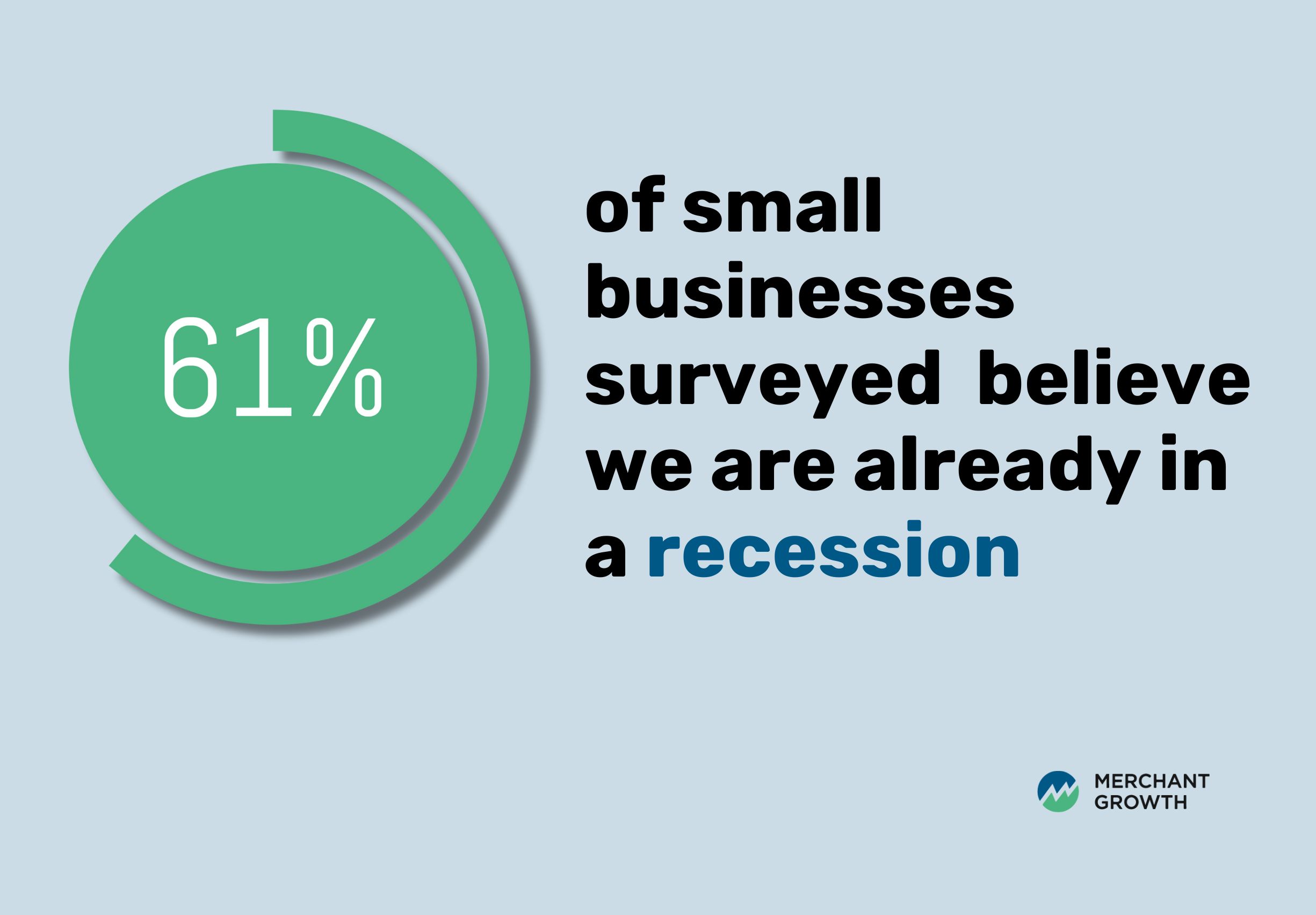

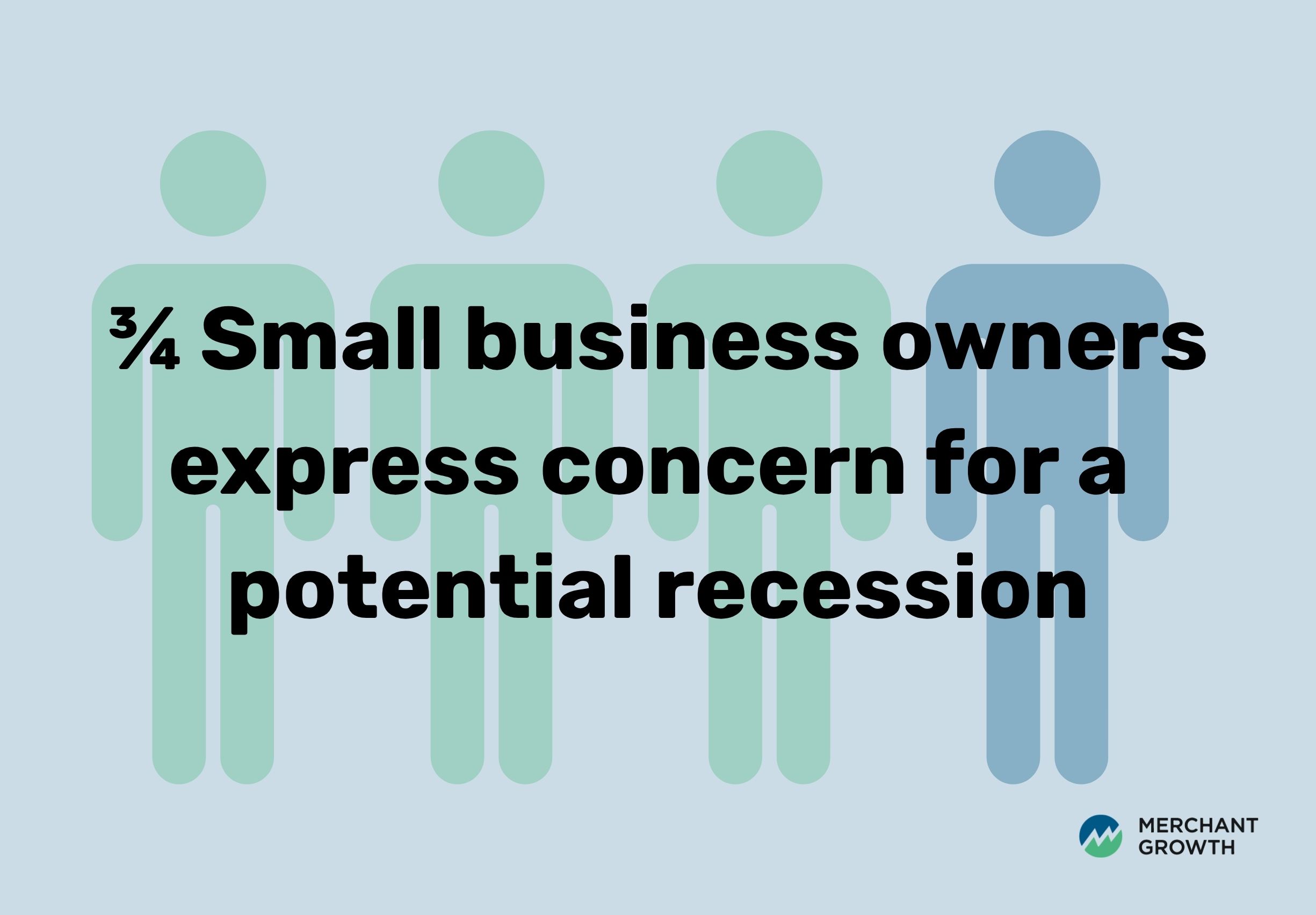

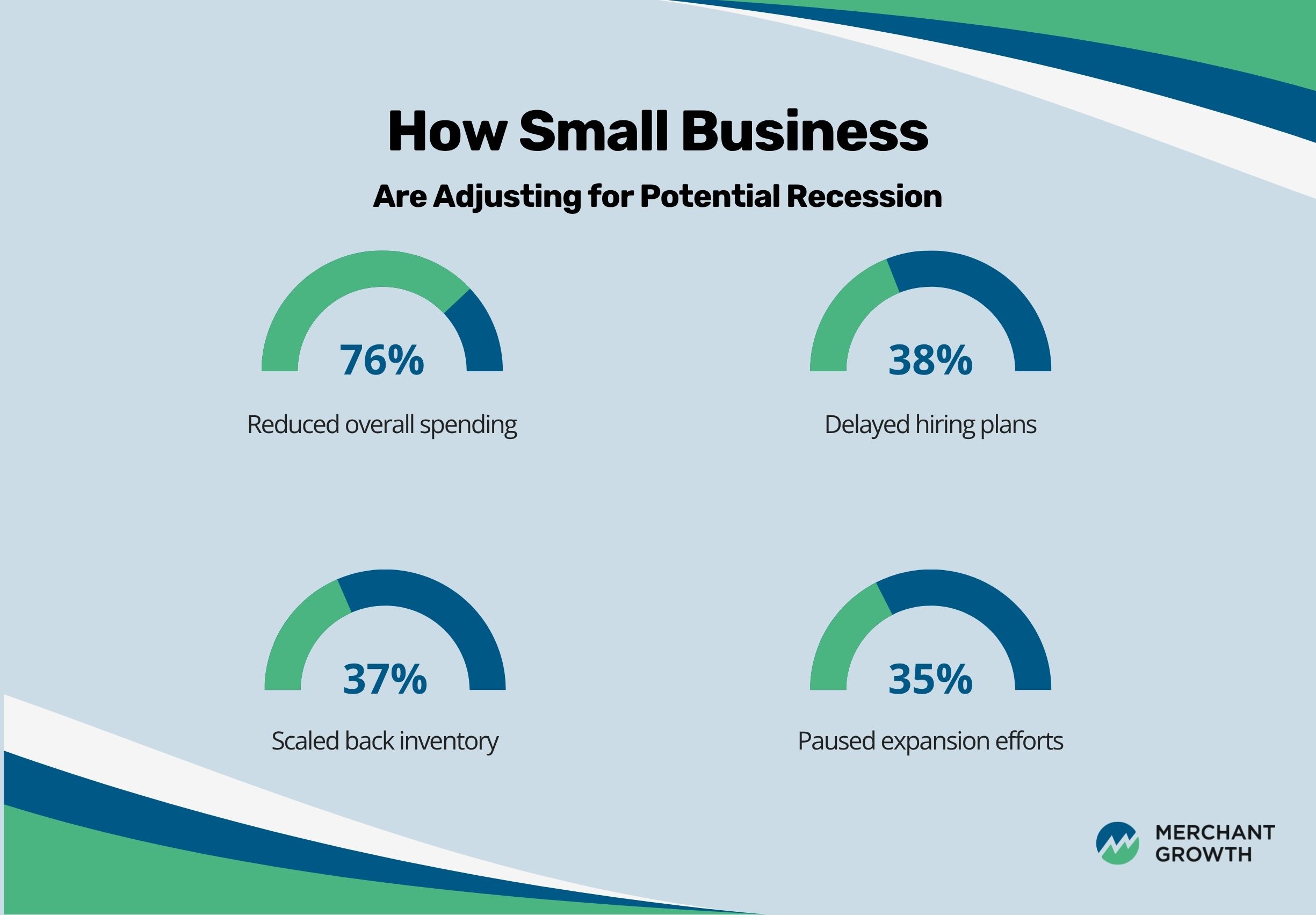

Is Your Business Failing? How to Recognize the Signs, Rebuild with Confidence, and Access Support in Canada

Running a small business comes with ups and downs, and if you're feeling like the challenges are starting to outweigh the wins, you're not alone. Many business owners experience periods of financial stress, declining momentum, or even full-blown burnout. The important thing is recognizing the warning signs early and knowing that there are proven strategies and support systems available to help you recover.

According to Made in Canada, about 20% of small businesses don't survive their first year. But that means approximately 80% do—and with the right tools and support, many struggling businesses can be turned around.

In this article, we’ll walk you through how to spot trouble early, figure out your next steps, and tap into the resources that can help your business get back on track.

Key Takeaways

- Business failure can stem from cash flow issues, poor planning, shifting markets, or burnout, but these challenges can be addressed with the right strategies.

- Recognizing early warning signs like declining revenue, customer loss, or staff turnover is critical.

- Canadian small businesses have access to support, from government programs (BDC, Futurpreneur, etc.) to advisory services and financing solutions.

- Not every business can be saved, but many can be stabilized, pivoted, or reborn with the right approach.

Early Warning Signs of a Failing Business

Spotting trouble early can mean the difference between a successful recovery and having to shut your doors for good. In fact, only about 7% of businesses cite a 'failure to make necessary changes' as the primary cause for closure, highlighting just how powerful it can be to adapt when warning signs appear. Here are some red flags that should prompt a closer look:

- Declining revenue or shrinking profit margins

- Cash flow crunches and unpaid bills

- Mounting debt or rejections from lenders

- Loss of regular customers or increased churn

- High staff turnover or low team morale

- New competitors or changing market demand

- Missed deadlines, disorganized operations, or unclear roles

If several of these signs feel familiar, take it as your cue to act, not out of panic, but out of possibility. Identifying issues early gives you the best chance to course-correct, stabilize, and build a stronger, more resilient business.

Common Reasons Small Businesses Fail

Understanding why small businesses fail isn’t about placing blame—it’s about empowering yourself with the knowledge to avoid the same missteps. Many entrepreneurs pour their hearts, time, and savings into their ventures, only to be blindsided by avoidable pitfalls. Whether it’s a lack of planning, poor cash flow management, or not adapting to market changes, the root causes of failure often follow predictable patterns. By getting clear on what commonly derails small businesses, you can make smarter, more informed decisions to protect your own. Below, we break down the key challenges Canadian entrepreneurs face—and how to navigate them.

Poor Planning or Lack of a Business Model

Without a clear plan or strategy, it's easy to drift. Whether it's skipping market research, overestimating demand, or failing to forecast expenses, weak business planning puts you at a disadvantage from day one.

Tip: Create a simple business plan—even a one-page version—that outlines your goals, target market, revenue model, and key expenses. Tools like the BDC’s free business plan template can make this process easier and more focused.

Inadequate Marketing

If you're not reaching the right audience or clearly showing what makes your business different, it's hard to stand out, let alone grow. According to the CFIB, 42% of small businesses fail because they haven’t properly researched the market. That means many entrepreneurs launch without fully understanding who their customers are, where to find them, or what messages resonate.

Tip: To avoid falling into this trap, take time to define your target audience, study their behaviours, and test different marketing channels. Even a small, consistent marketing strategy can go a long way in building awareness and attracting loyal customers.

Over-Reliance on One Revenue Stream

Many businesses fail because a single client or product line dries up. Diversification is essential to long-term resilience. When too much depends on one revenue source, any disruption—like a client leaving or a product becoming obsolete—can quickly spiral into a crisis.

Tip: Explore complementary revenue streams such as new product offerings, subscription models, or targeting different customer segments. Even a modest second stream can provide helpful stability.

Weak Cash Flow Management

A lack of financial visibility is one of the top reasons small businesses fail. Late payments, poor pricing strategies, or over-investment can quickly drain your resources and leave you scrambling to cover expenses. In fact, 22% of small business owners expect to face challenges maintaining their cash flow, highlighting just how common and critical this issue is.

Tip: Use cash flow forecasting tools or work with a bookkeeper to project future cash flow needs. Review pricing regularly to ensure you're covering costs and building in a margin for growth.

Business Owner Burnout

Business owners often wear every hat, and it catches up fast. Chronic stress, decision fatigue, and isolation can lead to poor choices or a complete loss of motivation.

Tip: Build rest and support into your business plan. Set realistic work hours, take regular breaks, and seek out mentors, peer networks, or even part-time help to reduce isolation and overload.

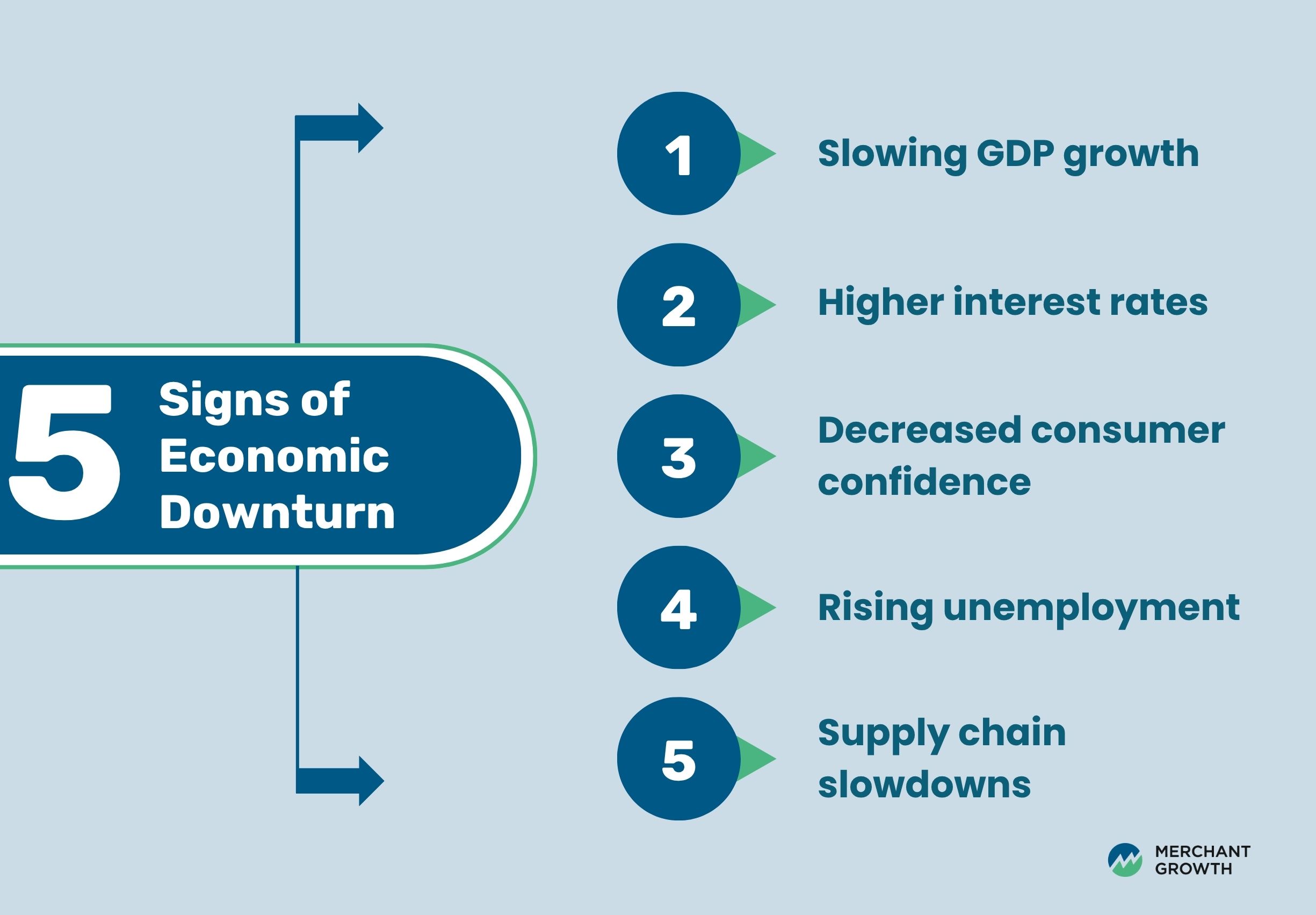

External Pressures

Economic downturns, supply chain disruptions, and regulatory changes can throw even successful businesses off course. These are often out of your control, but how you respond makes all the difference.

Tip: Stay agile by regularly reviewing industry trends, maintaining strong supplier relationships, and having contingency plans in place for major disruptions.

Assessing Your Business’s Financial Health

When a business starts to struggle, it’s easy to focus on surface-level symptoms—missed deadlines, mounting stress, or slow sales. But the root cause often lies in the numbers. Understanding your financial health is one of the most important steps in regaining control and avoiding deeper trouble. Consider it a financial health check—looking closely at your cash flow, revenue, and obligations to understand where your business truly stands.

Here are key areas to examine:

- Cash Flow Statement: Are your incoming funds consistently covering your expenses? If not, your business may be at risk of running into operational trouble. Download our free Cash Flow Statement Template to help you get a clearer picture ➡️ Download Here

- Profit & Loss Trends: Are you profitable month to month? Is your growth flat, steady, or slipping?

- Debt & Loan Obligations: Are repayments manageable, or are they adding strain?

- Payroll & Vendor Payments: Are you paying people (or yourself) on time, or constantly behind?

- Client Base: Are customers sticking around, or are you always trying to replace lost business?

These indicators can reveal not just how your business is doing—but where to focus your efforts first. Even small improvements in one area can create a ripple effect. Don’t be discouraged by what you find. This isn’t about perfection; it’s about clarity, direction, and taking control.

What Does “Going Concern” Mean in Business?

You may have heard the term “going concern” in business conversations, but what does it actually mean? In simple terms, it’s the assumption that your business will continue to operate and generate income in the foreseeable future, typically at least the next 12 months.

But when that assumption is at risk—due to sustained losses, cash flow problems, or mounting debt—your business may no longer be considered a going concern. This status has serious implications and is often a red flag to lenders, investors, and even employees.

Signs your business may no longer be a going concern:

- You're unable to pay your bills or meet payroll consistently

- Your debt is growing faster than your revenue

- You’ve lost access to financing or are being turned down for credit

- Auditors raise concerns about your financial statements

- You’re relying heavily on personal savings or short-term fixes to stay afloat

Why it matters:

- It affects how you report your finances, potentially requiring disclosure of material uncertainty in your statements

- It can impact your ability to raise funds or renew lines of credit

- It signals to stakeholders (employees, partners, banks) that significant changes may be needed

Recognizing and addressing these risks early gives you a better chance to stabilize and rebuild before the situation becomes irreversible.

Revisit Your Business Model and Strategy

When your business hits a plateau—or worse, begins to decline—it’s often not just about cash flow or marketing. The root issue may lie in the foundation: your business model. What once worked to attract and retain customers may no longer meet market needs, especially in fast-changing industries or economic conditions.

Taking a step back to assess your overall strategy can give you the clarity needed to make smart, intentional changes. Think of it less as starting over and more as a recalibration.

Here are some questions to guide your evaluation:

- Does your product or service still solve a real problem?

- Are there new audiences you could reach?

- Can you adjust pricing or add new revenue streams?

- Are your operations bloated or outdated?

Small, strategic changes—like bundling your services, refining your niche, or experimenting with new sales channels—can breathe new life into a tired business model. The key is to stay curious, test ideas, and be willing to pivot. A fresh perspective might reveal untapped opportunities hiding in plain sight.

Canadian Support Programs That Can Help

You are not alone. Whether you're experiencing a slow season, rethinking your strategy, or trying to turn your business around, there are many support systems across Canada designed to help small business owners like you.

From mentorship and financial guidance to grants and digital adoption programs, these resources can offer the tools, insight, and encouragement you need to move forward with confidence. Tapping into the right support at the right time can make all the difference.

Here’s a snapshot of national and regional programs worth exploring:

| Resource | What It Offers |

|---|---|

| BDC (Business Development Bank of Canada) | Advisory services, small business loans, planning tools, and financial calculators. |

| Futurpreneur Canada | Financing and mentorship for entrepreneurs aged 18–39, including business plan support. |

| Canada Digital Adoption Program (CDAP) | Grants and expert advisors to help small businesses modernize their digital operations. |

| Provincial Programs | Most provinces offer their own funding, training, or low-interest loan programs through economic development offices or business hubs. |

| Local Chambers of Commerce | Access to networking events, training sessions, and local business advisors or consultants. |

If you're unsure where to start, consider speaking with a local mentor, accountant, or business coach. These professionals can help you map out a recovery plan and connect you with the programs that fit your goals and challenges best. Sometimes, just having a sounding board can reframe a tough situation—and remind you that better days are ahead.

How to Deal with Burnout as a Business Owner

Burnout isn’t just being tired—it’s a state of chronic physical, mental, and emotional exhaustion that can make even basic business decisions feel overwhelming. And it’s more common than most entrepreneurs admit.

In fact, two-thirds of small business owners reported feeling close to burnout in 2022, and over half said they were actively struggling with their mental health. With so many hats to wear and never enough hours in the day, it’s no surprise. A healthy work-life balance is not just a nice-to-have—58% of Canadian small business owners say it’s crucial to long-term success.

Recognizing what’s causing your burnout is the first step toward managing it. Here's a breakdown of common triggers and how to address them:

| Cause | Strategy to Manage It |

|---|---|

| Overworking with no breaks | Set clear work hours and stick to them. Use scheduling tools to create structured time off—even just an hour or two daily. |

| Constant financial pressure | Work with a financial advisor to build a realistic budget or seek out flexible financing options to ease short-term stress. |

| Isolation from peers or mentors | Join a local small business network, peer mastermind group, or online community to share experiences and gain support. |

| Decision overload | Delegate low-impact decisions where possible. Use checklists, SOPs, or hire a virtual assistant to streamline daily choices. |

| Disconnect from business purpose | Revisit why you started. Reflect on wins, review client testimonials, or set fresh short-term goals to reignite motivation. |

No business thrives when the person running it is burned out. Seeking support—whether through mentorship, therapy, or a trusted network—can make the journey more manageable. Don’t wait until you're running on empty. Just like your business, your well-being needs ongoing investment.

Resources:

For mental health and burnout prevention, explore the Government of Canada’s guide to preventing burnout and BDC’s entrepreneur well-being resources for practical tools and support.

Should You Pivot, Downsize, or Close?

It’s a tough truth: not every business survives in its original form. But choosing to pivot, scale down, or close isn’t a failure—it’s a smart, strategic decision that many successful entrepreneurs have made. Sometimes letting go of what’s not working is the bravest and most empowering move you can make.

If you’ve been losing money month after month, feeling constant anxiety, or noticing that your business is harming your health, relationships, or overall quality of life—it may be time to re-evaluate. You’re not alone. Thousands of small business owners each year go through this process, and many come out stronger on the other side.

Here are some options to consider, and when they might make sense:

| Option | When to Consider It |

|---|---|

| Pivot to a more viable offering | You’ve identified a product, service, or market with stronger demand or profitability, and still feel committed to entrepreneurship. |

| Downsize to reduce costs | Overhead is too high, but you believe in the business. Shrinking operations could give you time to regroup. |

| Merge with a complementary business | You’ve found a business with strengths that complement yours—joining forces could spark new growth. |

| Sell your assets | You’re ready to step away, but have valuable assets. Selling helps recover investment and move on cleanly. |

| Close your business legally and cleanly | You’ve tried other paths, but it’s time to move on. Formal closure frees you from future obligations. |

If you're considering a major change—whether that's pivoting, downsizing, or exiting entirely—what matters most is making a thoughtful, informed decision. Reflect on your goals, weigh the trade-offs, and seek guidance if needed. Clarity, not pressure, should drive your next move. Your future success doesn’t depend on holding on—it depends on choosing what’s right for you now.