Getting Started with Budgeting for Your Small Business Finances

Most Canadian small business owners don’t struggle because they aren’t making money, they struggle because it’s hard to see how that money is actually working in the business. You might be covering expenses, bringing in sales, and staying busy, but still feel unsure about what you can afford to spend, save, or reinvest. Without a clear plan in place, even healthy businesses can feel financially unpredictable.

That’s where budgeting comes in. A budget isn’t just a financial document you create once and forget about; it’s a practical tool that helps you understand your business, make better decisions, and stay in control of your cash flow.

Whether you’re building your first budget or revisiting your approach, the goal isn’t perfection, it’s clarity. You won’t have every number exactly right from the start, but taking the time to map things out will give you a stronger understanding of how your business actually operates.

Key Takeaways

- A budget is a simple plan that tracks your income and expenses

- It helps you understand and manage your cash flow

- Every budget is built from revenue, fixed costs, and variable expenses

- Budgets should be reviewed and adjusted regularly

- Budgeting supports both day-to-day stability and future growth

What Is a Budget for a Small Business?

At its core, a small business budget is a plan that outlines how your business will earn and spend money over a set period of time. It brings together your expected revenue, your costs, and what remains, giving you a clear view of your financial position.

A typical budget is built from a few key components. This includes your projected income, fixed costs like rent and payroll, and variable expenses such as inventory, marketing, or utilities. It may also account for one-time expenses and the timing of when money comes in and goes out.

You can think of it as a working snapshot of your business finances. For example, if you expect to bring in $20,000 in a month and your total expenses are $18,000, your budget shows the margin you’re working with. It also highlights how those numbers are structured, helping you see where your money is being allocated.

Why Budgeting Matters (Even If You’re Just Getting Started)

When you’re running a small business, timing matters just as much as profitability. You might be making sales, but if payments are delayed or expenses hit all at once, it can still feel like you’re constantly playing catch-up. Budgeting helps bring structure to that uncertainty.

A well-built budget allows you to anticipate upcoming expenses, plan for slower periods, and make decisions with more confidence. It also reduces the stress that comes from not knowing whether you can afford to hire, invest in marketing, or take on new opportunities.

Even if your business is still in its early stages, budgeting gives you a foundation to build on. It doesn’t require perfect data, it just requires a willingness to track, estimate, and adjust as you go.

What Goes Into a Small Business Budget

Every small business budget is built from a few core components. Once you understand how each of these works, budgeting becomes much more practical and far less overwhelming. Instead of guessing where your money is going, you can start to see how each piece fits together.

Revenue

Revenue is the money your business expects to bring in over a given period, and it’s the starting point for your entire budget. This can include one-time sales, ongoing service contracts, or recurring income streams like subscriptions or retainers.

When estimating revenue, it’s important to stay grounded in reality. If your sales fluctuate month to month, look at historical averages or identify patterns such as seasonality or slower periods. Overestimating revenue is one of the most common budgeting mistakes, and it can lead to spending decisions that aren’t sustainable. A conservative estimate gives you a more stable foundation to work from and helps prevent shortfalls later on.

Fixed Costs

Fixed costs are the expenses that remain relatively consistent each month, regardless of how your business is performing. These typically include rent, salaries, insurance, software subscriptions, and loan payments.

Because fixed costs don’t change often, they form the baseline of your budget. Understanding these expenses clearly allows you to determine the minimum amount of revenue your business needs to generate just to operate. This is especially important for newer businesses, as it helps define your financial “starting point” before accounting for growth or additional spending.

Variable Costs

Variable costs fluctuate based on your level of business activity. These can include inventory, shipping, utilities, payment processing fees, or marketing spend.

Unlike fixed costs, these expenses can increase as your business grows, which makes them important to track closely. For example, higher sales may lead to higher inventory costs or increased transaction fees. While that growth is positive, it still needs to be accounted for in your budget to maintain healthy margins. Keeping a close eye on variable costs helps you understand how efficiently your business is operating as it scales.

One-Time Expenses

One-time expenses are costs that don’t occur regularly but can still have a significant impact on your finances. This might include purchasing new equipment, redesigning your website, investing in a rebrand, or running a large marketing campaign.

Because these expenses are less predictable, they’re often overlooked in early budgets. However, failing to plan for them can disrupt your cash flow when they arise. Setting aside a portion of your budget for occasional or unexpected costs can help you stay prepared without putting pressure on your day-to-day operations.

Cash Flow Timing

Cash flow isn’t just about how much money your business makes, it’s about when that money actually arrives. Even profitable businesses can run into challenges if there’s a delay between earning revenue and receiving payment.

For example, if you invoice clients on net terms, you may need to cover expenses weeks before payment is received. A strong budget accounts for these timing differences, helping you plan ahead and avoid gaps where cash might be tight. Understanding your cash flow timing allows you to make more informed decisions about spending, saving, and reinvesting in your business.

When you bring all of these components together, your budget becomes more than just a list of numbers. It becomes a clear, structured view of how your business operates financially. Once you have that visibility, the next step is understanding how to use it, because knowing your numbers is only valuable if it helps you make better day-to-day decisions.

How to Create Your First Small Business Budget

Creating your first budget doesn’t need to be complicated. The goal is to build a clear, workable starting point that reflects how your business operates today, not a perfect projection of where you hope it will be. Once you have that foundation in place, you can refine and improve it over time as you gather more data and experience.

![Infographic of how to create your first small business budget]](https://www.merchantgrowth.com/wp-content/uploads/2025/04/How-to-Create-a-Small-Business-Budget-Infographic.jpg)

1. Estimate Your Income

Start by reviewing past sales if you have them, or by making realistic projections if you’re just getting started. Look for patterns in your revenue, such as seasonal trends, busy periods, or slower months, to guide your estimates.

If your income varies, it’s better to take a conservative approach rather than assuming your highest-performing months will continue. This gives you more room to manage expenses without putting pressure on your cash flow. Over time, as you track actual performance, your revenue estimates will become more accurate and reliable.

2. List Your Fixed Costs

Next, outline all of your recurring expenses that stay relatively consistent each month. These may include rent, payroll, insurance, subscriptions, loan payments, and any other essential costs required to keep your business running.

Because these expenses are predictable, they provide a clear baseline for your budget. Knowing exactly what you need to cover each month helps you understand the minimum revenue required to operate your business sustainably. This step is often the most straightforward, but it’s also one of the most important.

3. Track Variable Expenses

Variable expenses require a bit more attention because they can change depending on your level of business activity. This might include inventory purchases, shipping costs, utilities, marketing spend, or transaction fees.

Review past transactions where possible, or make informed estimates based on how your business operates. It’s generally safer to slightly overestimate these costs, especially in the early stages, to avoid under-budgeting. As you track these expenses over time, you’ll gain a clearer understanding of how they fluctuate and how they impact your margins.

4. Plan for One-Time or Unexpected Costs

Not every expense shows up on a monthly basis. Equipment upgrades, website improvements, or one-time marketing initiatives can all create sudden financial pressure if they aren’t accounted for in advance.

Setting aside even a small portion of your budget for these types of expenses can make a meaningful difference. It allows you to handle opportunities or unexpected costs without disrupting your day-to-day operations or relying on last-minute solutions.

5. Map Out Your Cash Flow

Once you’ve outlined your income and expenses, the next step is to look at timing. When does money come in, and when does it go out? This is where many businesses run into challenges, especially if payments are delayed or expenses are due up front.

Mapping out your cash flow helps you identify periods where cash might be tight and plan accordingly. It also gives you a better sense of how much flexibility you have when making decisions about spending or investing in your business.

6. Review and Adjust Regularly

A budget is not something you set once and leave untouched. As your business changes, your numbers will change with it. That’s why regular reviews are essential to keeping your budget accurate and useful.

Set a schedule—monthly or quarterly—to compare your projections against actual results. Look for gaps, trends, or areas where adjustments are needed. Over time, this process helps you build a budget that reflects your business more accurately and supports better decision-making.

By following these steps, you’re not just creating a budget—you’re building a system that helps you understand and manage your finances more effectively. And once that system is in place, the next step is learning how to make it work for you in practice, from choosing the right approach to avoiding common pitfalls.

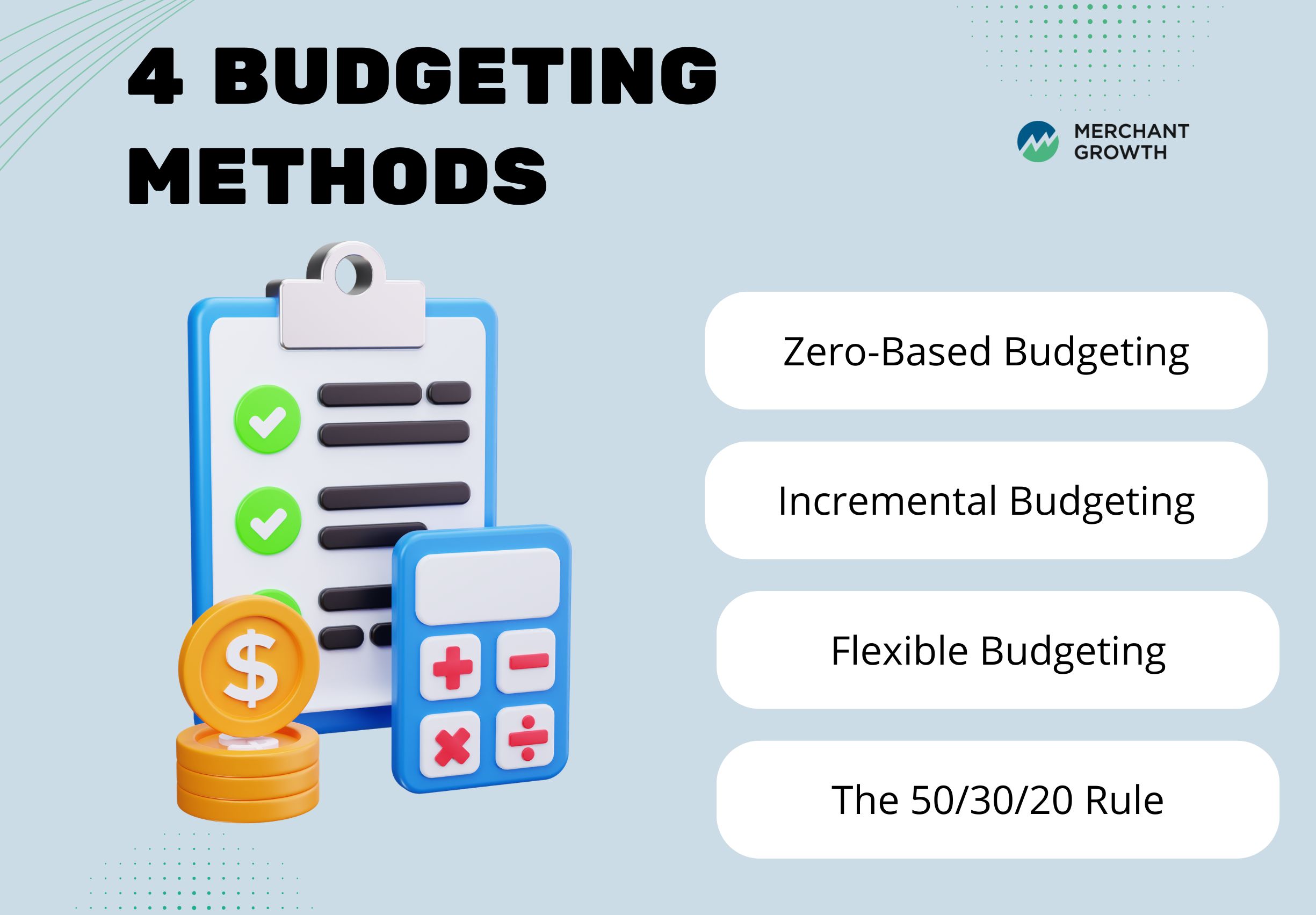

Budgeting Methods (Made Simple)

There’s no single “right” way to build a budget. The best approach depends on how your business operates, how predictable your revenue is, and how much time you want to spend managing your finances. What matters most is choosing a method that’s practical, easy to maintain, and flexible enough to grow with your business.

Zero-Based Budgeting

Zero-based budgeting starts from scratch each period, meaning every expense must be reviewed and justified before it’s included. Instead of relying on past budgets, you build your plan based on current priorities and needs.

This method is especially useful if you’re trying to gain tighter control over spending or identify areas where costs can be reduced. It forces you to evaluate each expense more critically, which can help eliminate inefficiencies. However, it can be more time-intensive, making it better suited for business owners who want a hands-on approach or are going through a period of change.

Incremental Budgeting

Incremental budgeting takes your previous budget as a starting point and adjusts it based on expected changes, such as growth, inflation, or new expenses. This is one of the most common approaches because it’s simple and relatively quick to implement.

For businesses with stable operations and predictable costs, incremental budgeting provides a practical way to plan without rebuilding everything from the ground up. However, it’s important to review your existing expenses carefully, as this method can sometimes carry forward unnecessary costs if they aren’t reassessed regularly.

Flexible Budgeting

Flexible budgeting is designed to adapt as your revenue changes. Instead of setting fixed spending limits, this approach allows certain expenses to scale up or down depending on how your business is performing.

This method works well for businesses with seasonal sales, fluctuating demand, or variable income streams. For example, if revenue increases, you might increase your marketing spend or inventory accordingly. Flexible budgeting helps you stay responsive and avoid overcommitting during slower periods, making it a strong option for businesses that need agility.

The 50/30/20 Rule

Although it’s commonly used in personal finance, the 50/30/20 rule can be adapted as a simple framework for small business budgeting. It divides your budget into three categories: essential expenses, growth-related spending, and savings or debt repayment.

For example, you might allocate around 50% of your budget to core operating costs, 30% to growth initiatives like marketing or product development, and 20% toward building reserves or paying down debt. While the exact percentages may vary depending on your business, this structure can help you maintain balance and avoid overextending in any one area.

Choosing a budgeting method gives you structure, but it’s how you apply it day to day that makes the biggest difference. Small habits, consistent tracking, and realistic assumptions are what turn a plan into something you can actually rely on.

Practical Budgeting Tips for Small Business Owners

Budgeting works best when it’s supported by consistent habits and realistic expectations. Small adjustments in how you manage your finances can make a significant difference over time, especially when they’re applied consistently.

Here are a few practical ways to make your budget more effective:

Keep your business and personal finances separate

Mixing personal and business expenses makes it much harder to track where your money is going. Keeping them separate gives you a clearer, more accurate view of your business performance and simplifies everything from budgeting to tax preparation.

Set aside money for taxes early

Taxes are one of the most commonly overlooked expenses in small business budgeting. Setting aside a portion of your revenue as you earn it helps you avoid large, unexpected payments and reduces financial stress later on.

Build a contingency buffer

Unexpected costs are part of running a business, whether it’s equipment repairs, supplier changes, or slower sales periods. Even a small reserve built into your budget can help you handle these situations without disrupting your operations.

Be conservative with your revenue estimates

It’s easy to assume your best months will continue, but that can lead to overspending. Using more conservative estimates helps create a buffer and keeps your budget realistic and sustainable.

Use tools that match your workflow

Whether it’s a simple spreadsheet or accounting software, the best system is one you’ll actually use. Consistency matters more than complexity when it comes to managing your budget effectively.

These habits may seem simple, but they create a strong foundation for managing your budget more effectively. Once these are in place, it becomes easier to spot where things can go wrong, and how to avoid common budgeting mistakes.

Common Budgeting Mistakes to Avoid

Even with the best intentions, small budgeting mistakes can create bigger financial challenges over time. Being aware of these common pitfalls can help you build a budget that’s more accurate, flexible, and reliable.

Here are a few mistakes to watch out for:

Overestimating your revenue

It’s easy to assume your business will continue performing at its peak, but relying on overly optimistic projections can lead to spending decisions that aren’t sustainable. A more conservative approach gives you room to adapt if sales fluctuate.

Underestimating variable costs

Variable expenses like inventory, shipping, and marketing can change quickly as your business grows. If these costs aren’t tracked carefully, they can quietly reduce your margins and impact your overall financial stability.

Ignoring small or irregular expenses

One-time purchases and smaller costs may seem insignificant on their own, but they can add up over time. Failing to account for them can throw off your budget and create gaps you didn’t anticipate.

Not updating your budget regularly

A budget that isn’t reviewed or adjusted will quickly become outdated. As your business changes, your numbers should reflect that. Regular updates help ensure your budget stays relevant and useful.

Treating your budget as fixed

Your budget should guide your decisions, not limit them. Treating it as a rigid plan can make it harder to adapt to new opportunities or unexpected challenges. Flexibility is key to making your budget work in real-world conditions.

Avoiding these common mistakes doesn’t require perfection, just awareness and consistency. With the right habits in place and a clear understanding of what to watch for, your budget becomes a much more reliable tool for managing your business finances.

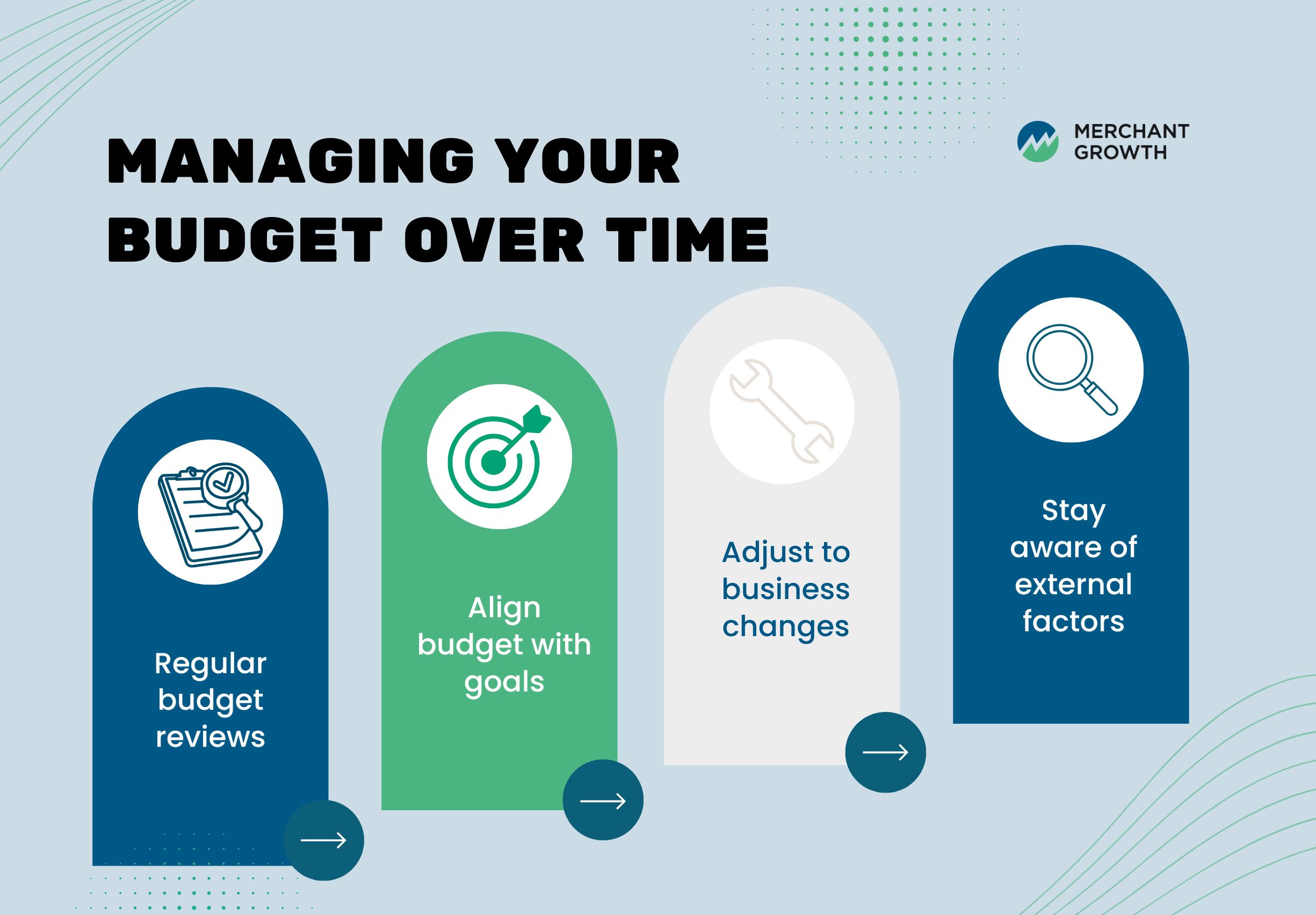

Staying on Track: How to Manage Your Budget Over Time

Once your budget is in place, the next step is making sure it stays useful. As your business changes, your numbers will shift, and how you manage your budget over time becomes just as important as how you build it.

Make Regular Budget Reviews a Habit

Routine reviews help you stay connected to your business finances and make informed decisions before small issues become larger problems. Whether you review your budget monthly or quarterly, consistency is key to keeping your numbers accurate and relevant.

During these check-ins, focus on understanding what’s changed and why. This isn’t just about tracking performance, it’s about identifying patterns and making adjustments that keep your business on track.

Some simple ways to make your reviews more effective include:

- Comparing your budgeted numbers to actual income and expenses

- Looking for patterns in your cash flow, such as seasonal trends or slower periods

- Identifying areas where you may be overspending or underutilizing resources

- Updating your projections based on real performance rather than assumptions

Even a short, consistent review can provide valuable insight into how your business is operating financially.

Align Your Budget with Your Business Goals

Your budget shouldn’t just reflect where your business is today, it should also support where you want it to go. Setting clear, measurable goals helps you turn your budget into a decision-making tool rather than just a tracking system.

For example, if your goal is to increase revenue, you might allocate more toward marketing or sales efforts. If your focus is improving profitability, you may look more closely at reducing unnecessary costs or improving margins.

When your budget is aligned with your goals, it becomes easier to prioritize spending and evaluate whether your decisions are moving your business in the right direction.

Adjust as Your Business Changes

No matter how carefully you plan, your business will evolve. Expenses may increase, revenue may fluctuate, or new opportunities may require you to shift your priorities.

Instead of treating your budget as fixed, think of it as flexible. Making adjustments based on real-world conditions allows you to stay responsive without losing control of your finances. This could mean reallocating funds, delaying certain expenses, or increasing investment in areas that are performing well.

Stay Aware of External Factors

Your business doesn’t operate in isolation, and external factors can have a direct impact on your budget. Changes in supplier costs, shifts in customer demand, or broader economic conditions can all affect your financial performance.

Staying informed about these changes helps you anticipate challenges and adjust your budget proactively. Even simple scenario planning—thinking through best-case, worst-case, and expected outcomes—can help you feel more prepared and confident in your decisions.

Staying on track with your budget isn’t about constant adjustments or reacting to every small change. It’s about building a consistent process that keeps you informed, flexible, and in control. With that foundation in place, your budget becomes a reliable tool you can use to support both your day-to-day operations and your long-term plans.

Tools to Help You Manage Your Small Business Finances

Managing your budget becomes much easier when you have the right tools in place. Modern accounting software can automate much of the process, giving you real-time visibility into your finances.

Platforms like QuickBooks, Wave, and FreshBooks allow you to track income and expenses, generate reports, and monitor your budget in one place. These tools are designed to simplify financial management, making them accessible even for business owners without an accounting background.

In some cases, working with a financial advisor can also provide valuable insight. While software helps with tracking, an expert can help you interpret your numbers and make more strategic decisions based on your goals.

Using a Budget to Plan Ahead (Without Overcomplicating It)

Once you have a working budget, it becomes a powerful tool for planning ahead. Whether you’re thinking about hiring, increasing your marketing spend, or investing in new equipment, your budget helps you understand what’s possible.

The key is to keep things practical. You don’t need complex forecasts or detailed models to make informed decisions. Instead, focus on how changes will impact your cash flow and whether your business can support them comfortably.

Budgeting isn’t about limiting your growth, it’s about giving you the confidence to pursue it with a clear understanding of your financial position.

Download Your Small Business Budget Template

Budgeting becomes much easier when you have a structure to follow. Our downloadable Monthly Budgeting Worksheet is designed to help you organize your revenue, expenses, and cash flow in one place.

You can use it to track your monthly estimates, calculate totals automatically, and monitor how your actual performance compares to your projections. Over time, this gives you a clearer picture of your business and helps you make more informed decisions.

Start Simple and Build From There

Budgeting doesn’t need to be complicated to be effective. The most important step is simply getting started and building a habit of tracking and reviewing your finances regularly.

As your business grows, your budget will naturally become more detailed and refined. What begins as a simple estimate can evolve into a powerful tool for decision-making, planning, and long-term success.

The goal isn’t to create a perfect budget from day one. It’s to create one that works for your business today—and improves with you over time.