Top Business Ideas in Canada: Profitable Ventures to Start Now

Ever dreamed of being your own boss, but unsure where to start? You're in the right place. Whether you're chasing a lifelong dream or looking for more freedom in your career, Canada’s supportive startup culture and wealth of resources make it a great time to take that leap. In fact, Canada has one of the highest small business ownership rates in the world, with over 1.19 million small businesses contributing to 97.8% of the total private sector workforce.¹ What’s more, the types of businesses thriving today are more diverse—and more accessible—than ever before.

From side hustles to full-time ventures, there’s no shortage of exciting paths to explore. In this guide, we’ll walk you through some of the most promising business ideas for Canadians in 2025—ones that are not only profitable and scalable but also realistic to start. We’ll take a look at rising industries, budget-friendly ideas you can launch from home, and smart ways to fund your business so you can grow with confidence.

Key takeaways

- Freelancing, real estate, and e-commerce are some of the most lucrative business sectors in Canada right now.

- Low-cost ideas like virtual assistance and dog walking are ideal for aspiring entrepreneurs with minimal startup capital.

- Home-based businesses and digital services continue to experience high demand, particularly post-pandemic.

- Choosing the right funding (loan, line of credit, or grant) can help accelerate your business growth.

The Best Businesses to Start Right Now in Canada

Freelancing

Freelancing is one of the most popular and accessible business options for Canadians, especially given the rise of remote work. As of 2023, 1 in 4 self-employed Canadians worked ‘gig work’ as their main job with the majority of freelancers being women.² This is likely due to the flexibility that freelance work allows. It is a great option if you are looking to choose your workload, set your own schedule and work from anywhere. If you’re wondering how contract work compares to traditional full-time employment, this blog breaks down the key differences to help you decide what suits you best.

Popular freelancing fields include writing, design, bookkeeping, marketing, and IT consulting. Online platforms like Upwork and Fiverr make it easy to find clients and build a reputation. Plus, startup costs are minimal, typically requiring only a computer and an internet connection.

- Startup cost: <$500

- Profitability: High, depending on skill and client base

Demand: Increasing due to remote work culture

Important considerations:

- Client acquisition: Consistently finding and retaining clients can be challenging, especially early on.

- Marketing yourself: Building a strong personal brand and online presence (LinkedIn, portfolio site, etc.) is essential.

- Time management: You're responsible for all aspects of your work, from invoicing to deadlines.

- Differentiation: Standing out in a crowded market often means niching down or showcasing unique skills.

Income fluctuation: Work can be feast-or-famine—budgeting and saving is crucial.

Construction

Canada’s construction industry is experiencing sustained growth, driven by infrastructure development, new housing demands, and an aging housing stock. Notably, 98.9% of construction businesses in the country are small businesses, highlighting the significant role independent operators play in this sector.¹

If you have experience in the trades and are considering taking the next step, starting your own construction business—whether in residential, commercial, or specialized services like electrical or plumbing—can be a highly viable path. With the right training and certifications, there is strong earning potential and a steady demand for skilled, reliable professionals.

- Startup cost: $5,000–$10,000

- Profitability: High

- Demand: Ongoing due to infrastructure growth and housing needs

Important considerations:

- Licensing & certifications: Depending on the province and trade, certifications may be required.

- Insurance & liability: Construction carries risk; appropriate coverage is critical.

- Skilled labour shortage: Finding qualified workers (or subcontractors) can be tough.

- Equipment & tools: Initial investment in tools or machinery can be high.

Cash flow: You may need to front costs before clients pay (materials, permits, etc.).

Catering

Canada's catering industry is thriving, with $3.8 billion in annual revenue as of 2023.³ The demand for catering services is particularly strong in urban areas, driven by corporate events, weddings, and private gatherings. Specializing in niche markets like vegan, gluten-free, or international cuisines can help you stand out in this competitive space.

If you love cooking and dream of sharing that passion with others, catering can be a rewarding way to turn your talent into a business. While food safety and some culinary know-how are essential, you don’t need a full commercial kitchen to get started—many successful caterers launch from their own home kitchens to keep costs low and build up gradually. Access to commercial kitchen space is also easier than ever, with apps like The Food Corridor allowing you to rent licensed kitchens by the hour or day.

- Startup cost: $2,000–$5,000

- Profitability: Moderate to high

- Demand: Steady in urban centers and growing in smaller communities

Important considerations:

- Licensing & food safety: Health inspections, food handler certifications, and licenses are a must.

- Seasonality: Demand can be event-driven and fluctuate depending on the time of year.

- Time & labor intensive: Long prep times, weekend work, and last-minute changes are common.

- Storage & delivery: Managing perishables and logistics requires planning.

Menu differentiation: Offering unique or specialized menus (e.g., plant-based) helps you stand out.

Social media management

Social media management is in high demand, particularly for small businesses looking to expand their digital footprint. According to Statista, over 77% of Canadians use social media, making it a crucial channel for business marketing.³ Small businesses, solopreneurs, and even larger corporations need skilled individuals to manage their social media platforms, create engaging content, and track performance.

With minimal startup costs—mainly a computer and social media know-how—this business is perfect for those looking to enter the digital marketing world.

- Startup cost: <$1,000

- Profitability: Moderate to high

- Demand: High among small businesses and solopreneurs

Important considerations:

- Results-driven: Clients often expect measurable growth (followers, engagement, conversions).

- Content creation: You’ll need design, copywriting, and trend-spotting skills.

- Time management: Managing multiple clients' calendars, content, and metrics can get overwhelming.

- Platform knowledge: Algorithms and best practices change frequently—stay updated.

- Client education: Some clients may not understand what social media can and can’t do.

Landscaping

Landscaping is a business that never goes out of style, particularly in suburban and rural areas. Services such as lawn care, tree trimming, and seasonal maintenance are always in demand and it is expected to continue to grow as both residential and commercial properties continue to be built.

Seasonality is a factor to consider—spring and summer will be your peak months, but some businesses expand into winter snow removal to balance year-round demand.

- Startup cost: $2,000–$8,000 (equipment-heavy)

- Profitability: High during peak seasons

- Demand: Consistent in suburban and rural areas

Important considerations:

- Weather dependency: Seasonal income is a reality—consider off-season services like snow removal.

- Physical demands: It’s labor-intensive and requires stamina, especially in peak season.

- Equipment maintenance: Tools and machines require ongoing investment and upkeep.

- Customer service: Good communication and reliability are key to repeat business.

Licensing: Some services (like pesticide use) may require certification.

Cleaning business

Whether it’s office cleaning, post-construction cleanup, or residential services, the cleaning industry in Canada remains one of the most stable and profitable. The industry is worth almost $2 billion annually, and demand is expected to grow as businesses and homeowners prioritize cleanliness.

With low startup costs—mainly cleaning supplies and transportation—you can start a cleaning business with minimal investment.

- Startup cost: $500–$2,000

- Profitability: Moderate to high

- Demand: Year-round with high retention potential

Important considerations:

- Reputation is everything: Cleanliness standards and trust are critical for client retention.

- Low barrier to entry: Easy to start, but also lots of competition—consider specializing (e.g., post-reno, eco-friendly).

- Scheduling: Clients may want evening or early morning services.

- Labor management: If you grow, finding reliable, detail-oriented staff can be tricky.

Supplies & safety: Ensure proper handling of cleaning chemicals and eco-friendly options if needed.

E-commerce

E-commerce is one of Canada’s fastest-growing industries. The global pandemic accelerated the shift to online shopping, and Canadians now spend over $45 billion annually on e-commerce, with 75% of Canadians shopping online regularly.⁴ Whether you're interested in dropshipping, selling handmade goods, or launching a niche online store, e-commerce provides endless opportunities for entrepreneurs.

Starting an online business is relatively low-cost, with dropshipping allowing you to sell products without holding inventory, and digital marketing tools helping to promote your brand. To keep costs down, you can also market your business organically through SEO and social media, without the need for paid ads. Ready to grow your online storefront? There are many financing options available to you.

- Startup Cost: <$1,000 (with dropshipping)

- Profitability: High

- Demand: Skyrocketing post-pandemic

Think e-commerce is the right fit for you but don’t know where to start? Check out these 8 tips to get your business off the ground and running.

Important considerations:

- Product sourcing: Inventory, shipping logistics, and supplier reliability are key factors.

- Customer acquisition: SEO, ads, and email marketing are ongoing necessities.

- Competition: It’s a crowded space—your niche and branding must stand out.

- Returns & customer service: Managing returns and questions can become time-consuming.

- Platform fees: Shopify, Etsy, Amazon, etc. come with fees—factor these into margins.

Real Estate

The Canadian real estate market, valued at approximately 257 billion in 2024, is projected to reach 324 billion by 2033, growing at a compound annual growth rate (CAGR) of 2.60% during 2025-2033.¹ This steady growth indicates a robust demand for real estate professionals, potentially like yourself.

Whether you're interested in becoming a real estate agent, property manager, or investor, the opportunities are substantial. While obtaining the necessary licenses and building a network are essential steps, the potential for significant returns makes this sector appealing.

- Startup Cost: $1,000–$10,000 (licensing, marketing, and initial expenses)

- Profitability: Variable, depending on market conditions and individual effort

- Demand: Consistent, with opportunities in both residential and commercial sectors

Important considerations:

- Licensing: Real estate agents require provincial licensing and ongoing education.

- Commission-based income: You don’t get paid until deals close—budgeting is crucial.

- Networking: Success relies heavily on building relationships and trust.

- Market sensitivity: Income can vary dramatically with housing market trends.

- Marketing expenses: Listings, ads, open houses, and personal branding cost money.

Online Courses & Coaching

Do you have knowledge or skills others are eager to learn? Whether it's business strategy, creative writing, coding, or wellness coaching, turning your expertise into an online course or coaching program can be both fulfilling and financially rewarding.

With the rise of digital platforms, creating and selling online courses or offering coaching services has become a lucrative business model. Whether you have expertise in business, personal development, technology, or the arts, there's a market for quality online education. This venture allows for flexibility and scalability, enabling you to reach a global audience from the comfort of your home.

- Startup Cost: $500–$5,000 (course development, platform fees, marketing)

- Profitability: High, with potential for passive income

- Demand: Growing, as more individuals seek to upskill online

Important considerations:

- Course design: Creating valuable, structured, and engaging content takes time and effort.

- Audience building: You’ll need an audience before you can effectively sell.

- Tech stack: Platforms (Teachable, Kajabi, etc.) come with learning curves and monthly fees.

- Trust & credibility: Establishing authority in your field is essential—testimonials, case studies, etc.

- Marketing funnels: A solid launch plan and email marketing strategy are crucial for success.

Personal Training & Fitness

The Canadian fitness industry has faced challenges in recent years, with a reported decline at a CAGR of 3.8% over the past five years, reaching an estimated $4.5 billion in 2024.⁵ Despite this, there remains a significant demand for personal training services, especially as more Canadians prioritize health and wellness. Offering personalized fitness programs, either in-person or virtually, can cater to this growing health-conscious demographic.

- Startup Cost: $1,000–$3,000 (certification, equipment, insurance)

- Profitability: Moderate to high, depending on client base and specialization

- Demand: Steady, with opportunities to expand into niche markets

Important considerations:

- Certification: Reputable certification (e.g., CanFitPro, ACE) is often required.

- Client consistency: Retaining clients and getting referrals are key to stable income.

- Liability insurance: Protect yourself in case of injury.

- Specialization: Consider niches like seniors, prenatal, or online training for differentiation.

- Scheduling flexibility: Clients may prefer early mornings, evenings, or weekends.

Industries on the Rise in Canada

As the economy evolves, there are certain industries that show no sign of slowing down—meaning more demand, more room for innovation, and more opportunity for small business owners to thrive. Whether you're planning your next move or still exploring ideas, keep an eye on these fast-growing sectors.

Check out the following industries and their growth rates projected until 2031.⁶

| Industry | Growth Rate |

|---|---|

| Arts, entertainment & recreation | 3.15% |

| Accommodations & hospitality | 3.36% |

| Food services | 2.27% |

| Management, administration & support | 2% |

| Legal, accounting, consulting & professional services | 1.56% |

| Repair, personal & household services | 1.54% |

Canada’s Most Profitable Ventures with Low - Medium Investment

If profitability is your top priority, these business ventures consistently deliver strong returns in the Canadian market without having to break the bank. Backed by steady demand and high earning potential, they represent some of the most financially rewarding paths for those looking to become self-employed. From booming digital industries to essential services, these are the types of businesses where your investment has the potential to pay off—big time.

- Technology

- Real Estate

- Ecommerce

- Consulting

- Digital marketing

- Fitness coaching

Low-Cost Business Ideas That Work

Not every successful business requires a large upfront investment. In fact, many entrepreneurs in Canada are building profitable businesses with little more than a laptop, a skillset, and a bit of hustle. If you're looking to start small and stay lean, these low-cost business ideas can help you get up and running without breaking the bank.

Copywriting

Starting a copywriting business is a great option for anyone with a knack for words. With virtually no overhead beyond a laptop and internet connection, you can offer services like website content, email marketing, and ad copy.

- Start-up cost: $100–$500 (website, portfolio tools)

- Operating cost: Very low; mostly time-based with optional subscriptions for grammar and productivity tools

Dog walking

Love animals? Dog walking is a simple, in-demand service in urban and suburban areas. You’ll need basic pet care knowledge, reliability, and perhaps some pet insurance to build trust with clients.

- Start-up cost: $200–$600 (marketing materials, pet insurance, scheduling app)

- Operating cost: Low; mostly transportation and insurance

Virtual assistant services

As more businesses go remote, the need for virtual assistants continues to rise. You can start by offering admin support, email management, scheduling, or social media assistance from home.

- Start-up cost: $300–$1,000 (computer, internet, branding, online tools)

- Operating cost: Low and scalable; mainly based on the platforms you use

Social Media Content Creation

Creating content for platforms like TikTok, Instagram, or YouTube can evolve into a profitable business through brand deals, affiliate marketing, and digital products. It’s highly accessible and ideal for creatives who enjoy video, trends, and building online communities.

- Start-up cost: $100–$500 (phone, editing tools, basic branding)

- Operating cost: Low; optional upgrades for lighting, software, or promotions

Graphic design

If you have an eye for design and know your way around software like Adobe Illustrator or Canva Pro, graphic design services are in high demand for small businesses, content creators, and startups.

- Start-up cost: $500–$1,200 (design software, website, branding)

- Operating cost: Moderate; mainly software subscriptions and occasional client tools

Event planning

Event planning can be launched on a shoestring budget if you start with small private or community events. You’ll need great organizational skills, people skills, and a strong local network.

- Start-up cost: $500–$1,500 (website, marketing, initial supplies)

- Operating cost: Variable; project-based costs depending on event size and scope

Home Sweet Hustle: Businesses You Can Run from Your House

There’s never been a better time to start a business from the comfort of home. Whether you’re looking to keep costs low, ditch the commute, or work on your own schedule, home-based businesses offer flexibility and strong earning potential. Here are five of the most popular options among Canadian entrepreneurs:

- Freelance writing or editing

- Virtual assistant services

- Handmade product sales (via Etsy or Shopify)

- Online coaching or consulting

- Dropshipping or e-commerce Store

These ventures are not only easy to launch with minimal investment, but they also allow you to grow at your own pace—right from your living room.

From Grants to Loans: Finding the Right Funding for Your Business

Once you've chosen a business idea that fits your skills and goals, the next big step is figuring out how to fund it. The good news? Canada offers a variety of financing options to help small business owners get off the ground—whether you're looking for a flexible line of credit or hoping to tap into non-repayable grant funding. Below, we break down some of the most common funding avenues, each suited to different needs and stages of growth.

Loans

Small business loans remain one of the most widely used ways to finance a new business in Canada. Whether you're just getting started or looking to scale, lenders like banks and online platforms offer secured and unsecured loans tailored to your needs. For a deeper look at the types of loans available—and how to qualify—check out this comprehensive guide to small business loans in Canada. If you're based in Ontario, there's also a region-specific breakdown to help you get started locally.

Financing

Need fast access to funds to cover short-term costs or invest in growth opportunities? Alternative financing options like our flexible solutions are designed to deliver quick capital without the long wait times of traditional banks. These can be a great fit for businesses that need working capital but don’t want to go through a lengthy loan application process.

Credit cards

Business credit cards are another practical tool for managing day-to-day expenses—especially when you're just starting out. They’re easy to access and often come with rewards, but be mindful of interest rates. Not sure whether a credit card or line of credit is a better fit? This comparison of credit cards vs. business lines of credit breaks down the pros and cons of each.

Line of credit

A business line of credit offers flexibility and peace of mind—giving you access to funds when you need them, without having to reapply. It's ideal for managing cash flow, covering seasonal dips, or handling unexpected expenses. For more on how it works and when to use it, read how a business line of credit can keep your Canadian business running.

Grants

Unlike loans, grants don’t need to be repaid, making them one of the most attractive options for entrepreneurs. Canada offers a variety of small business grants through both federal and provincial programs—often focused on innovation, hiring, or regional development. While competition can be steep, securing a grant can significantly reduce your startup burden.

Still weighing your options? These guides—Start-Up Funding Options and How to Choose the Right Type of Business Financing—offer valuable insights to help you make the smartest financial decision for your business.

Your Next Move: Turn These Ideas into Reality

Starting a business in Canada is not just a dream—it’s an achievable and highly rewarding path to financial independence. Whether you’re passionate about freelancing, opening a catering service, or diving into the world of e-commerce, there are plenty of opportunities to grow your business in Canada.

Take the time to create a business plan, outline your strategy, and explore funding options that suit your goals. Canada’s entrepreneurial ecosystem is here to support you at every stage of your business journey.

Looking for flexible business financing solutions? Whether you’re launching a cleaning company or scaling your e-commerce store, we offer fast, flexible financing tailored to Canadian entrepreneurs. Explore our business financing solutions today to help bring your vision to life!

References

- https://ised-isde.canada.ca/...2023

- https://www150.statcan.gc.ca/...240603b

- https://www.marketresearch.com/...38815647

- https://www.statista.com/...899045

- https://stallionexpress.ca/...e-commerce-in-canada

- https://www.imarcgroup.com/...real-estate-market

- https://www.perfectgym.com/...fitness-industry-statistics

- https://www.shopify.com/...most-profitable-businesses

Getting Started with Budgeting for Your Small Business Finances

Most Canadian small business owners don’t struggle because they aren’t making money, they struggle because it’s hard to see how that money is actually working in the business. You might be covering expenses, bringing in sales, and staying busy, but still feel unsure about what you can afford to spend, save, or reinvest. Without a clear plan in place, even healthy businesses can feel financially unpredictable.

That’s where budgeting comes in. A budget isn’t just a financial document you create once and forget about; it’s a practical tool that helps you understand your business, make better decisions, and stay in control of your cash flow.

Whether you’re building your first budget or revisiting your approach, the goal isn’t perfection, it’s clarity. You won’t have every number exactly right from the start, but taking the time to map things out will give you a stronger understanding of how your business actually operates.

Key Takeaways

- A budget is a simple plan that tracks your income and expenses

- It helps you understand and manage your cash flow

- Every budget is built from revenue, fixed costs, and variable expenses

- Budgets should be reviewed and adjusted regularly

- Budgeting supports both day-to-day stability and future growth

What Is a Budget for a Small Business?

At its core, a small business budget is a plan that outlines how your business will earn and spend money over a set period of time. It brings together your expected revenue, your costs, and what remains, giving you a clear view of your financial position.

A typical budget is built from a few key components. This includes your projected income, fixed costs like rent and payroll, and variable expenses such as inventory, marketing, or utilities. It may also account for one-time expenses and the timing of when money comes in and goes out.

You can think of it as a working snapshot of your business finances. For example, if you expect to bring in $20,000 in a month and your total expenses are $18,000, your budget shows the margin you’re working with. It also highlights how those numbers are structured, helping you see where your money is being allocated.

Why Budgeting Matters (Even If You’re Just Getting Started)

When you’re running a small business, timing matters just as much as profitability. You might be making sales, but if payments are delayed or expenses hit all at once, it can still feel like you’re constantly playing catch-up. Budgeting helps bring structure to that uncertainty.

A well-built budget allows you to anticipate upcoming expenses, plan for slower periods, and make decisions with more confidence. It also reduces the stress that comes from not knowing whether you can afford to hire, invest in marketing, or take on new opportunities.

Even if your business is still in its early stages, budgeting gives you a foundation to build on. It doesn’t require perfect data, it just requires a willingness to track, estimate, and adjust as you go.

What Goes Into a Small Business Budget

Every small business budget is built from a few core components. Once you understand how each of these works, budgeting becomes much more practical and far less overwhelming. Instead of guessing where your money is going, you can start to see how each piece fits together.

Revenue

Revenue is the money your business expects to bring in over a given period, and it’s the starting point for your entire budget. This can include one-time sales, ongoing service contracts, or recurring income streams like subscriptions or retainers.

When estimating revenue, it’s important to stay grounded in reality. If your sales fluctuate month to month, look at historical averages or identify patterns such as seasonality or slower periods. Overestimating revenue is one of the most common budgeting mistakes, and it can lead to spending decisions that aren’t sustainable. A conservative estimate gives you a more stable foundation to work from and helps prevent shortfalls later on.

Fixed Costs

Fixed costs are the expenses that remain relatively consistent each month, regardless of how your business is performing. These typically include rent, salaries, insurance, software subscriptions, and loan payments.

Because fixed costs don’t change often, they form the baseline of your budget. Understanding these expenses clearly allows you to determine the minimum amount of revenue your business needs to generate just to operate. This is especially important for newer businesses, as it helps define your financial “starting point” before accounting for growth or additional spending.

Variable Costs

Variable costs fluctuate based on your level of business activity. These can include inventory, shipping, utilities, payment processing fees, or marketing spend.

Unlike fixed costs, these expenses can increase as your business grows, which makes them important to track closely. For example, higher sales may lead to higher inventory costs or increased transaction fees. While that growth is positive, it still needs to be accounted for in your budget to maintain healthy margins. Keeping a close eye on variable costs helps you understand how efficiently your business is operating as it scales.

One-Time Expenses

One-time expenses are costs that don’t occur regularly but can still have a significant impact on your finances. This might include purchasing new equipment, redesigning your website, investing in a rebrand, or running a large marketing campaign.

Because these expenses are less predictable, they’re often overlooked in early budgets. However, failing to plan for them can disrupt your cash flow when they arise. Setting aside a portion of your budget for occasional or unexpected costs can help you stay prepared without putting pressure on your day-to-day operations.

Cash Flow Timing

Cash flow isn’t just about how much money your business makes, it’s about when that money actually arrives. Even profitable businesses can run into challenges if there’s a delay between earning revenue and receiving payment.

For example, if you invoice clients on net terms, you may need to cover expenses weeks before payment is received. A strong budget accounts for these timing differences, helping you plan ahead and avoid gaps where cash might be tight. Understanding your cash flow timing allows you to make more informed decisions about spending, saving, and reinvesting in your business.

When you bring all of these components together, your budget becomes more than just a list of numbers. It becomes a clear, structured view of how your business operates financially. Once you have that visibility, the next step is understanding how to use it, because knowing your numbers is only valuable if it helps you make better day-to-day decisions.

How to Create Your First Small Business Budget

Creating your first budget doesn’t need to be complicated. The goal is to build a clear, workable starting point that reflects how your business operates today, not a perfect projection of where you hope it will be. Once you have that foundation in place, you can refine and improve it over time as you gather more data and experience.

![Infographic of how to create your first small business budget]](https://www.merchantgrowth.com/wp-content/uploads/2025/04/How-to-Create-a-Small-Business-Budget-Infographic.jpg)

1. Estimate Your Income

Start by reviewing past sales if you have them, or by making realistic projections if you’re just getting started. Look for patterns in your revenue, such as seasonal trends, busy periods, or slower months, to guide your estimates.

If your income varies, it’s better to take a conservative approach rather than assuming your highest-performing months will continue. This gives you more room to manage expenses without putting pressure on your cash flow. Over time, as you track actual performance, your revenue estimates will become more accurate and reliable.

2. List Your Fixed Costs

Next, outline all of your recurring expenses that stay relatively consistent each month. These may include rent, payroll, insurance, subscriptions, loan payments, and any other essential costs required to keep your business running.

Because these expenses are predictable, they provide a clear baseline for your budget. Knowing exactly what you need to cover each month helps you understand the minimum revenue required to operate your business sustainably. This step is often the most straightforward, but it’s also one of the most important.

3. Track Variable Expenses

Variable expenses require a bit more attention because they can change depending on your level of business activity. This might include inventory purchases, shipping costs, utilities, marketing spend, or transaction fees.

Review past transactions where possible, or make informed estimates based on how your business operates. It’s generally safer to slightly overestimate these costs, especially in the early stages, to avoid under-budgeting. As you track these expenses over time, you’ll gain a clearer understanding of how they fluctuate and how they impact your margins.

4. Plan for One-Time or Unexpected Costs

Not every expense shows up on a monthly basis. Equipment upgrades, website improvements, or one-time marketing initiatives can all create sudden financial pressure if they aren’t accounted for in advance.

Setting aside even a small portion of your budget for these types of expenses can make a meaningful difference. It allows you to handle opportunities or unexpected costs without disrupting your day-to-day operations or relying on last-minute solutions.

5. Map Out Your Cash Flow

Once you’ve outlined your income and expenses, the next step is to look at timing. When does money come in, and when does it go out? This is where many businesses run into challenges, especially if payments are delayed or expenses are due up front.

Mapping out your cash flow helps you identify periods where cash might be tight and plan accordingly. It also gives you a better sense of how much flexibility you have when making decisions about spending or investing in your business.

6. Review and Adjust Regularly

A budget is not something you set once and leave untouched. As your business changes, your numbers will change with it. That’s why regular reviews are essential to keeping your budget accurate and useful.

Set a schedule—monthly or quarterly—to compare your projections against actual results. Look for gaps, trends, or areas where adjustments are needed. Over time, this process helps you build a budget that reflects your business more accurately and supports better decision-making.

By following these steps, you’re not just creating a budget—you’re building a system that helps you understand and manage your finances more effectively. And once that system is in place, the next step is learning how to make it work for you in practice, from choosing the right approach to avoiding common pitfalls.

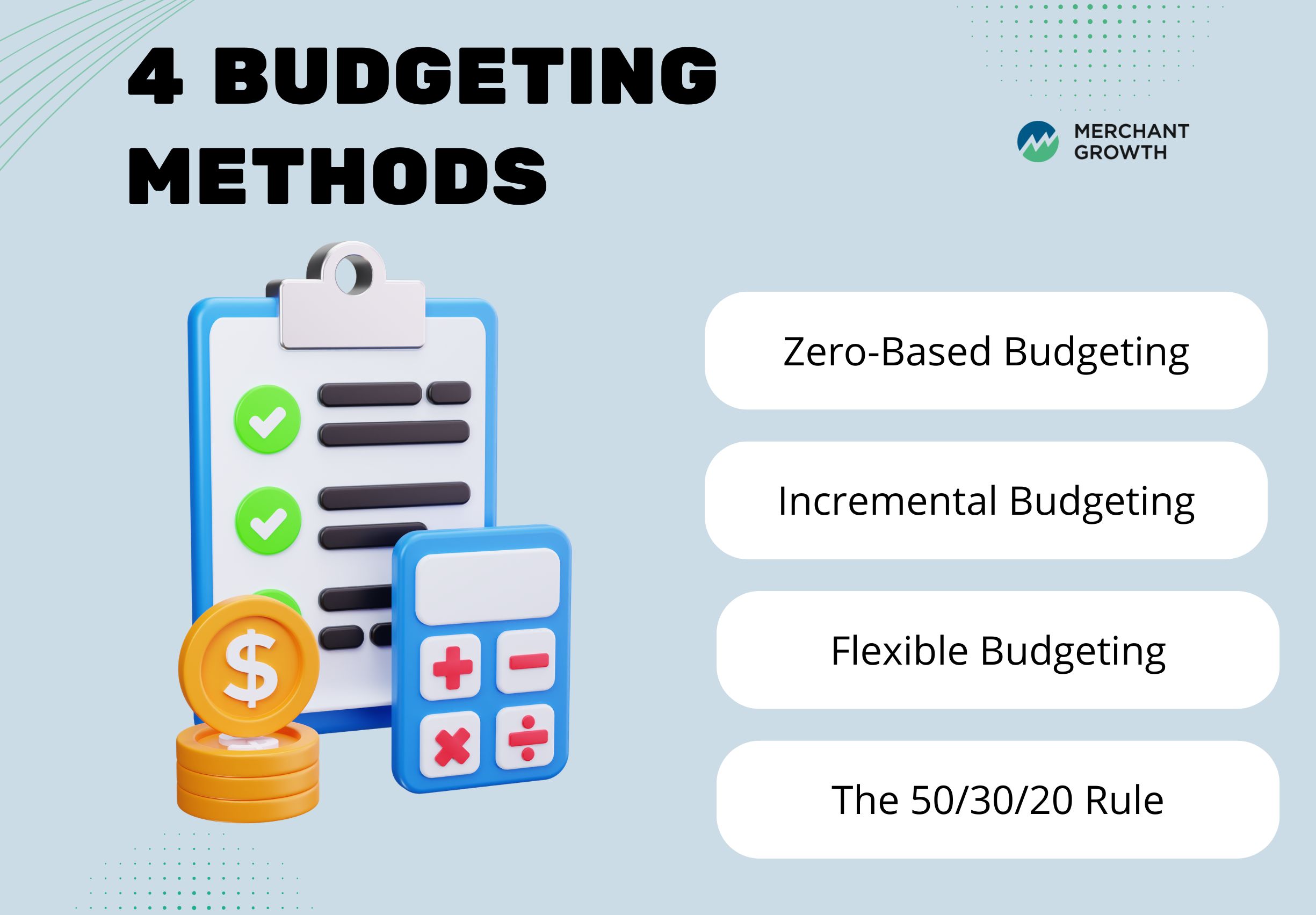

Budgeting Methods (Made Simple)

There’s no single “right” way to build a budget. The best approach depends on how your business operates, how predictable your revenue is, and how much time you want to spend managing your finances. What matters most is choosing a method that’s practical, easy to maintain, and flexible enough to grow with your business.

Zero-Based Budgeting

Zero-based budgeting starts from scratch each period, meaning every expense must be reviewed and justified before it’s included. Instead of relying on past budgets, you build your plan based on current priorities and needs.

This method is especially useful if you’re trying to gain tighter control over spending or identify areas where costs can be reduced. It forces you to evaluate each expense more critically, which can help eliminate inefficiencies. However, it can be more time-intensive, making it better suited for business owners who want a hands-on approach or are going through a period of change.

Incremental Budgeting

Incremental budgeting takes your previous budget as a starting point and adjusts it based on expected changes, such as growth, inflation, or new expenses. This is one of the most common approaches because it’s simple and relatively quick to implement.

For businesses with stable operations and predictable costs, incremental budgeting provides a practical way to plan without rebuilding everything from the ground up. However, it’s important to review your existing expenses carefully, as this method can sometimes carry forward unnecessary costs if they aren’t reassessed regularly.

Flexible Budgeting

Flexible budgeting is designed to adapt as your revenue changes. Instead of setting fixed spending limits, this approach allows certain expenses to scale up or down depending on how your business is performing.

This method works well for businesses with seasonal sales, fluctuating demand, or variable income streams. For example, if revenue increases, you might increase your marketing spend or inventory accordingly. Flexible budgeting helps you stay responsive and avoid overcommitting during slower periods, making it a strong option for businesses that need agility.

The 50/30/20 Rule

Although it’s commonly used in personal finance, the 50/30/20 rule can be adapted as a simple framework for small business budgeting. It divides your budget into three categories: essential expenses, growth-related spending, and savings or debt repayment.

For example, you might allocate around 50% of your budget to core operating costs, 30% to growth initiatives like marketing or product development, and 20% toward building reserves or paying down debt. While the exact percentages may vary depending on your business, this structure can help you maintain balance and avoid overextending in any one area.

Choosing a budgeting method gives you structure, but it’s how you apply it day to day that makes the biggest difference. Small habits, consistent tracking, and realistic assumptions are what turn a plan into something you can actually rely on.

Practical Budgeting Tips for Small Business Owners

Budgeting works best when it’s supported by consistent habits and realistic expectations. Small adjustments in how you manage your finances can make a significant difference over time, especially when they’re applied consistently.

Here are a few practical ways to make your budget more effective:

Keep your business and personal finances separate

Mixing personal and business expenses makes it much harder to track where your money is going. Keeping them separate gives you a clearer, more accurate view of your business performance and simplifies everything from budgeting to tax preparation.

Set aside money for taxes early

Taxes are one of the most commonly overlooked expenses in small business budgeting. Setting aside a portion of your revenue as you earn it helps you avoid large, unexpected payments and reduces financial stress later on.

Build a contingency buffer

Unexpected costs are part of running a business, whether it’s equipment repairs, supplier changes, or slower sales periods. Even a small reserve built into your budget can help you handle these situations without disrupting your operations.

Be conservative with your revenue estimates

It’s easy to assume your best months will continue, but that can lead to overspending. Using more conservative estimates helps create a buffer and keeps your budget realistic and sustainable.

Use tools that match your workflow

Whether it’s a simple spreadsheet or accounting software, the best system is one you’ll actually use. Consistency matters more than complexity when it comes to managing your budget effectively.

These habits may seem simple, but they create a strong foundation for managing your budget more effectively. Once these are in place, it becomes easier to spot where things can go wrong, and how to avoid common budgeting mistakes.

Common Budgeting Mistakes to Avoid

Even with the best intentions, small budgeting mistakes can create bigger financial challenges over time. Being aware of these common pitfalls can help you build a budget that’s more accurate, flexible, and reliable.

Here are a few mistakes to watch out for:

Overestimating your revenue

It’s easy to assume your business will continue performing at its peak, but relying on overly optimistic projections can lead to spending decisions that aren’t sustainable. A more conservative approach gives you room to adapt if sales fluctuate.

Underestimating variable costs

Variable expenses like inventory, shipping, and marketing can change quickly as your business grows. If these costs aren’t tracked carefully, they can quietly reduce your margins and impact your overall financial stability.

Ignoring small or irregular expenses

One-time purchases and smaller costs may seem insignificant on their own, but they can add up over time. Failing to account for them can throw off your budget and create gaps you didn’t anticipate.

Not updating your budget regularly

A budget that isn’t reviewed or adjusted will quickly become outdated. As your business changes, your numbers should reflect that. Regular updates help ensure your budget stays relevant and useful.

Treating your budget as fixed

Your budget should guide your decisions, not limit them. Treating it as a rigid plan can make it harder to adapt to new opportunities or unexpected challenges. Flexibility is key to making your budget work in real-world conditions.

Avoiding these common mistakes doesn’t require perfection, just awareness and consistency. With the right habits in place and a clear understanding of what to watch for, your budget becomes a much more reliable tool for managing your business finances.

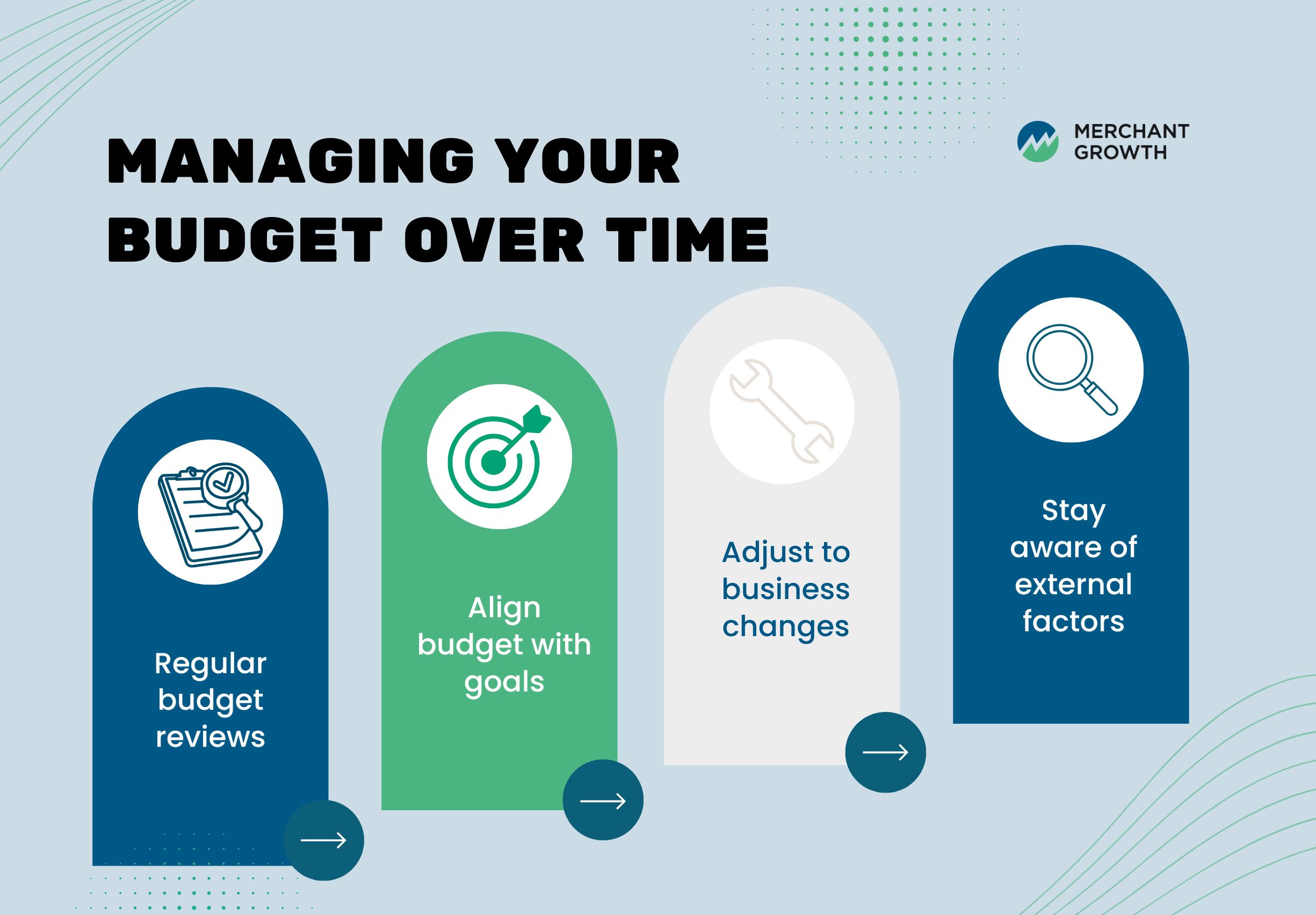

Staying on Track: How to Manage Your Budget Over Time

Once your budget is in place, the next step is making sure it stays useful. As your business changes, your numbers will shift, and how you manage your budget over time becomes just as important as how you build it.

Make Regular Budget Reviews a Habit

Routine reviews help you stay connected to your business finances and make informed decisions before small issues become larger problems. Whether you review your budget monthly or quarterly, consistency is key to keeping your numbers accurate and relevant.

During these check-ins, focus on understanding what’s changed and why. This isn’t just about tracking performance, it’s about identifying patterns and making adjustments that keep your business on track.

Some simple ways to make your reviews more effective include:

- Comparing your budgeted numbers to actual income and expenses

- Looking for patterns in your cash flow, such as seasonal trends or slower periods

- Identifying areas where you may be overspending or underutilizing resources

- Updating your projections based on real performance rather than assumptions

Even a short, consistent review can provide valuable insight into how your business is operating financially.

Align Your Budget with Your Business Goals

Your budget shouldn’t just reflect where your business is today, it should also support where you want it to go. Setting clear, measurable goals helps you turn your budget into a decision-making tool rather than just a tracking system.

For example, if your goal is to increase revenue, you might allocate more toward marketing or sales efforts. If your focus is improving profitability, you may look more closely at reducing unnecessary costs or improving margins.

When your budget is aligned with your goals, it becomes easier to prioritize spending and evaluate whether your decisions are moving your business in the right direction.

Adjust as Your Business Changes

No matter how carefully you plan, your business will evolve. Expenses may increase, revenue may fluctuate, or new opportunities may require you to shift your priorities.

Instead of treating your budget as fixed, think of it as flexible. Making adjustments based on real-world conditions allows you to stay responsive without losing control of your finances. This could mean reallocating funds, delaying certain expenses, or increasing investment in areas that are performing well.

Stay Aware of External Factors

Your business doesn’t operate in isolation, and external factors can have a direct impact on your budget. Changes in supplier costs, shifts in customer demand, or broader economic conditions can all affect your financial performance.

Staying informed about these changes helps you anticipate challenges and adjust your budget proactively. Even simple scenario planning—thinking through best-case, worst-case, and expected outcomes—can help you feel more prepared and confident in your decisions.

Staying on track with your budget isn’t about constant adjustments or reacting to every small change. It’s about building a consistent process that keeps you informed, flexible, and in control. With that foundation in place, your budget becomes a reliable tool you can use to support both your day-to-day operations and your long-term plans.

Tools to Help You Manage Your Small Business Finances

Managing your budget becomes much easier when you have the right tools in place. Modern accounting software can automate much of the process, giving you real-time visibility into your finances.

Platforms like QuickBooks, Wave, and FreshBooks allow you to track income and expenses, generate reports, and monitor your budget in one place. These tools are designed to simplify financial management, making them accessible even for business owners without an accounting background.

In some cases, working with a financial advisor can also provide valuable insight. While software helps with tracking, an expert can help you interpret your numbers and make more strategic decisions based on your goals.

Using a Budget to Plan Ahead (Without Overcomplicating It)

Once you have a working budget, it becomes a powerful tool for planning ahead. Whether you’re thinking about hiring, increasing your marketing spend, or investing in new equipment, your budget helps you understand what’s possible.

The key is to keep things practical. You don’t need complex forecasts or detailed models to make informed decisions. Instead, focus on how changes will impact your cash flow and whether your business can support them comfortably.

Budgeting isn’t about limiting your growth, it’s about giving you the confidence to pursue it with a clear understanding of your financial position.

Download Your Small Business Budget Template

Budgeting becomes much easier when you have a structure to follow. Our downloadable Monthly Budgeting Worksheet is designed to help you organize your revenue, expenses, and cash flow in one place.

You can use it to track your monthly estimates, calculate totals automatically, and monitor how your actual performance compares to your projections. Over time, this gives you a clearer picture of your business and helps you make more informed decisions.

Start Simple and Build From There

Budgeting doesn’t need to be complicated to be effective. The most important step is simply getting started and building a habit of tracking and reviewing your finances regularly.

As your business grows, your budget will naturally become more detailed and refined. What begins as a simple estimate can evolve into a powerful tool for decision-making, planning, and long-term success.

The goal isn’t to create a perfect budget from day one. It’s to create one that works for your business today—and improves with you over time.

More than half of Canadian small businesses say they are feeling the sting of escalating tariffs between the United States and Canada, according to a new survey by Merchant Growth, a digital financing and growth solution for small businesses.

The survey, which polled 130 small business owners, reveals widespread impacts on workforce decisions, rising costs, and mounting uncertainty as companies scramble to adapt to the ongoing trade dispute.

Workforce Reductions Ripple Across Industries

The ripple effects of U.S. tariffs and Canada’s counter-tariffs have been felt across various industries, from automotive and steel to consumer goods. Major corporations like Stellantis, the automaker behind Chrysler, Dodge, and Jeep, temporarily laid off 4,500 Canadian employees, while Sheertex, a Canadian maker of unbreakable pantyhose, reduced its workforce by 40%.

The survey found that these large-scale layoffs have trickled down to small businesses as well. More than one in four (29%) small businesses have adjusted their workforce and/or hiring plans due to the tariffs.

Specifically, 17% of businesses have reduced their workforce and paused hiring, while 12% have only paused hiring plans. Around one in 10 (11%) have yet to make any changes but plan to do so soon. In contrast, three in five (60%) report that the tariffs have had no impact on their workforce or hiring plans.

Rising Costs Passed to Consumers

Tariffs are pushing up costs for businesses, and many are passing some of those increases onto consumers. Among companies facing higher costs due to tariffs, 39% have raised prices, though most (81%) have passed on only a quarter or less of the added expense.

This trend is already showing up in consumer prices. Statistics Canada data show that grocery prices rose 2.8% year-over-year in February 2025, with the pace accelerating to 3.2% in March. Coffee, in particular, is expected to become more expensive, as Canadian roasters and retailers face higher costs for beans and equipment sourced from the U.S. and other countries hit by new tariffs.

Adaptation Strategies: Diversification and Caution

Despite the challenges, only about half (51%) of small businesses surveyed have implemented strategies to manage tariff impacts. Among those taking action:

- 42% diversified supply chains by reducing reliance on U.S. suppliers

- 20% pursued new export markets outside of the U.S.

- 13% completely exited the U.S. market

- 5% applied for federal support programs (e.g. EDC’s $5B Trade Impact Program, BDC loans)

- 3% invested in automation/tech upgrades to offset increased operational costs

- 56% have implemented other strategies

What Small Businesses Want from the Next Government

When asked which federal measures would help most, business owners gave mixed responses:

- 38% said increasing access to low-interest loans for market diversification

- 27% said deferred tax payments for small businesses

- 22% said permanent tax incentives for small businesses, like expanding the small business deduction limit and a potential refundable credit on expenses for non-U.S. supplier development

- 22% said payroll relief in the form of wage subsidies

- 13% said eliminating barriers to interprovincial trade

While some federal support programs exist, access can be limited, and many businesses say more targeted relief is needed to weather the ongoing trade tensions.

At Merchant Growth, we’re committed to helping Canadian small businesses navigate this uncertainty. Whether it’s through flexible financing, strategic advice, or advocating for policy changes, our goal is to empower entrepreneurs to adapt, grow, and thrive – even in turbulent times.

The road ahead may be uncertain, but with the right support and a willingness to adapt, Canadian small businesses can weather the storm and emerge stronger on the other side.

Want a deeper look at the data? Our full report offers a detailed breakdown of survey findings, including industry-specific impacts, workforce trends, and what small businesses say they need from policymakers.

🔹 Download: Small Business Pulse Customer Experience

As a small business owner, you’ve probably heard about tariffs for the last little while, and for good reason.

Trade tensions between Canada and the U.S. are nothing new, but when U.S. tariffs on Canada come into play, they can have a serious impact on businesses of all sizes. From decreased demand to disrupted supply chains, these economic policies can directly affect your bottom line.

Tariffs don’t usually change overnight, but we’re in uncharted territory right now, with decisions being made and put into action faster than ever.

Take what happened in early 2025. A 25% tariff on Canadian imports was announced by U.S. President Donald Trump, shaking up industries that depend on cross-border trade. While negotiations eventually put it on pause, the uncertainty lingered, leaving businesses scrambling to adjust.

If nothing else, this was a wake-up call: tariffs can hit anytime, no matter who’s in charge. Governments shift, trade policies evolve, and businesses are often caught in the crossfire. A new tariff can lower demand for Canadian products, disrupt supply chains, and force tough pricing decisions that impact your bottom line.

But there’s good news: You’re not powerless. With the right approach, you can prepare, adapt, and keep your business strong. That way, as changes come, you're less likely to be caught off guard.

What Are Tariffs and Who Pays Them?

At their core, tariffs are taxes on imported goods. When the U.S. imposes tariffs on Canadian products, demand for Canadian goods may decrease as they become more expensive for American buyers, in comparison to the price pre-tariffs.

Who Pays the Tariffs?

A common misconception is that Canadian businesses pay the tariff. They don’t. It’s actually the U.S. importer (buyer) who foots the bill. But that doesn’t mean Canadian businesses are off the hook. Higher costs for American buyers can make Canadian products less competitive, leading to lower sales, pricing pressure, or even lost customers

Here’s how that plays out in real life: Say you own a furniture company in British Columbia that sells custom-made wooden tables to American buyers. If the U.S. slaps a 20% tariff on Canadian wood products, that means the U.S. retailer has to cough up an extra 20% just to bring your tables into the U.S. Now, they’ve got a choice: eat the cost of the tariffs themselves or bump up their prices and pass that cost on to their customers.

Why Should We Care? How Do the Trump Tariffs Affect Canada's Economy?

Tariffs don’t just affect individual businesses—they send shockwaves through the entire Canadian economy.

Take a local coffee roaster that exports specialty beans to the U.S. If tariffs suddenly make those beans more expensive for American buyers—because American importers will be paying the tariffs on items imported from Canada—the U.S. buyer might switch to a local supplier instead.

When the cost of exporting to the U.S. goes up, Canadian businesses are forced to make tough decisions: raise their prices for Canadian customers to offset lost revenue, lower their prices for American customers, or find new markets. Multiply this scenario across industries, and the ripple effect becomes clear.

For manufacturers, tech companies, and retailers, tariffs don’t necessarily mean higher costs for Canadian businesses—but they do mean a tougher time selling to U.S. customers. Since American buyers are the ones footing the bill, they might start looking elsewhere, pushing for discounts, or just buying less. This could mean less profit for you.

But here’s the thing: as a small business owner, you can’t afford to just wait and see what happens if or when tariffs are imposed. No matter what decisions come from the Trump administration (or any other administration), it’s important to stay informed, be flexible, and have a plan in place.

Government policies can shift at any time, but smart business owners stay prepared.

Canadian Businesses That Could Take a Hit

Some industries are more vulnerable to tariffs than others. If your business falls into one of these sectors, it’s a good idea to start preparing now:

- Manufacturing & Construction: If you sell steel, aluminum, or other materials to the U.S., Trump’s tariffs make your goods more expensive for American buyers. That could mean fewer orders, tougher price negotiations, or customers looking elsewhere.

- Food & Beverage: Selling food to the U.S.? Tariffs can bump up your prices, making it harder to compete with local producers. And if you buy ingredients from the U.S., your costs could go up too.

- Automotive & Trades: If your business deals with car parts, machinery, or equipment, tariffs could make your products less appealing to U.S. buyers, pushing them to look for alternatives.

How Could U.S. Tariffs Affect Your Canadian Business?

When the U.S. imposes tariffs on Canadian goods, businesses that rely on trade can feel the effects almost immediately, shaking up your operations in ways that are hard to predict. Here’s how the Trump tariffs could impact Canada’s economy.

1. Less profit

Like we saw with the furniture example, the tariffs Trump imposes can make Canadian products significantly more expensive for U.S. buyers. A 25% tariff means something that used to sell for $1,000 in the U.S. now costs $1,250. That kind of price hike could push American customers to look for cheaper, locally made alternatives—leaving Canadian businesses with fewer sales and tighter margins.

You can quickly figure out how much tariffs will cost using a calculator, so you’re not caught off guard by unexpected fees.

Ultimately, if you sell to the U.S., you may make less money, be forced to raise your prices in Canada or other markets and risk losing customers. Either way, it cuts into your bottom line and makes it harder to stay competitive.

2. Supply Chain Ripple Effects

Even if you don’t sell to the U.S., you’re not totally off the hook. If your Canadian suppliers export to the U.S. and start losing business because of tariffs, they might try to make up for the loss by raising prices elsewhere—including in Canada. That means you could end up paying more for materials or products you rely on, even if your business has nothing to do with cross-border trade.

3. Job Cuts and Layoffs

When businesses lose sales or struggle with higher costs, they often have to cut expenses. That can mean fewer hours for workers, hiring freezes, or even layoffs. Industries like farming, manufacturing, and natural resources—where a lot of goods are sold to the U.S.—could be hit the hardest.

How to Stay Prepared Against U.S. Tariffs—No Matter What Happens

You can’t control tariffs on Canadian goods, but you can control how your business handles them. The key is to stay flexible and ready for anything.

1. Expand Your International Customer Base

If the U.S. imposes tariffs, your biggest challenge isn’t higher costs, it’s that your products become less competitive for American buyers. If they start looking elsewhere, relying too much on U.S. sales could put your business at risk.

One way to stay ahead is to diversify where you sell. If you mainly do business in the U.S., now might be the time to explore more Canadian markets or even expand into other countries. Canada has strong trade agreements with regions such as Europe and Asia, which could open up new opportunities.

But if completely expanding or changing markets isn’t an option, building stronger relationships with U.S. buyers can help you weather the storm. That might mean offering flexible pricing, long-term contracts, or highlighting what makes your product worth the extra cost.

The more options you have, the less one trade policy can throw off your business.

2. Focus on Your Canadian Market

If U.S. tariffs are making it harder to turn a profit, it’s time to shift your focus back home. A strong Canadian customer base means you’re not depending on U.S. sales, giving you more control over your business. Here’s how you can make that happen:

- Highlight the benefits of “Canadian-made”: Canadians love supporting local and Canadian businesses, so focus on marketing your goods as Canadian-made. Share your story, talk about what makes your stuff special, and remind people why buying local matters.

- Encourage customer loyalty: Offer loyalty perks, exclusive deals, or even free shipping within Canada to make shopping with you more appealing than ordering from the U.S.

- Find new Canadian customers: If most of your focus has been on U.S. sales, it’s time to see where else in Canada you can grow. Are there provinces or industries you haven’t tapped into yet? Expanding locally could bring in new customers who’d love what you offer.

- Take advantage of Canadian business programs: Look into government grants, funding, or trade programs designed to support local businesses. You might find financial support that makes shifting your focus easier and more profitable.

By putting more energy into your Canadian customers, you’re building a stronger, more stable business.

3. Stay Informed on Trade Policies

Trade policies can change quickly, and the tariffs Canada faces today might not be the same tomorrow. Keep up with industry news, sign up for trade newsletters, and join small business groups that talk about these issues. If tariffs affect your industry in a big way, a trade consultant might also be something worth considering to help you plan ahead.

4. Adjust Your Pricing

Maybe the thought of lowering your prices makes you cringe a little. Totally fair. But when U.S. buyers are dealing with tariffs and seeing higher costs, they might start second-guessing their orders. Instead of immediately slashing prices or losing customers to cheaper alternatives, think about the bigger picture—loyalty can be more valuable than short-term profit.

A small price adjustment now might feel like a hit, but keeping a loyal customer is often worth more than constantly chasing new ones. Maybe you offer a small discount for repeat orders or better payment terms to make things easier on their end. A little flexibility could go a long way in showing them you value their business—without hurting your bottom line.

At the same time, don’t just assume they’ll understand what’s happening.

If you’ve built good relationships with your U.S. buyers, be upfront. Let them know why prices are shifting and what you’re doing to help keep things fair. If they trust you, they’re way more likely to stick around, and in the long run, a steady customer beats a one-time sale any day.

5. Secure Flexible Financing

The impact of tariffs can put a strain on your cash flow. If your American customers start pulling back because of the tariffs they have to pay, having quick access to funds can help you keep your business on track even while you’re taking a hit.

A business line of credit is a great safety net. It gives you the flexibility to cover short-term costs—whether it’s dealing with tariff-related expenses, slow business seasons, or jumping on a new opportunity.

At Merchant Growth, we offer an option for small businesses looking for a faster and more flexible alternative to traditional bank loans. Our business line of credit is designed to help businesses cover short-term costs, whether it’s dealing with tariff-related expenses, seasonal slowdowns, or taking advantage of a new opportunity. With this type of financing, you can:

- Get access to funds quickly without a drawn-out approval process

- Borrow only the amount you need and repay it on terms that work for your cash flow

- No collateral needed—your personal and business assets stay safe

When money gets tight, having a flexible funding option can help you handle surprises and keep your business moving forward.

6. Build an Emergency Fund

When it comes to potential Trump tariffs, or trade shifts, or economic curveballs, you never know when something might hit your bottom line. That’s why having an emergency fund isn’t just smart, it’s survival.

Ideally, you’d have three to six months’ worth of expenses set aside so you’re covered if cash flow slows or sales take a hit. But let’s be real—saving that much overnight isn’t easy. The good news? Small steps add up.

If saving that much feels out of reach, start small. Set aside a percentage of your revenue each month. Even a little cushion can help you handle surprises and keep things running smoothly when the economy shifts.

Final Thoughts: Stay Informed, Stay Ready

Tariffs are just one of many curveballs small businesses have to deal with. While you may not be the one directly paying the tariffs if the U.S. decides to impose them, you do still feel the ripple effects.

Maybe it’s tougher to compete in the U.S. market, maybe your customers start pushing for lower prices, or maybe your suppliers adjust their own prices to make up for lost business.

But here’s the thing: you’ve handled challenges before, and you’ll handle this too. Whether it’s exploring new markets, switching up suppliers, or keeping extra cash flow on hand, there are always ways to stay ahead.

You can’t control trade policies, but you can control how prepared you are. Stay flexible, stay informed, and keep your business moving forward—no matter what comes next.

Need a financial safety net to help you navigate challenges? Merchant Growth offers fast, flexible financing designed for small businesses. Learn more today!

Running a small business is full of surprises...and not always the fun kind. Maybe your restaurant’s fridge decides to quit during the dinner rush. Or your construction project hits a delay, and you still have bills to pay. When cash flow gets tight, it’s stressful. You need a solution fast.

But traditional bank loans? They’re slow, complicated, and often come with requirements that small businesses can’t meet.

So, what do you do when you don’t qualify (or don’t have the time to apply and wait)? Luckily, there’s a solution that doesn’t involve long waits or piles of paperwork: a business line of credit. It can be used to cover a last-minute expense, restock your inventory, or bridge a cash flow gap.

Does that sound a little too good to be true? Don’t worry! We’ll explain everything you need to know to make it work for your business.

What Is a Business Line of Credit?

A business line of credit is like a financial backup plan for your business. You get approved for a set amount of money, but you only use it when you need it.

You can borrow as much or as little as you need (up to your limit), and you only pay interest on what you actually use. Once you repay what you’ve borrowed, that money becomes available again. It’ll be ready for the next time you need it.

It’s a bit like a credit card. The difference is that it is designed to help you with your business needs (like covering payroll, repairing equipment, or buying extra inventory).

A business line of credit gives you quick, flexible access to cash. Best of all, there’s no need to reapply every time you need funds. It’s there when you need it.

How Does a Business Line of Credit Work?

Still not sure how a business line of credit works or what the process looks like? Here’s exactly how:

1. Getting Approved and Setting a Limit

When you apply, the lender will look at your business’s revenue, credit history, and financial health to decide your credit limit.

Think of it as a cap on how much you can borrow at any time. Typically, it ranges from $5,000 to $250,000.

2. Drawing and Using Funds

Once you’re approved, you can borrow as much or as little as you need, whenever you need it, up to your limit.

As an example: If you have a $15,000 credit limit and withdraw $5,000 to cover payroll, you still have $10,000 available for other expenses.

3. Repaying and Reusing Funds

After you repay the $5,000 (plus interest), your full $15,000 becomes available again. This is what’s called revolving business credit: you can draw, repay, and reuse without reapplying.

A business line of credit gives you flexible access to funds, ensuring you're prepared for unexpected costs, emergencies, or simply for peace of mind.

How You Can Benefit from A Business Line of Credit

There are many ways a business can benefit from a business line of credit. Here are just four of the many advantages you get:

1. Better Cash Flow Management

Every business has its highs and lows, and cash flow can be unpredictable. Maybe your café needs to stock up on supplies before the holiday rush, or you’re a contractor waiting on a late payment to come through. A business line of credit helps you fill those gaps, so you can keep your operations running smoothly without any interruptions. This can save you from missing out on profits during busy times.

2. Save Money with Flexible Interest

With a line of credit, you only pay interest on what you actually borrow. For example, if you’re approved for $20,000 but only use $5,000 to cover a quick repair, you’ll only pay interest on that $5,000, not the entire limit.

This is a big advantage over traditional loans, where you’re often stuck paying interest on the full amount, even if you don’t use it all. With a business line of credit, you stay flexible and never pay more than necessary.

3. Get Funds Faster and Easier

Bank loans are known for being slow and complicated. They require piles of paperwork, perfect credit, and weeks (if not months) to get approved. A business line of credit, especially from alternative lenders like Merchant Growth, is much faster and simpler.

You can apply online, skip the mountains of forms, and get access to funds when you need them most. It’s a very simple process that saves you time and stress.

4. Flexible Financing for Any Business Need

A business line of credit is flexible. You can use it for whatever your business needs. Fix a broken fridge, restock inventory, or run a quick marketing campaign.

Unlike traditional loans, you’re not locked into using the money for one thing. Use it where it helps most. It’ll help you handle surprises or take advantage of opportunities when they arise without wasting time.

When to Use a Business Line of Credit

A business line of credit can help you cover:

- Seasonal expenses: Stock up on inventory for busy times of the year.

- Unexpected repairs: Fix that broken fridge, leaky roof, or out-of-service van.

- Payroll gaps: Cover wages during slow months or unexpected delays in client payments.

- Growth opportunities: Fund a quick marketing campaign or buy extra materials for a new contract.

That said, a line of credit isn’t ideal for long-term or big-ticket investments. For those, you’d want to consider other small business credit solutions.

Check out our term financing and e-commerce financing options to see what’s the best fit for your business.

How Does a Business Line of Credit Compare to Other Options?

What other options and alternative business loans are there and how do they stack up to a business line of credit?

- Traditional Loans: Good for larger, long-term investments, but less flexible and slower to approve.

- Credit Cards: Convenient but often come with higher interest rates and fees.

- Merchant Cash Advances: Quick access to funds but less flexible in repayment terms.

A business line of credit sits right in the middle. It’s fast, flexible, and affordable. It works for day-to-day needs and smaller expenses that pop up unexpectedly.

Common Misconceptions About Business Lines of Credit (Debunked)

If you’re like many other small business owners, some common myths might be holding you back. We’ve heard lots of the same concerns over and over again. Let’s clear those up:

“Isn’t a line of credit just like a credit card?”

Not quite. Both let you borrow as needed, but a business line of credit has some big advantages:

- It comes with higher borrowing limits, often tens of thousands of dollars.

- It’s designed specifically for business needs, like covering payroll or buying equipment, rather than everyday purchases.

“Will I need perfect credit to qualify?”

Not necessarily. While traditional banks may require excellent credit, alternative lenders like Merchant Growth have more flexible criteria. They consider your business’s overall health, such as revenue and cash flow, rather than just your credit score.

Why Should You Choose Merchant Growth for Your Business Line of Credit?

We get it: running a small business in Canada isn’t easy. Unexpected business expenses pop up, cash flow can get tight, and bank loans? They’re not always an option, especially if you don’t meet their strict criteria.

That’s why we designed our business line of credit to be exactly what small businesses need: fast, flexible, and free of unnecessary hurdles.

Merchant Growth works differently:

- Fast Approvals: No one has time to wait weeks for small business funding. Our online application process is quick and straightforward. You’ll get the funds in just 24 hours.

- No Credit Score Worries: Your credit score won’t be impacted by applying. It’s risk-free.

- Flexible Repayments: Borrow what you need, when you need it, and only pay for what you use. It’s financing that works with your cash flow, not against it.

Made for Small Businesses: Are you running a restaurant, managing a construction project, or keeping up with retail demand? Whatever struggles you face, we understand them. Our financing solutions offer flexible short-term options with terms ranging from 6 to 18 months, tailored to your business needs

Not every business fits into the bank’s mold, and that’s okay. We’re here to provide financing that works for real-world businesses, all without the stress or delays.

When your business thrives, so does your community. That’s something we’re proud to support.

Ready to Take Control of Your Cash Flow?

Merchant Growth’s business line of credit is designed to give Canadian small businesses the flexibility and support they need to handle unexpected expenses, seasonal slowdowns, or new opportunities for growth.

With our LOC, you can:

- Access funds quickly with a straightforward online application process.

- Get approved in as little as 24 hours. No waiting weeks like with traditional lenders.

- Borrow only what you need, when you need it, and repay on flexible terms that align with your cash flow.

At Merchant Growth, we make emergency business funding easy, stress-free, and completely online. Apply today and receive your funds in as little as 24 hours.

Frequently Asked Questions About Business Lines of Credit

How much can I borrow with a business line of credit?

It depends on the lender and your business’s financial health. Limits typically range from $5,000 to $250,000. Approval is usually based on factors like your revenue and creditworthiness.

How quickly can I access funds?

With alternative lenders like Merchant Growth, you can get approved and access funds in as little as 24 hours. This is great for when unexpected expenses or emergencies come up (you can’t plan for those).

Do I need collateral to secure a line of credit?

At Merchant Growth, our financing is always collateral-free. You won’t need to provide assets like equipment or real estate as backing.

However, traditional bank lines of credit often require collateral, which could include business or personal assets. This can sometimes lead to higher credit limits or lower interest rates, but it also makes the process less accessible for many small businesses.

Summary: Your Business, Backed by a Flexible Solution

A business line of credit is a smart way to keep your business running smoothly when surprises happen. It’s fast, flexible, and is there when you need it. Unlike traditional bank loans, Merchant Growth’s line of credit gets you the funds you need quickly, without the stress of piles of paperwork or long waits.

Our line of credit requires no collateral. It’s a solution that is designed for Canadian small businesses that are handling unexpected repairs, covering payroll, or seizing a growth opportunity. Keep your business moving forward with financing that works for you. Apply today and take control of your cash flow with ease!