Can Canada Survive a Trade War with the U.S.? What It Means for Small Businesses

Over the past year, the Canada–U.S. trade relationship has shifted in ways few businesses expected. What began as tariff disputes has evolved into a more complex and uncertain cross-border environment. February 1st marked one year since tariffs escalated between the two countries, and for many Canadian businesses, that year has required adaptation, recalibration, and resilience.

At a national level, Canada has not “collapsed” under trade pressure. But survival at the macroeconomic level does not automatically translate to stability for small businesses operating on tight margins. The real question isn’t just whether Canada can survive a trade war with the U.S. It’s how Canadian businesses, especially small and mid-sized ones, navigate the operational impact.

To better understand what’s happening on the ground, Merchant Growth surveyed 103 Canadian small businesses in January 2026. The results offer a clear picture: resilience exists, but it comes with cost pressure and cautious decision-making.

In this article, we’ll explain what a trade war means, why Canada is particularly exposed, what the data says about small business resilience, and what business owners can do next.

Key Takeaways

- A trade war increases costs through tariffs and retaliatory measures.

- 41% of surveyed small businesses report margin declines due to tariffs.

- Nearly half absorbed added costs instead of raising prices.

- Trade uncertainty delays investment, hiring, and expansion.

- Survival depends on adaptation, fiscal policy, and business-level cash flow management.

What Is a Trade War? (In Simple Terms)

A tariff is a tax placed on imported goods. When one country imposes tariffs, the affected country may respond with its own tariffs in retaliation. That cycle of escalating trade barriers is what defines a trade war.

The impact goes beyond the tax itself. Tariffs raise the cost of goods crossing borders, which increases input costs for manufacturers, retailers, and distributors. Over time, businesses adjust supply chains, pricing strategies, and sourcing decisions. Consumers may face higher prices, and investment decisions become more cautious.

The economic effect isn’t limited to the tariff percentage. The real cost often lies in uncertainty and unpredictability around policy shifts, negotiations, and future restrictions. That uncertainty influences hiring, capital investment, and long-term planning.

Why Is Canada So Exposed to a U.S. Trade War?

The United States is Canada’s largest trading partner, and the scale of that relationship is significant. In 2024 alone, nearly $3.6 billion (US$2.6 billion) worth of goods and services crossed the Canada–U.S. border every single day. Cross-border trade is deeply integrated across industries, including manufacturing, energy, automotive production, steel, and aluminum. Supply chains often operate seamlessly across provincial and state lines, with products and components moving back and forth multiple times before reaching consumers.

Because these industries are highly interconnected, even modest tariffs can ripple across multiple sectors. For example, an auto part manufactured in Ontario may cross the border several times before final assembly. Each tariff layer compounds cost.

The impact is also regionally uneven. Provinces with stronger exposure to manufacturing and resource exports may feel pressure more acutely than service-driven economies. This interconnected structure makes “Canada vs U.S. trade war” effects highly sector-specific.

How Will a Trade War Affect Canada?

The effects of a trade war don’t show up in just one headline number. They ripple through the economy in layered and sometimes subtle ways. While the national economy may continue functioning, individual industries, regions, and businesses can feel pressure differently depending on their exposure to cross-border trade. Understanding these channels of impact helps clarify why even targeted tariffs can create broader economic consequences.

At a high level, trade conflict affects Canada in several key ways:

- Higher input costs for imported components

- Margin compression for exporters

- Delayed investment decisions

- Consumer price sensitivity

For businesses, higher input costs are often absorbed initially to protect customer relationships and maintain market share. Many companies hesitate to raise prices immediately, especially in competitive sectors. But sustained cost pressure eventually forces difficult decisions around pricing, hiring, and expansion.

Uncertainty acts as an economic tax. Even if tariffs themselves are modest, unpredictability reduces confidence. When business owners hesitate to invest in equipment, inventory, or new hires, growth slows. The effects may not be dramatic in a single quarter, but they accumulate over time, influencing both business momentum and broader economic performance.

What the Data Says: How Canadian Small Businesses Are Responding

National economic indicators tell one story. Small businesses tell another. To understand how the trade war is affecting Canadian companies on the ground, Merchant Growth conducted its own Trade War Survey in January 2026, gathering insights from 103 small businesses across the country. The findings provide direct visibility into how owners are adjusting operations, managing margins, and planning for the months ahead.

The data reveals not panic, but pressure. And that pressure is shaping real business decisions.

Key findings include:

- 57% scaled back U.S.-related activity

- 14% cut ties with U.S. activity entirely

- 41% reported profit margin decreases

- 32% spent $5,000–$25,000 in added trade costs

- 9% spent $26,000–$100,000

- 48% did not pass on increased costs to customers

- 43% plan to raise prices in the next six months

The pattern is clear: many businesses are absorbing higher costs to protect customer demand. Nearly half chose not to immediately pass tariff-related increases on to buyers. While this strategy preserves relationships and competitiveness in the short term, it places sustained pressure on profitability.

Operational adjustments further illustrate how businesses are adapting:

- 55% are cutting discretionary spending

- 45% plan to take on additional financing

- 29% are negotiating supplier terms

- 25% are reducing inventory

- 53% report headcount has remained steady, reflecting cautious resilience

Taken together, the findings suggest something important. Canada may appear stable at the macro level, but small businesses are making deliberate trade-offs behind the scenes, protecting demand, preserving jobs, and carefully managing cash flow in the face of rising uncertainty.

Why Didn’t 2025 Tariffs “Break” Canada?

Despite the disruption, Canada’s economy has not collapsed under tariff pressure. Several factors contributed to resilience.

CUSMA (formerly USMCA) protections limited full exposure in certain sectors. Businesses adapted supply chains and diversified sourcing. Currency movements partially offset tariff costs for exporters. Consumer “buy local” behaviour provided some support to domestic producers.

Additionally, federal fiscal capacity remains a buffer. Targeted support measures and government programs can help stabilize affected industries.

The outcome is nuanced: Canada didn’t break, but it didn’t escape impact either. The pressure has been uneven, concentrated in trade-dependent sectors rather than across the entire economy.

Can Canadian Federal Finances Withstand a Prolonged Trade War?

Fiscal resilience matters in prolonged trade disputes. In simple terms, fiscal resilience refers to the federal government’s ability to respond to economic stress through spending, tax relief, or targeted support programs without destabilizing public finances. During trade disruptions, that can mean sector-specific aid, temporary tax measures, wage subsidies, or credit programs designed to help affected industries stay afloat.

The federal government’s capacity to deploy targeted stimulus, meaning temporary spending or financial support intended to stabilize the economy, plays an important stabilizing role. If exporters, manufacturers, or regional industries face sudden tariff pressure, timely government support can cushion the immediate impact and prevent broader job losses or business closures.

However, sustained trade conflict would test fiscal limits. Government support is funded through public revenues and borrowing, and those resources are not unlimited. A short-term dispute may be manageable, but a prolonged or escalating trade war could strain budgets, increase deficits, and reduce the government’s flexibility to respond to future shocks.

Fiscal policy acts as a stabilizer, not a shield. It can soften the blow of external disruption, but it cannot eliminate structural exposure to cross-border trade risk. For small businesses, confidence in government stability and policy support influences real decisions around hiring, capital investment, and expansion. When that confidence weakens, businesses often shift into preservation mode rather than growth mode

A Structural Shift, Not Just a Short-Term Dispute

While it’s tempting to frame trade tensions as a temporary flare-up, many analysts suggest something more fundamental may be unfolding. The current environment may represent a structural shift in global trade dynamics rather than a one-off policy dispute. If that’s the case, the implications extend beyond tariffs and into how Canada positions itself economically over the long term.

Canada’s deep reliance on a single trading partner has historically delivered efficiency and scale. However, concentration also creates vulnerability. Diversifying export markets, strengthening domestic supply chains, and reducing dependency on specific cross-border inputs could help mitigate future exposure. These adjustments take time, but they build resilience into the system.

There is also a strategic opportunity embedded in this shift. Canada’s role in critical minerals, energy development, advanced manufacturing, and reshoring initiatives could become more central in a more fragmented global trade environment. If global supply chains become more regionalized, Canada may benefit from its resource base, political stability, and proximity to major markets.

Trade tensions may therefore signal a longer-term recalibration of global commerce. Businesses that recognize this possibility and plan for continued volatility rather than a quick return to stability may be better positioned to adapt, diversify, and compete over time.

How Small Businesses Can Build Resilience During a Trade War

National policy decisions and trade negotiations unfold over months, sometimes years. Small businesses don’t have that luxury. When costs rise or uncertainty increases, owners need to respond in real time. The ability to adapt quickly often determines whether pressure becomes temporary or structural.

While macro policy evolves slowly, small businesses can act immediately. Practical steps include:

- Diversifying suppliers where feasible

- Reviewing pricing strategy and margin buffers

- Negotiating supplier payment terms

- Improving working capital management

- Using financing strategically to smooth volatility

The Merchant Growth survey shows that many businesses are already taking these steps. With 45% turning to financing and 29% renegotiating supplier terms, the focus is clearly on preserving cash flow and maintaining flexibility.

At the small business level, resilience often comes down to liquidity. When margins compress, even profitable companies can feel strain. Strong cash flow management provides breathing room, allowing businesses to make strategic decisions rather than reactive ones.

How Long Will It Take the Canadian Economy to Recover?

There isn’t a fixed timeline for economic recovery in a trade dispute. The pace of improvement depends largely on policy stability, the direction of trade negotiations, and how quickly businesses adapt to shifting conditions.

If negotiations stabilize and tariff uncertainty eases, investment confidence could return relatively quickly. Businesses tend to respond fast when predictability improves. However, if tensions persist or escalate, the adjustment period may stretch longer, requiring continued cost discipline and strategic flexibility.

For small businesses, the priority isn’t predicting exactly when macroeconomic recovery will arrive. It’s building operational resilience, the kind that allows growth and stability even when external conditions remain uncertain.

From Surviving a Trade War to Strengthening Your Business

Uncertainty is increasingly part of doing business. Survival is not just about national GDP resilience, it is about small business stability.

The Merchant Growth survey highlights real operational pressure: margin compression, cautious hiring, and increased financing demand. These are not signs of collapse, but they do signal strain.

Managing cash flow under pressure, absorbing cost shocks, and financing growth strategically are essential during periods of volatility. Financing should create flexibility, not risk.

Trade wars create uncertainty. Resilient businesses create options.

If rising costs or cross-border disruptions are affecting your cash flow, talk to Merchant Growth about financing solutions built to support Canadian small businesses through change.

What Is the Break-Even Point? A Simple Guide to Break-Even Analysis

Every business eventually reaches a moment when its revenue finally covers its costs. Before that point, the company is effectively investing in its own operations, spending money on rent, salaries, materials, and marketing while sales gradually catch up. Once revenue equals expenses, the business has reached what’s known as the break-even point.

For many entrepreneurs, understanding when this moment will happen is one of the most important parts of financial planning. Knowing your break-even point helps answer critical questions:

- How much do you need to sell to cover your costs?

- Is your pricing sustainable?

- How long might it take before a new product or business idea becomes profitable?

This is where break-even analysis becomes useful. By examining the relationship between costs, pricing, and sales volume, break-even analysis helps business owners estimate when their company will begin generating profit. Whether you're launching a startup, introducing a new product, or evaluating the performance of an existing business, understanding this calculation can provide valuable insight into your financial strategy.

Key Takeaways

- The break-even point is when total revenue equals total costs.

- Break-even analysis shows how much a business needs to sell before it becomes profitable.

- The calculation depends on fixed costs, variable costs, and contribution margin.

- Lower costs or higher prices reduce the break-even threshold.

- Break-even analysis helps businesses plan pricing, sales targets, and profitability.

- It works best when combined with broader financial planning tools.

What Is the Break-Even Point?

The break-even point is when a business’s total revenue equals its total costs. At this stage, the company is no longer losing money, but it has not yet begun generating profit either. Every dollar earned beyond this point contributes directly to profit because the initial operating costs have already been covered.

Reaching the break-even point is an important milestone for any business. It represents the moment when operations begin to sustain themselves financially rather than relying on startup capital or borrowed funds. For new businesses, understanding how long it may take to reach this stage can help set realistic expectations for growth.

The break-even point also provides useful insight for established companies. When launching new products, adjusting pricing, or expanding operations, businesses often calculate a new break-even point to understand how much sales volume will be required to support those changes.

Break-Even Point vs Break-Even Analysis

Although the terms are often used together, the break-even point and break-even analysis refer to different concepts.

The break-even point is the specific level of sales where revenue and costs are equal. It is a single figure that represents the threshold between operating at a loss and becoming profitable.

Break-even analysis, on the other hand, is the process used to calculate that threshold. This analysis examines how costs, pricing, and sales volume interact. By adjusting these variables, businesses can explore different scenarios and better understand how changes might affect profitability.

For example, increasing prices or reducing costs will lower the break-even point. On the other hand, higher operating expenses or lower margins will push it further away, requiring greater sales volume before profits begin.

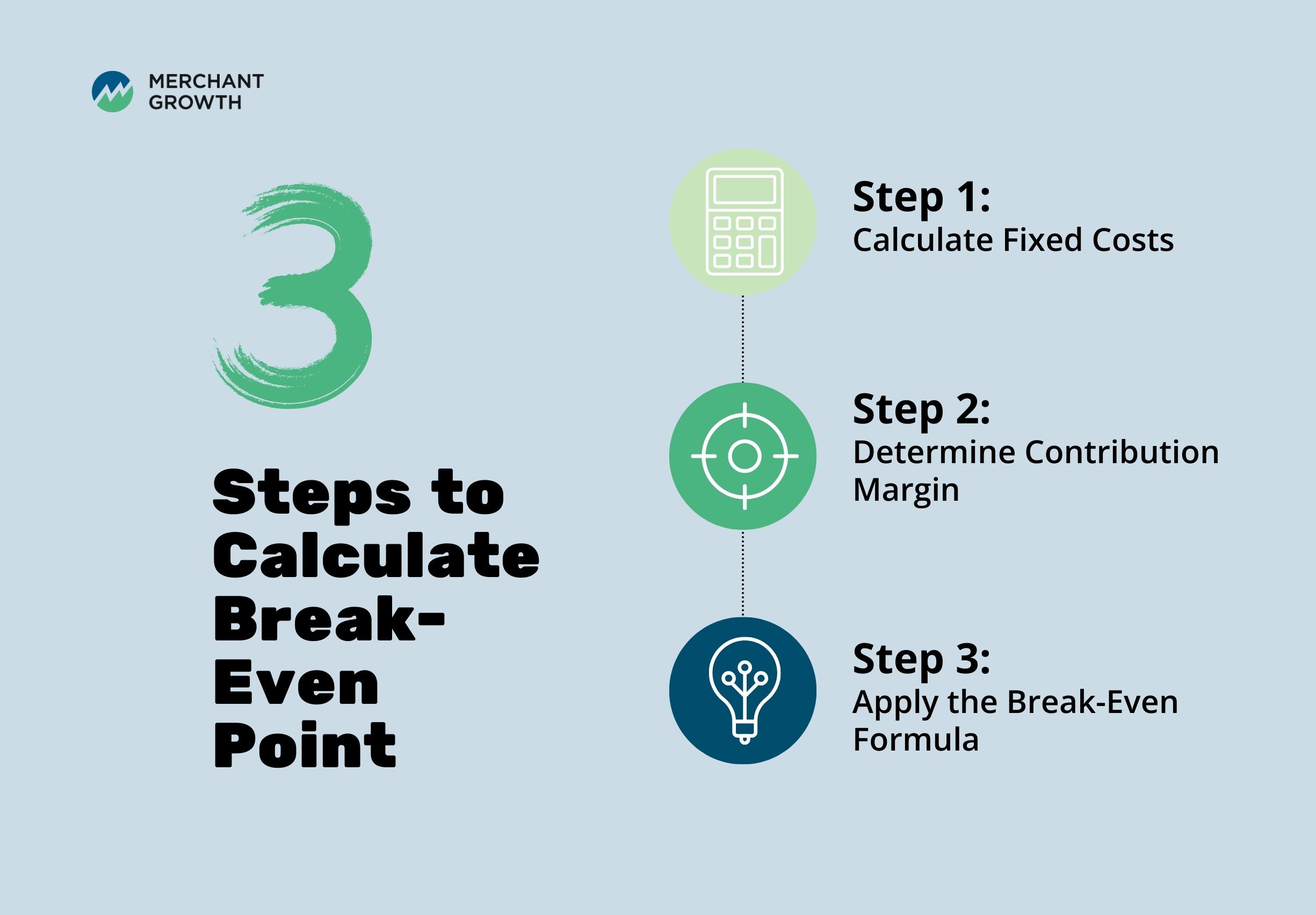

How to Calculate the Break-Even Point in 3 Steps

Calculating the break-even point may sound complicated at first, but the process is actually quite straightforward when you break it down into a few steps. The goal is to figure out how much a business needs to sell before it covers all of its operating costs. Once you know this number, it becomes much easier to set realistic sales targets and understand how close your business is to becoming profitable.

Step 1: Calculate Fixed Costs

The first step is identifying your fixed costs. These are expenses that stay the same regardless of how much your business sells. Whether you sell one product or one thousand, these costs still need to be paid each month.

Typical fixed costs include:

- Rent or mortgage payments

- Salaries and wages

- Insurance

- Software subscriptions

- Utilities

Because fixed costs remain relatively stable, they provide the starting point for calculating your break-even point. Understanding these expenses clearly helps you determine how much revenue your business must generate before it begins making a profit.

Step 2: Determine Contribution Margin

Next, you’ll need to calculate your contribution margin. This number shows how much money each sale contributes toward covering fixed costs after the cost of producing the product has been accounted for.

The formula looks like this:

Contribution Margin = Price per Unit – Variable Cost per Unit

For example, if a product sells for $100 and costs $60 to produce, the contribution margin is $40. That means every sale contributes $40 toward covering fixed expenses such as rent, salaries, and other operating costs.

Step 3: Apply the Break-Even Formula

Once you know your fixed costs and contribution margin, calculating the break-even point becomes simple. You can use the following formula:

Break-Even Point (Units) = Fixed Costs ÷ Contribution Margin

This calculation shows how many units a business needs to sell before it covers all of its costs. Once sales pass that number, the business begins generating profit because the fixed costs have already been paid.

Once these numbers are clear, calculating your break-even point becomes much easier. By understanding how fixed costs, variable costs, and contribution margin work together, business owners can see how pricing decisions, cost changes, or shifts in sales volume will affect profitability. The next step is to take a closer look at these key components and how they influence the break-even calculation.

The Key Components of Break-Even Analysis

Break-even analysis is built on a few core financial variables that determine how quickly a business can move from covering its costs to generating profit. These variables help business owners understand how pricing, production costs, and operating expenses interact with one another. When these components are clearly defined, it becomes much easier to estimate how much revenue is required to sustain the business.

Before applying the break-even formula, it is important to understand the three key elements that drive the calculation: fixed costs, variable costs, and contribution margin. Each plays a different role in determining how much a business must sell to cover its expenses.

Fixed Costs

Fixed costs are expenses that remain the same regardless of how much a business produces or sells. These costs must be paid regularly, even during periods when sales slow down or fluctuate. Because they do not change with production levels, fixed costs often represent the baseline amount a business must cover before it can begin earning a profit.

Common examples of fixed costs include rent, salaries, insurance, and software subscriptions. These ongoing expenses form the foundation of a break-even calculation because they represent the minimum financial commitment required to keep the business operating.

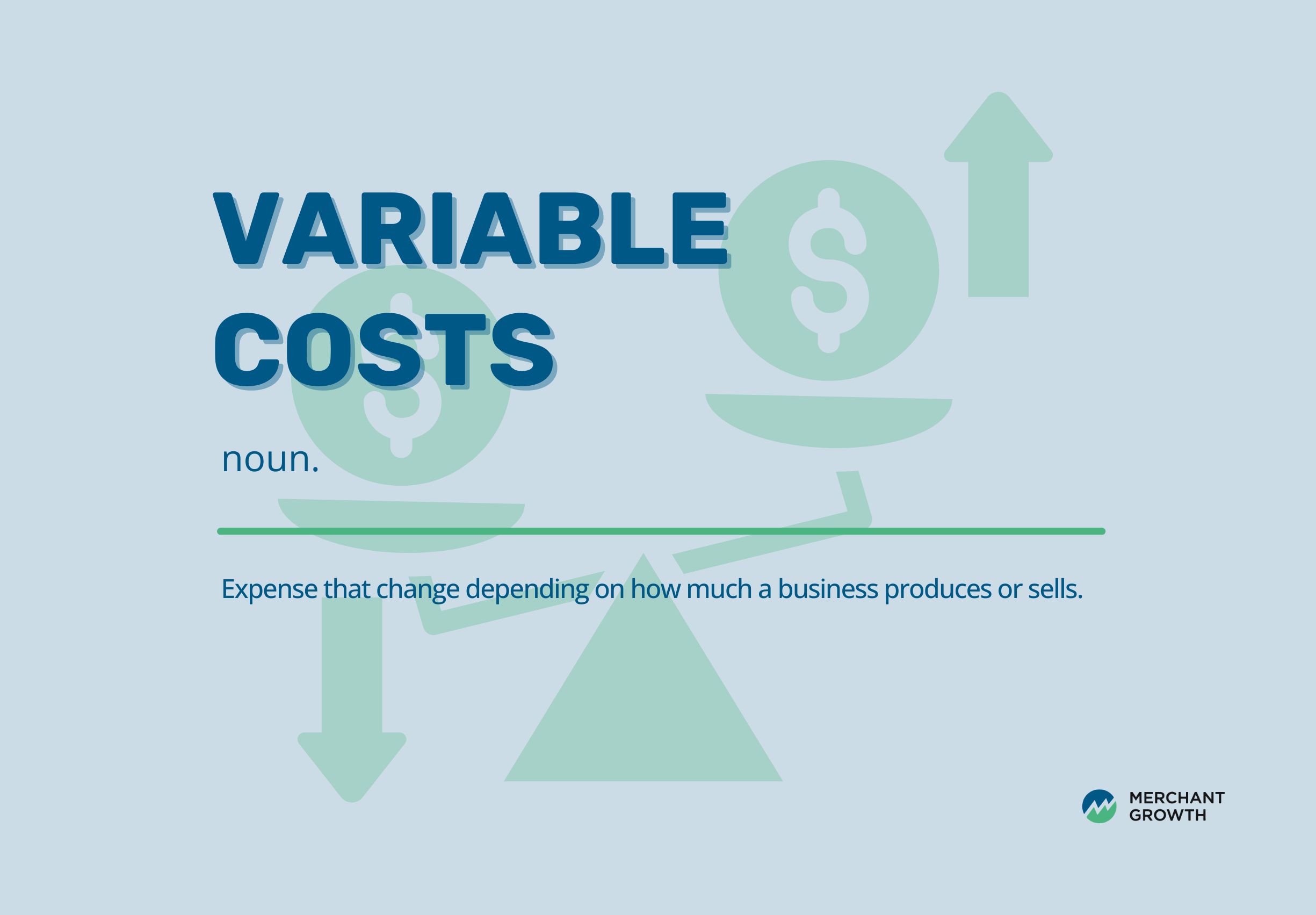

Variable Costs

Variable costs, as the name suggests, change depending on how much a business produces or sells. When production increases, these costs rise accordingly, and when production slows, they decrease. Because they are tied directly to sales activity, variable costs are closely linked to a company’s revenue generation.

Examples of variable costs include raw materials, packaging, shipping, and sales commissions. Understanding these costs is important because they affect how much profit remains from each sale after production expenses are covered.

Contribution Margin

The contribution margin represents the portion of revenue from each sale that helps cover fixed costs. It is calculated by subtracting the variable cost per unit from the selling price of the product or service. Once fixed costs have been fully covered, any remaining contribution margin becomes profit.

By understanding contribution margin, businesses can see how changes in pricing or production costs may influence their path to profitability. Even small adjustments in margins can significantly affect how quickly a company reaches its break-even point.

Break-Even Point Formula (Units)

Once the key components are clear, the break-even point can be calculated using a straightforward formula. Many businesses begin by measuring break-even in terms of units sold, which makes it easier to connect the calculation directly to sales activity.

The formula is:

Break-Even Point (Units) = Fixed Costs ÷ (Price per Unit – Variable Cost per Unit)

This equation highlights the relationship between costs, pricing, and sales volume. If operating costs increase or prices decrease, the number of units required to break even will rise. On the other hand, improving margins through pricing adjustments or cost reductions can lower the break-even threshold and help businesses reach profitability sooner.

Break-Even Point Formula (Sales Dollars)

While calculating break-even in units works well for product-based businesses, some companies prefer to measure break-even in terms of total revenue. This approach is particularly useful for service-based businesses that may not sell standardized products.

The formula for calculating break-even in revenue terms is:

Break-Even Sales = Fixed Costs ÷ Contribution Margin Ratio

Instead of focusing on the number of units sold, this calculation shows how much total revenue must be generated before a business begins producing profit. For service businesses, consultants, and subscription-based companies, this revenue-based perspective can provide a clearer picture of financial performance.

Example of Break-Even Analysis

To better understand how break-even analysis works in practice, it helps to walk through a simple example. Consider a business with the following financial structure:

- Fixed costs: $50,000

- Price per unit: $100

- Variable cost per unit: $60

First, calculate the contribution margin:

$100 – $60 = $40

Next, divide the fixed costs by the contribution margin:

$50,000 ÷ $40 = 1,250 units

This means the business must sell 1,250 units before it begins generating profit. Once that threshold has been reached, each additional sale contributes directly to the company’s bottom line.

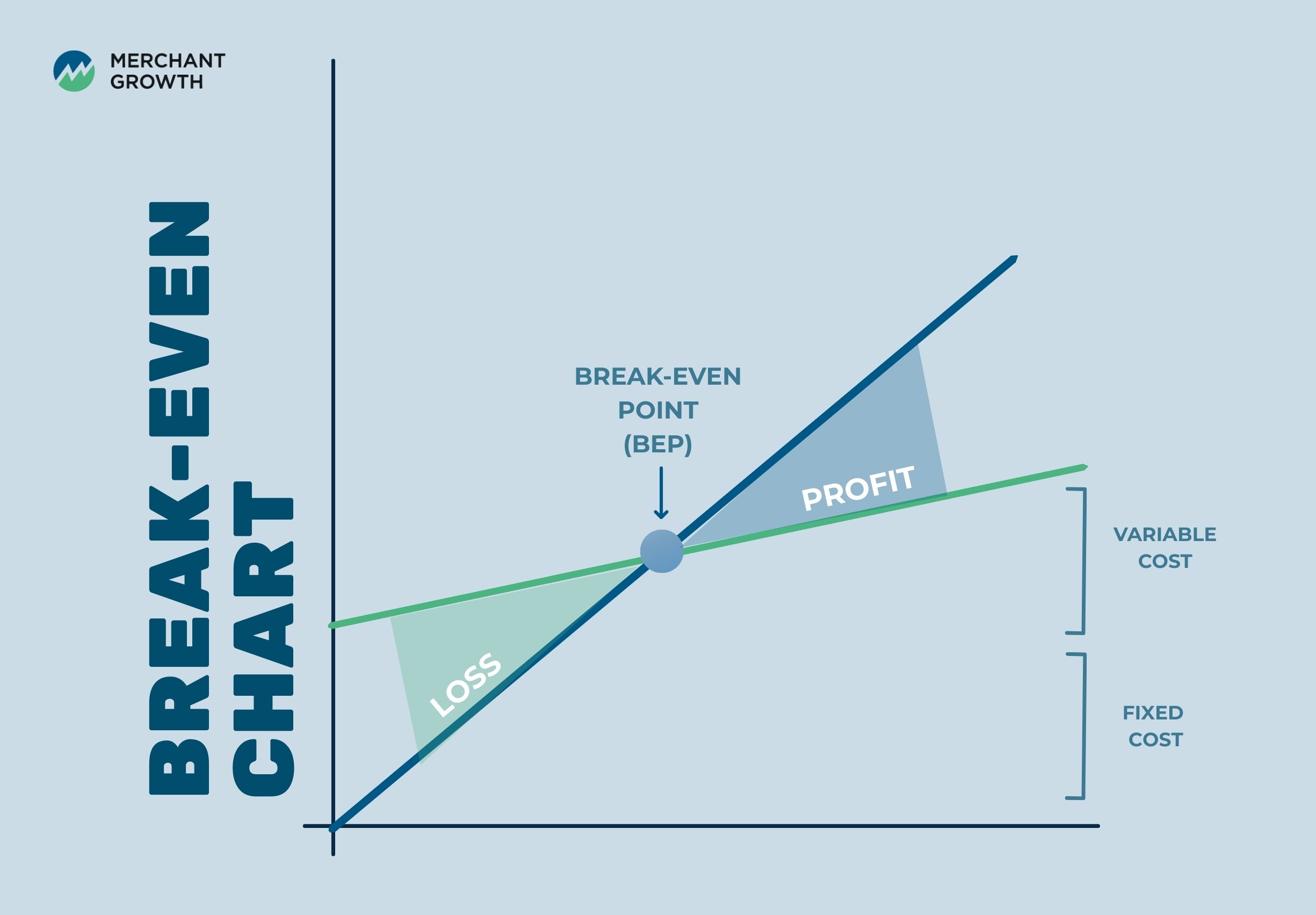

Break-Even Chart Explained

Break-even analysis is often easier to understand when visualized using a chart. This chart illustrates how revenue and costs change as sales volume increases.

In a typical break-even chart, the horizontal axis represents sales volume, while the vertical axis represents both revenue and costs. Fixed costs appear as a horizontal line because they remain constant regardless of sales activity. Meanwhile, total costs gradually increase as production grows due to rising variable expenses.

The revenue line rises alongside sales volume. The point where the revenue line intersects with the total cost line represents the break-even point. This visual representation makes it easier for business owners to see how adjustments in pricing, cost structure, or production levels can influence profitability.

Why Break-Even Analysis Matters for Business Owners

Break-even analysis is more than just a financial calculation. For many business owners, it becomes a valuable planning tool that helps guide important decisions about pricing, growth, and cost management.

By understanding the break-even point, companies can set realistic sales targets and evaluate whether a business idea is financially viable. It also provides insight into how pricing strategies and operational costs influence profitability.

For established businesses, break-even analysis helps assess the potential impact of new initiatives such as launching products, expanding operations, or entering new markets. Rather than relying on guesswork, business owners can use this analysis to make more informed decisions based on financial data.

Is a High Break-Even Point Good?

A higher break-even point means a business must generate more sales before it begins earning profit. In some cases, this may indicate higher financial risk, especially if revenue fluctuates or market demand is uncertain.

However, a high break-even point is not always a negative sign. Certain industries require substantial upfront investments in equipment, technology, or infrastructure. Businesses operating in these sectors often expect higher break-even thresholds because their fixed costs are larger.

Ultimately, the key question is whether the required sales volume is realistic. If demand is strong and the business model is sustainable, a higher break-even point may simply reflect the scale of the operation.

Common Break-Even Analysis Mistakes

Although break-even analysis is a useful tool, it can produce misleading conclusions if important factors are overlooked. Many mistakes occur when businesses rely on incomplete cost estimates or outdated financial assumptions.

Common errors include:

- Ignoring variable costs, which can lead to overstating profitability.

- Underestimating operating expenses, especially smaller recurring costs that add up over time.

- Assuming demand is guaranteed, even though market conditions can change.

- Failing to update calculations when costs, pricing, or production levels shift.

Regularly reviewing and updating break-even calculations helps ensure they remain accurate as the business grows and evolves.

The Limitations of Break-Even Analysis

While break-even analysis provides valuable insights, it is not a complete financial forecasting tool. The calculation assumes that prices, costs, and sales patterns remain relatively stable, which may not always reflect real-world conditions.

External factors such as changes in customer demand, economic trends, or competitive pressures can influence profitability in ways that break-even analysis alone cannot predict. For this reason, businesses often combine break-even analysis with other financial planning tools.

Budgeting, forecasting, and market analysis can provide additional context that helps business owners understand how their financial strategies may perform under different circumstances.

From Break-Even to Profitability: Planning the Next Stage of Growth

Reaching the break-even point is an important milestone, but it is only the beginning of a company’s financial journey. Once a business has covered its costs, the focus shifts toward sustaining profitability and building long-term growth.

At this stage, many companies begin investing in expansion opportunities such as hiring new staff, increasing marketing efforts, or purchasing additional inventory. These initiatives often require upfront capital before the resulting revenue is realized.

Merchant Growth supports Canadian businesses by providing flexible financing solutions designed to help companies move beyond break-even and continue growing. Access to working capital can help businesses manage cash flow, invest in new opportunities, and scale operations with greater confidence.

Move Beyond Break-Even and Grow Your Business

Understanding your break-even point is an important step toward building a sustainable business. When you know how much revenue is required to cover your costs, it becomes easier to set realistic goals and make informed financial decisions.

Merchant Growth provides flexible funding solutions designed to help Canadian small businesses manage cash flow, invest in growth, and scale with confidence. Whether you are expanding operations, launching new products, or strengthening your financial foundation, the right financing can help support your next stage of growth.

Explore Merchant Growth financing solutions to move beyond break-even and build a stronger future for your business.

How to Solve Cash Flow Problems Without Shutting Down Your Business

Cash flow problems rarely start with a dramatic moment. More often, they creep in quietly, an invoice that takes longer to get paid, an unexpected expense, or a few slow weeks of sales. Suddenly, a business that looks healthy on paper is struggling to cover payroll, pay suppliers, or keep up with everyday expenses. Even profitable companies can run into serious trouble when there simply isn’t enough cash available at the right time.

The good news is that cash flow issues are usually manageable when they are identified early and addressed with the right strategies. By understanding the causes, recognizing the warning signs, and taking practical steps to stabilize finances, businesses can regain control without shutting down operations.

In the sections ahead, we’ll break down what cash flow problems actually look like in a business, why they tend to happen, and what you can do to fix them. We’ll also look at how to identify the type of cash flow challenge you’re facing so you can take practical steps to stabilize your finances and keep your business moving forward.

Key Takeaways

- Cash flow problems occur when a business doesn’t have enough available cash to cover expenses.

- Late payments, high operating costs, and rapid growth are common triggers.

- Identifying the type of cash flow problem helps determine the best solution.

- Accelerating payments and controlling expenses can improve liquidity quickly.

- Long-term cash flow management and forecasting help prevent future issues.

What Are Cash Flow Problems?

Cash flow problems occur when a business does not have enough available cash to meet its immediate financial obligations. This situation can arise even if the company is technically profitable. For example, a business might have strong sales and outstanding invoices, but if customers haven’t paid yet, there may not be enough cash available to cover payroll, rent, or supplier payments.

The root of most cash flow issues is timing. Businesses often incur expenses before they receive payment for their products or services. When that timing gap becomes too large, financial pressure builds quickly. Over time, persistent cash shortages can disrupt operations, strain relationships with suppliers, and limit the company’s ability to invest in growth.

Understanding what cash flow problems look like is the first step toward solving them. Once business owners recognize the patterns that cause these challenges, they can begin implementing strategies to stabilize their finances.

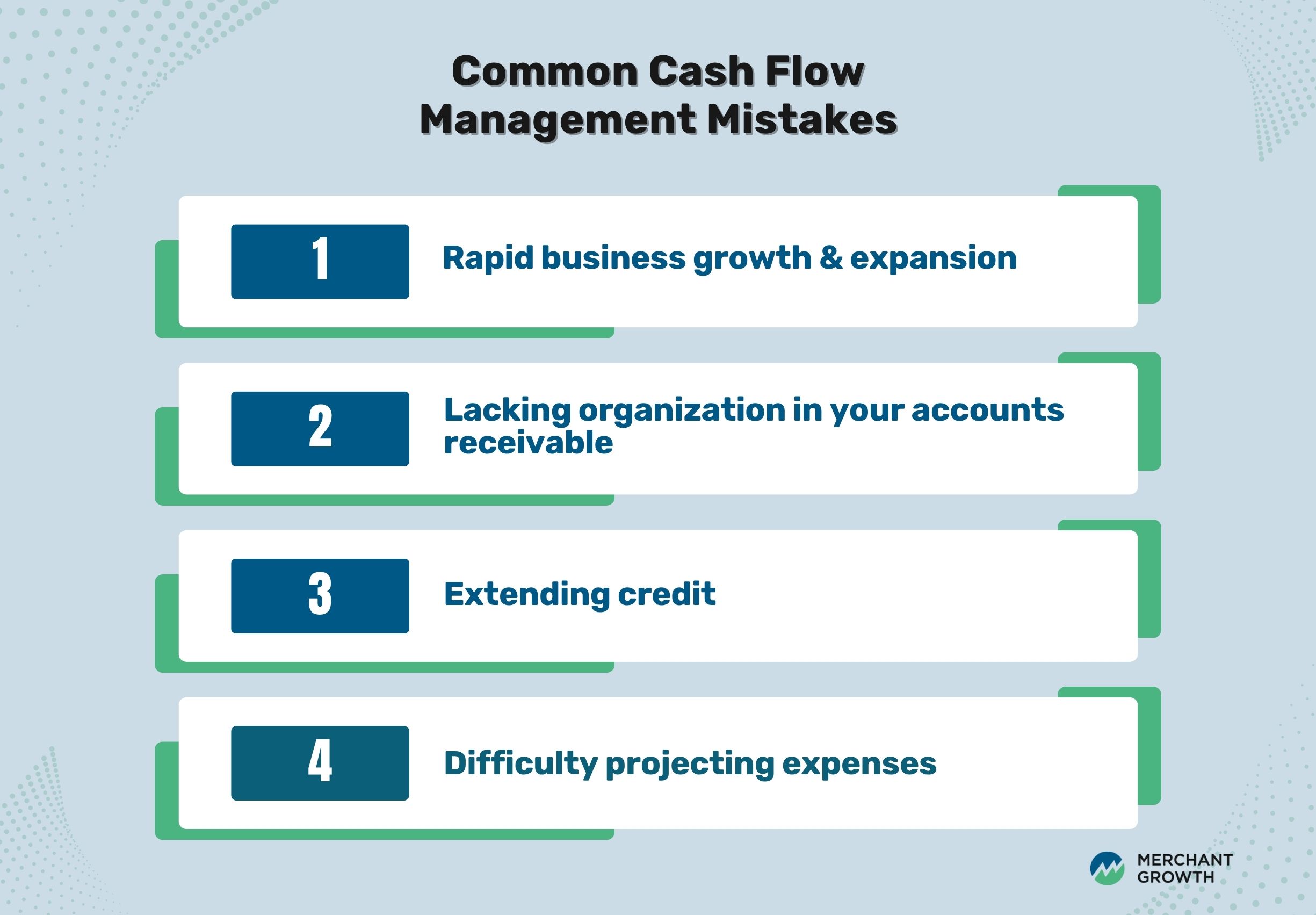

What Causes Cash Flow Problems in a Business?

To understand what’s creating cash flow pressure, it helps to look at two areas of the business. Some problems are operational, meaning they arise from everyday activities like invoicing customers, managing inventory, or paying routine expenses. Others are more strategic and relate to decisions around pricing, growth, or financial planning. Identifying which category a challenge falls into can make it much easier to address the root cause.

Operational Causes

One of the most common causes of cash flow problems is slow-paying customers. When invoices remain unpaid for long periods, businesses may struggle to cover their expenses even if they have strong sales. Weak invoicing processes or inconsistent follow-ups can make this situation worse by allowing overdue payments to accumulate.

Inventory management can also create cash flow pressure. When businesses purchase more inventory than they need, a large portion of their cash becomes tied up in unsold products. At the same time, high fixed expenses, such as payroll, rent, and software subscriptions, can quickly drain available cash during slower periods.

Strategic Causes Businesses Often Miss

Some causes of cash flow problems are less obvious. Pricing strategies, for example, can play a major role. If prices are too low or margins are too thin, a business may struggle to generate enough cash from each sale to cover operating costs.

Rapid growth can also strain working capital. Expanding operations often requires spending money on inventory, hiring, and marketing before new revenue arrives. Similarly, offering long payment terms to customers shifts the financing burden onto the business itself. Without proper forecasting, these decisions can create financial pressure even in otherwise successful companies.

In many cases, more than one of these factors may be affecting a business at the same time. That’s why it’s important not only to understand the possible causes of cash flow problems, but also to determine the type of cash flow challenge you’re dealing with. Identifying whether the issue is temporary, structural, or tied to growth can make it much easier to choose the right solution.

Diagnose the Type of Cash Flow Problem You're Facing

While these causes can affect businesses in different ways, the impact they have on cash flow isn’t always the same. In some cases the pressure is temporary and tied to timing issues, while in others it reflects deeper financial imbalances or rapid growth. Understanding how the problem is showing up in your business can help clarify what kind of solution is needed.

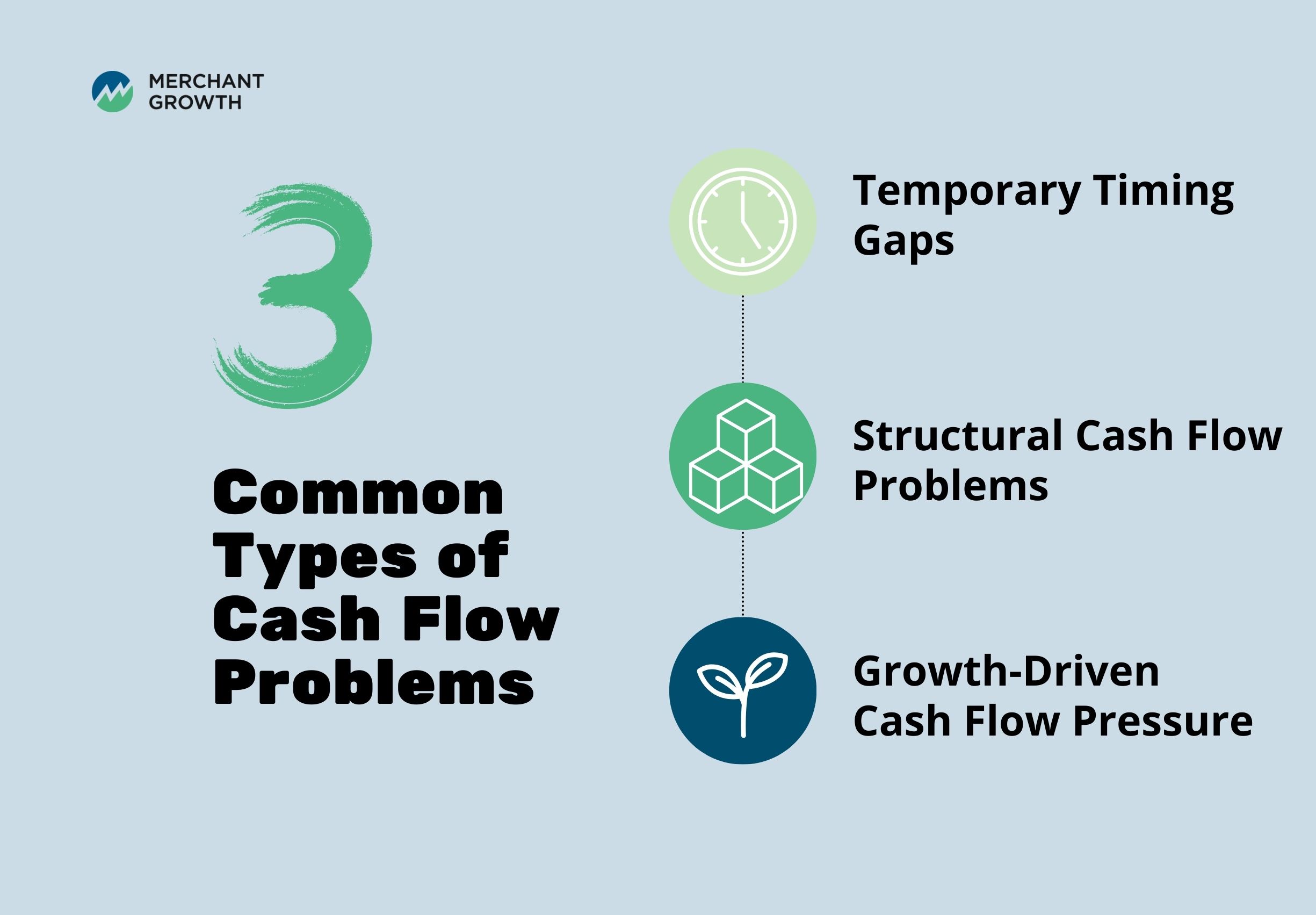

Temporary Timing Gaps

A temporary timing gap occurs when revenue is coming in, but expenses arrive sooner than expected. This is common when customers take longer to pay invoices or when sales fluctuate seasonally. In these situations, the business may simply need better payment terms or improved collections processes.

Structural Cash Flow Problems

A structural cash flow problem is more serious. In this case, operating expenses consistently exceed incoming cash. This may be caused by high overhead costs, poor pricing strategies, or inefficient operations. Solving this type of problem usually requires adjusting the underlying business model.

Growth-Driven Cash Flow Pressure

Some companies experience growth-driven cash flow pressure. Rapid expansion can require significant upfront investment before revenue increases. Purchasing inventory, hiring staff, or launching marketing campaigns all require capital. Without careful planning, even a growing business can experience cash shortages during periods of expansion.

Signs Your Business Has a Cash Flow Problem

Many businesses overlook early warning signs until the situation becomes urgent. Recognizing these signals can help prevent larger financial challenges and give business owners time to take corrective action before the problem escalates.

Common indicators of cash flow problems include:

- Difficulty paying suppliers on time

- Increasing reliance on credit or short-term borrowing to cover routine expenses

- Delaying payroll or other operational payments

- Postponing investments in equipment, marketing, or hiring

- Reducing inventory purchases due to limited cash

- Constantly reacting to short-term financial pressures instead of planning ahead

These warning signs often appear gradually, which is why they are easy to overlook at first. Paying attention to them as they come up can help businesses address cash flow challenges before they begin to disrupt day-to-day operations.

A 30-Day Plan to Stabilize Cash Flow

When a business starts running into cash flow challenges, taking a structured approach can help bring finances back under control. Instead of reacting to problems as they arise, it helps to focus on a short-term plan that prioritizes protecting available cash, bringing in revenue faster, and managing outgoing expenses. The following four-week framework outlines practical steps businesses can take to assess their financial situation, improve liquidity, and begin rebuilding a more stable cash position.

Week 1: Identify Immediate Cash Risks

Start by reviewing all outstanding invoices and identifying which payments are overdue. At the same time, prioritize essential expenses such as payroll, rent, and supplier payments. During this stage, it is also important to pause any non-essential spending so that available cash can be directed toward critical obligations.

Week 2: Accelerate Cash Inflows

Once immediate risks are identified, focus on bringing cash into the business faster. Contact customers with overdue invoices and establish clear payment expectations. Some businesses may offer small discounts for early payment or require deposits for new projects to improve cash flow timing.

Week 3: Reduce Cash Outflows

The next step is to control spending. Negotiating payment terms with suppliers can help align expenses with incoming revenue. Businesses should also review recurring expenses to determine whether any subscriptions, services, or discretionary purchases can be reduced or postponed.

Week 4: Build a Short-Term Cash Buffer

In the final stage, businesses should begin strengthening their financial resilience. Updating cash flow forecasts can help identify upcoming financial risks. Exploring short-term financing options or establishing a minimum cash reserve can also provide stability while longer-term improvements take effect.

Immediate Actions to Improve Cash Coming In

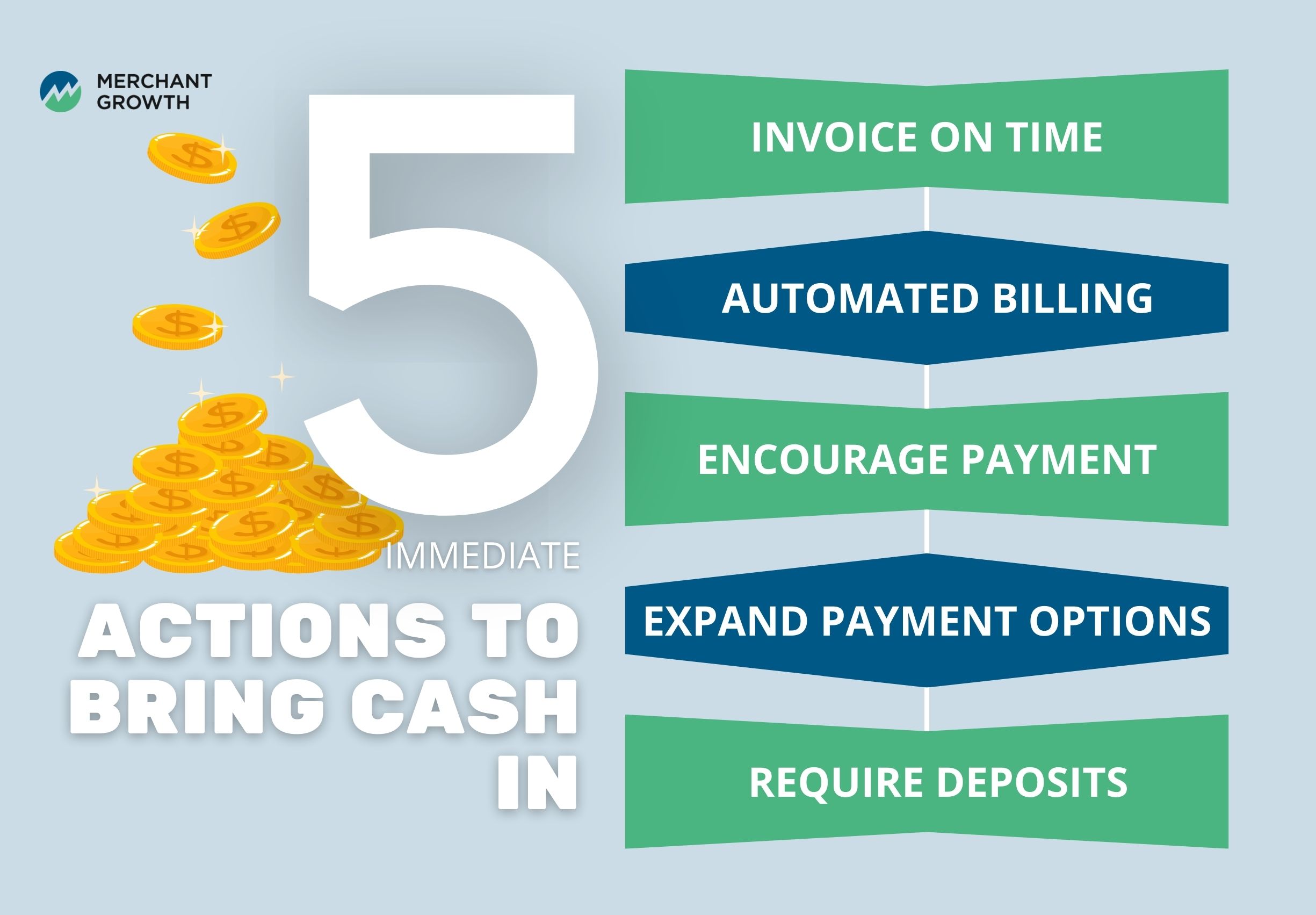

Several operational adjustments can improve cash flow relatively quickly. Many of these changes focus on accelerating incoming payments and improving the way money moves through the business. By tightening invoicing processes and making it easier for customers to pay, businesses can often shorten payment cycles and reduce delays. Small adjustments in how payments are requested and collected can make a noticeable difference in how quickly cash comes in.

Practical steps that can help improve cash flow include:

- Send invoices immediately after work is completed. Prompt invoicing reduces delays and ensures customers receive payment requests as soon as possible.

- Use automated billing systems. Automation can streamline invoicing and help ensure invoices are sent consistently and on time.

- Encourage faster payments. Offering small discounts for early payment can motivate customers to settle invoices sooner.

- Expand payment options. Accepting credit cards or online payment platforms can make it easier for customers to pay promptly.

- Require deposits or milestone payments for larger projects. Collecting partial payments upfront helps cover initial costs before work is completed.

Strategies to Reduce Cash Outflows

While increasing revenue is important, managing expenses is equally critical for maintaining healthy cash flow. Businesses can improve financial stability by carefully controlling how and when money leaves the company. Reviewing spending patterns and adjusting payment terms can create more flexibility and help align outgoing expenses with incoming revenue. Even small changes in how costs are managed can make a meaningful difference in preserving available cash.

Ways to reduce cash outflows include:

- Negotiate longer payment terms with suppliers. Extended payment terms can help align expenses more closely with incoming revenue.

- Review and reduce non-essential spending. Evaluating discretionary expenses may reveal opportunities to cut costs without affecting core operations.

- Manage inventory levels carefully. Excess inventory ties up valuable working capital that could otherwise support daily operations.

- Delay non-critical purchases or investments. Postponing equipment upgrades or large purchases can help preserve cash during tighter periods.

Manage Your Cash Flow More Effectively

Managing cash flow effectively requires consistent attention rather than a one-time fix. Businesses that regularly monitor their finances are better able to spot potential issues early and take action before they become larger problems. Having a clear view of how money is moving in and out of the business allows owners to make more informed decisions about spending, investments, and future growth.

One of the most useful tools for maintaining control over cash flow is a forecast. By estimating future cash inflows and outflows, businesses can anticipate potential shortfalls and plan for upcoming expenses. Regularly reviewing financial reports can also reveal patterns in revenue and spending, helping business owners identify trends that may affect liquidity over time.

Preparation is another important part of strong cash flow management. Building a cash reserve can provide a financial cushion during slower periods or when unexpected expenses arise. Even a modest buffer can help businesses navigate temporary challenges without disrupting day-to-day operations. Modern accounting software and financial tools can further support this process by providing real-time insights that make it easier to track financial performance and plan ahead.

When to Consider Financing to Solve Cash Flow Problems

Even when businesses take the right steps to improve their cash flow, those changes don’t always produce results immediately. Adjusting payment terms, improving collections, or reducing expenses can take time to fully affect the flow of money through the business. In the meantime, companies still need to cover everyday costs such as payroll, supplier payments, and inventory purchases.

This is where access to additional working capital can play an important role. Financing can help businesses bridge temporary gaps in cash flow while they work on strengthening their financial processes. It may be used to cover short-term operating expenses, purchase inventory ahead of demand, or manage fluctuations in seasonal revenue.

When used thoughtfully, financing gives businesses the flexibility to keep operations running smoothly while longer-term improvements take effect. Instead of constantly reacting to short-term cash shortages, owners can focus on improving their processes, serving customers, and continuing to grow the business.

Preventing Future Cash Flow Problems

Solving cash flow problems is only part of the process. Preventing them from recurring requires consistent financial planning and ongoing monitoring. Businesses that regularly review their financial position are better able to anticipate potential challenges and make adjustments before they become serious disruptions.

Maintain a Reliable Cash Flow Forecast

Maintaining an accurate cash flow forecast allows businesses to anticipate potential shortfalls before they occur. By projecting future inflows and outflows, owners can identify periods where cash may become tight and plan accordingly. Regularly updating these forecasts also helps businesses adjust spending and investment decisions as financial conditions change.

Review Payment Terms and Expenses Regularly

Payment terms and spending patterns can have a significant impact on cash flow stability. Reviewing customer payment policies and tightening credit terms when necessary can help reduce delayed payments. At the same time, regularly monitoring expenses ensures that costs remain aligned with revenue and prevents unnecessary spending from eroding available cash.

Build a Cash Reserve

Building a financial buffer is another important step in preventing future cash flow issues. Maintaining a reserve of available cash allows businesses to absorb unexpected expenses or temporary revenue slowdowns. Even a modest reserve can provide stability and give business owners the flexibility to manage challenges without disrupting operations.

Turning Cash Flow Challenges Into Opportunities for Growth

Cash flow problems can feel overwhelming, but they are also a common part of running a business. Many companies experience periods of financial pressure as they grow, adapt to market conditions, or adjust their operations.

Businesses that take a proactive approach to managing cash flow often emerge stronger. By improving invoicing processes, controlling expenses, and forecasting future financial needs, business owners can build a more resilient financial foundation.

Merchant Growth supports Canadian small businesses by providing flexible financing solutions designed to help stabilize cash flow and support ongoing growth. Whether a business needs working capital to manage short-term expenses or funding to pursue new opportunities, access to the right financial tools can make a meaningful difference.

CEBA Loan: Repayment, Forgiveness, and What It Means for Businesses Now

The CEBA loan helped hundreds of thousands of Canadian small businesses get through one of the most challenging periods in recent history. In total, 898,271 businesses were approved for CEBA loans, with 571,851 also receiving expansions, representing $49.2 billion in approved funding. For many owners, this support covered payroll, rent, and essential operating costs when revenue slowed or stopped altogether. It was designed as short-term relief, but for many businesses, it has become a longer-term financial commitment that still sits on the balance sheet today.

Now, the conversation around CEBA has shifted. Instead of emergency funding, it is about repayment, planning, and how this loan fits into the overall health of a business. Owners are thinking about cash flow, future growth, and how to manage obligations without creating unnecessary strain.

This article walks through how CEBA loans work today, what changed after the forgiveness period ended, what the repayment timeline means, and how businesses can approach this in a calm and practical way.

Key Takeaways

- CEBA loans that were not repaid by early 2024 are now term loans due at the end of 2026

- Partial loan forgiveness was available for businesses that met earlier repayment deadlines

- Interest applies during the remaining loan term

- If unpaid, CEBA loans may eventually be transferred to CRA collections

- Planning early creates more flexibility than waiting until the final repayment period

What Is a CEBA Loan?

The CEBA loan, short for the Canada Emergency Business Account, was a federal pandemic relief program that provided interest-free loans to small businesses through their financial institutions. Its purpose was simple: help businesses cover essential expenses and continue operating during the severe disruptions caused by COVID-19.

Businesses could initially access $40,000, with many later eligible for an additional $20,000, bringing the total possible loan to $60,000. These funds were backed by the Government of Canada and delivered through banks and credit unions, which made the program widely accessible at a critical time.

Today, CEBA is no longer about accessing support. For many businesses, it is now an existing loan balance that needs to be managed as part of regular financial planning. That shift from emergency relief to long-term obligation is why many owners are revisiting their CEBA loan and thinking about how they fit into their overall cash flow and future goals.

How CEBA Loan Forgiveness Worked and What Changed After the Deadlines

CEBA included a partial loan forgiveness feature designed to reward businesses that could repay most of their loan within a set timeframe. Businesses that received the original $40,000 loan could have up to $10,000 forgiven, while those that accessed the expanded $60,000 loan could qualify for up to $20,000 in forgiveness. In practical terms, this meant a portion of the loan could turn into a non-repayable grant if the remaining balance was paid back on time.

The key deadlines for forgiveness were tied to early 2024. The original deadline to repay and retain forgiveness was January 18, 2024. Businesses that had arranged refinancing and formally applied by that date were given a short extension, with a final forgiveness deadline of March 18, 2024. Once those dates passed, the forgiveness opportunity closed.

Another important shift happened at the same time. Starting January 19, 2024, any outstanding CEBA loan balance began accruing interest at 5% per year. Loans that were not repaid by the forgiveness deadline automatically transitioned into term loans, which changed how they function from that point forward.

For businesses, this marked a turning point. CEBA was no longer an interest-free emergency support program with a grant component. It became a standard business liability that carries interest, affects cash flow planning, and needs to be managed like other debt. The cost of holding the balance now grows over time, which is why many owners are reassessing how CEBA fits into their financial strategy.

CEBA Loan Repayment Timeline and What Applies Now

At this point, CEBA is less about the program itself and more about how it fits into the everyday financial rhythm of your business. It is one of several commitments that need to be balanced alongside payroll, suppliers, rent, and growth plans. The focus now is not on what the loan was, but on how to manage it in a way that supports stability rather than strain.

The final CEBA loan repayment date is December 31, 2026. While there is still time, the balance is not standing still. Interest continues to accrue, which means the longer the loan remains outstanding, the more it affects overall repayment cost and cash-flow planning.

For many business owners, the shift is mental as much as financial. CEBA is no longer about eligibility or forgiveness rules. It is about timing, cash flow, and strategy. Owners are looking at how repayment aligns with seasonal revenue, hiring plans, expansion goals, or other financial priorities over the next year.

CEBA Loan Repayment Terms and What Applies Now

For businesses that did not repay their CEBA loan by the applicable forgiveness deadline, the loan has now converted into a three-year term loan ending December 31, 2026. The repayment structure is standardized under the federal program and does not vary meaningfully by financial institution.

Under the current terms, interest accrues at 5% on the full outstanding balance of the loan, including any amount that was previously forgivable. Businesses are required to make monthly interest payments during the term. The full principal balance does not need to be repaid until the maturity date of December 31, 2026.

As it stands now, businesses with a converted CEBA term loan must budget for ongoing monthly interest payments while preparing to repay the full principal by the end of 2026. While borrowers may choose to repay principal early, the minimum required payments during the term are the monthly interest charges. Understanding this structure is key to planning cash flow and avoiding surprises at maturity.

Are CEBA Loans Personally Guaranteed?

In most cases, CEBA loans were not personally guaranteed in the traditional sense. A personal guarantee usually means that if the business cannot repay a loan, the owner becomes personally responsible, and their personal assets could be used to cover the debt. CEBA was structured differently. It was a government-backed business loan delivered through financial institutions, and most borrowers were not required to sign a standard personal guarantee.

However, this does not mean the obligation disappears if the loan is not repaid. The CEBA balance remains a legal responsibility of the business itself. If payments are missed and the account becomes delinquent, the file may move into collections. This can affect the business’s credit profile, make it more difficult to secure future financing, and create additional operational stress as recovery efforts begin.

If the loan progresses to CRA collections, the agency may use its standard recovery processes, which can include contacting the business to arrange payment and taking formal steps to recover the balance. While these situations are manageable, they are much easier to address when business owners stay aware of their loan status and plan ahead rather than reacting once the account has escalated.

What Happens to a CEBA Loan If a Business Closes in Canada?

Closing a business does not automatically erase a CEBA loan balance. Even if operations stop, the loan remains an outstanding obligation that still needs to be addressed. Many business owners assume that shutting down the company ends all financial responsibilities, but government-backed loans like CEBA continue to exist beyond the day-to-day life of the business.

If the balance is not repaid or arrangements are not made, the loan may move into collections. Over time, unresolved accounts can be transferred for recovery, and in some cases may be handled through CRA collections processes. This can add stress at a time when owners are already dealing with the challenges of closing a business, which is why understanding the situation early is helpful.

The most important step for businesses facing closure or financial difficulty is communication. Speaking with the lender or seeking professional advice early can create more options and reduce uncertainty. Even when a business is winding down, having a clear picture of outstanding obligations allows owners to make informed decisions rather than reacting under pressure later.

CEBA Loan Collections: What Happens if It Goes to CRA

When a CEBA loan reaches the collections stage, the experience changes from routine loan management to a more formal recovery process. Communication typically becomes more structured, timelines may feel less flexible, and the focus shifts to resolving the outstanding balance rather than ongoing account management.

For a business, this can create practical challenges. Collections activity can affect access to future financing, influence credit relationships, and add administrative pressure at a time when attention is needed elsewhere in the business. Even when a resolution is possible, handling the situation later in the process usually involves fewer options than addressing it earlier.

The takeaway here is about positioning, not urgency. Businesses that understand their repayment timeline and consider their options before reaching this stage tend to have more control over how the loan is handled. Planning ahead helps keep CEBA as a financial decision rather than a reactive situation.

Why Your CEBA Loan Is Now a Planning Decision, Not Just a Deadline

The CEBA loan is no longer a short-term crisis tool tied to the pandemic. For many businesses, it now sits alongside other financial commitments and needs to be viewed in the context of overall business planning. That means looking at it the same way you would evaluate equipment financing, operating expenses, or other forms of debt that affect cash flow over time.

Instead of focusing only on the repayment date, business owners can look at how CEBA fits into the bigger picture.

- Will repaying the loan in one lump sum create pressure on working capital?

- Does the timing of repayment overlap with hiring plans, inventory purchases, or expansion goals?

- Could adjusting how the loan is handled provide more stability while the business continues to grow?

Thinking about CEBA in this way changes the conversation. It moves from a deadline-driven mindset to a strategy-focused one. When the loan is considered as part of broader financial planning, it becomes something that can be managed deliberately rather than something that feels like it is hanging in the background.

Exploring CEBA Loan Refinancing as a Cash Flow Strategy

When CEBA first launched, refinancing was often discussed as a way to access forgiveness. Today, the conversation looks different. For many businesses, refinancing is less about deadlines and more about managing how the loan fits into ongoing operations and financial stability.

Refinancing can mean replacing the CEBA balance with another form of financing that better matches how the business earns and spends money. Instead of facing a single large repayment or carrying a growing interest balance, some owners look for a structure that spreads payments out in a more predictable way. This can make cash flow easier to manage, especially for businesses with seasonal revenue or uneven income cycles.

Another reason refinancing comes up is operating flexibility. Carrying a CEBA balance while also managing inventory, payroll, or expansion costs can tighten working capital. Adjusting how that debt is structured may allow a business to keep more liquidity available for day-to-day operations rather than tying up cash in one obligation.

For businesses concerned about future collections pressure, refinancing can also create a clearer repayment path. Moving the balance into a structured financing solution can reduce uncertainty and help owners stay in control of the timeline rather than reacting later.

This does not mean refinancing is the right step for every business. Costs, timing, and overall financial health all matter. The value is in understanding the option early, comparing it with other strategies, and choosing the path that best supports stability and growth. Having the conversation sooner simply gives businesses more room to make thoughtful decisions instead of rushed ones.

What Businesses Can Do Now Without Rushing

Even though there is still time in the CEBA repayment period, taking a few simple steps now can make the path ahead feel much more manageable. The goal is not to make immediate decisions, but to understand where things stand so there are no surprises later. When you have clarity, you gain flexibility and can approach repayment from a position of control rather than pressure.

Some practical starting points include:

- Review your current CEBA loan balance so you know exactly what remains outstanding

- Confirm your repayment structure and timeline with your financial institution

- Forecast your cash flow over the coming months to see how repayment fits alongside payroll, inventory, and other expenses

- Consider how repayment timing aligns with business plans, such as hiring, expansion, or equipment purchases

- Speak with an accountant or financial advisor to understand the impact on your overall financial picture

- Start exploring options early, even if you are not ready to act yet

These steps are about awareness, not urgency. Businesses that take the time to understand their position tend to feel more confident and have more options available. A little preparation now can turn CEBA from an open question into a manageable part of your financial plan.

From CEBA Uncertainty to Clarity

There is still time in the CEBA repayment period, and time is most valuable when it is paired with a plan. For many businesses, the challenge is not understanding that the loan needs to be repaid. It is figuring out how that repayment fits alongside everyday operating needs, future investments, and overall cash-flow stability.

Merchant Growth works with Canadian small businesses by providing flexible term financing designed to support real-world cash-flow needs. Funding can be delivered in as little as 6 hours, giving businesses fast access to working capital when timing matters. Whether the conversation is about understanding how CEBA affects working capital, exploring ways to manage repayment more smoothly, or simply reviewing financing options to avoid strain, the focus is on helping owners make informed, confident decisions based on their specific situation.

If you have questions about your CEBA loan or want to see what your options could look like, connecting with Merchant Growth can be a helpful starting point. A conversation does not mean committing to a solution. It means gaining clarity, understanding what is available, and choosing a path that supports your business’s stability and growth.

A Practical Guide to Working Capital for Small Businesses

Many small businesses are profitable on paper but still feel constant pressure on their cash. Sales are happening, customers are happy, and growth looks promising, yet there never seems to be enough money available at the right time. Bills arrive on fixed dates, payroll cannot wait, and suppliers expect payment whether customers have paid you or not. This disconnect between profit and available cash is one of the most common financial stress points for business owners.

That is where working capital comes in. Working capital explains how well your business can handle short-term financial demands using the resources it already has. It directly affects everyday decisions, from hiring and inventory purchases to marketing spend and tax payments. When working capital is healthy, operations feel steady and predictable, and decisions feel proactive instead of reactive.

This guide breaks down what working capital means in simple terms, how to calculate it, and how to use it as a decision-making tool. You will also learn how the working capital formula, ratio, and management strategies connect to real-world business stability and growth. By the end, working capital will feel less like an accounting term and more like a practical lens for running a stronger business.

Key Takeaways

- Working capital measures a business’s ability to cover short-term obligations

- It is calculated by subtracting current liabilities from current assets

- Positive working capital supports stability, while negative working capital increases risk

- The working capital ratio helps assess short-term financial health

- Strong working capital management improves resilience and growth readiness

What Is Working Capital?

Working capital is the money your business has available to run its day-to-day operations in the short term. It reflects whether you can cover upcoming expenses such as payroll, rent, supplier payments, and taxes using resources already within the business. In practical terms, working capital is the financial breathing room that keeps operations moving between money coming in and money going out. Without it, even routine payments can start to feel stressful.

Working capital is calculated as the difference between short-term assets and short-term liabilities. These are known as current assets and current liabilities, and together they show your company’s liquidity position. Unlike profit, which measures performance over time, working capital measures readiness right now. A business can be profitable overall and still struggle if working capital is tight.

What Is Net Working Capital?

Net working capital emphasizes the “net” difference between your totals of current assets and current liabilities. While the term is often used interchangeably with working capital, it highlights that we are looking at the balance between two moving parts. This balance shows how much flexibility the business truly has after accounting for short-term obligations. It gives a clearer picture than looking at cash alone.

Lenders, investors, and financial partners often review net working capital to assess short-term financial stability. For business owners, this number becomes especially important during growth periods, large purchases, or seasonal swings. These situations can increase demands on cash even when revenue is strong. Monitoring net working capital helps prevent surprises when timing gaps appear.

Understanding the Working Capital Formula

Before jumping into the math, it helps to understand what the formula is really measuring. The working capital formula compares what your business can turn into cash in the near term with what it must pay in the near term. This comparison shows whether your operations are supported by enough liquidity to run smoothly. It turns day-to-day financial movement into a clear snapshot.

Working Capital = Current Assets − Current Liabilities

Current assets are resources your business expects to use or convert into cash within a year. Current liabilities are financial obligations due within that same period. These two groups represent the inflows and outflows shaping your short-term financial health.

Current assets typically include:

- Cash in bank accounts

- Accounts receivable from customers

- Inventory that can be sold

- Short-term investments

- Prepaid expenses

Current liabilities typically include:

- Accounts payable to suppliers

- Short-term loans or lines of credit

- Payroll owed

- Taxes payable

- Accrued expenses such as rent or utilities

When these components are viewed together, the equation becomes a story about timing, not just totals. It shows whether the business has enough short-term support to stay steady, even when payments do not line up perfectly.

How Do You Calculate Working Capital?

Understanding the formula is one thing, but applying it to your own business is where the insight really comes from. Calculating working capital is not just an accounting exercise. It is a practical way to see how your daily operations are supported and whether your business has enough short-term resources to handle its obligations comfortably.

When you go through the calculation step by step, you start to see patterns. You notice how receivables rise and fall, how inventory levels change, and how upcoming payments affect your cash position. This process helps turn abstract financial statements into useful information that supports real decisions.

Step 1: Identify Your Current Assets

Begin by listing everything your business owns that can reasonably be converted into cash within the next year. This includes money in the bank, invoices customers are expected to pay soon, and inventory ready for sale. These assets represent the financial fuel that keeps your business moving and often fluctuate throughout the month. Tracking them regularly gives you a clearer picture of available resources.

Step 2: Identify Your Current Liabilities

Next, list the bills and obligations your business must pay within that same timeframe. Supplier invoices, loan payments, payroll, and taxes all fall into this category. These liabilities often arrive on fixed schedules, which can create pressure when customer payments are delayed. Understanding these commitments helps you anticipate when cash will be needed most.

Step 3: Subtract Liabilities from Assets

Once both totals are clear, subtract current liabilities from current assets. This working capital calculation shows the net amount of short-term resources your business has left after covering near-term obligations. It reveals whether you are operating with a comfortable cushion or a narrow margin.

Step 4: Interpret the Result

A positive result means you have breathing room to manage daily operations and unexpected costs. A negative result means short-term debts exceed short-term assets, which can signal liquidity strain. This step is about connecting the number to real decisions, such as whether to delay an expense or seek additional funding.

For example, if your business has $100,000 in current assets and $70,000 in current liabilities, your working capital is $30,000. That $30,000 acts as a buffer for timing gaps and normal cash flow fluctuations. It provides stability and reduces the likelihood of financial stress from routine operations.

What Is the Working Capital Ratio?

The working capital ratio, also known as the current ratio, shows the relationship between assets and liabilities rather than just their difference. It is calculated by dividing current assets by current liabilities. This ratio provides insight into how comfortably a business can cover short-term obligations. It adds context that a dollar figure alone may not show.

A ratio above 1 suggests assets exceed liabilities, which is generally positive. A ratio that is too low signals potential liquidity risk, while an extremely high ratio may mean resources are not being used efficiently. Many small businesses aim for a ratio between about 1.2 and 2, although the right level depends on industry and cash flow patterns. The goal is balance, not extremes.

Examples of Working Capital in Real Businesses

Working capital becomes much easier to understand when you see how it shows up in everyday business situations. While the formula is the same for every company, the pressures and timing challenges look very different depending on how a business earns revenue and pays its expenses. In practice, working capital is less about spreadsheets and more about how smoothly money moves through your operations.

Retail Business

Retail businesses often have a large portion of their cash tied up in inventory sitting on shelves or in storage. They usually need to pay suppliers for goods before those items are sold, which means cash leaves the business well before it returns. If products move quickly, working capital stays healthy. But if demand slows, trends change, or inventory is overstocked, cash can become trapped in unsold goods.

Retailers must constantly balance how much inventory to carry. Too little stock can mean missed sales opportunities, while too much can create liquidity pressure. Promotions, seasonal planning, supplier negotiations, and careful purchasing decisions all directly influence working capital. Even small changes in inventory turnover can have a noticeable effect on how much cash is available to run the business.

Service Business

Service businesses usually have fewer physical assets but face a different working capital challenge: timing of payments. Employees, contractors, and operating expenses must be paid regularly, yet clients often pay invoices on 30-, 60-, or even 90-day terms. This delay means the business may deliver services long before receiving payment.

Strong invoicing practices, clear payment terms, and consistent follow-ups are critical. When receivables are collected quickly, working capital improves. When clients pay late, the business may need to rely on savings or financing just to cover routine expenses. For service businesses, managing receivables is often the single biggest factor in maintaining healthy working capital.

Seasonal Business

Seasonal businesses experience dramatic swings in revenue throughout the year. Tourism operators, landscaping companies, and certain retailers may earn most of their income in just a few months. During peak season, cash inflows can be strong, but expenses such as rent, insurance, and equipment payments continue year-round.

Working capital built during busy months must stretch across the off-season. Without careful planning, a profitable year can still end in cash shortages during slower periods. Budgeting, setting aside reserves, and forecasting ahead help smooth these cycles and prevent short-term strain.

Across all these examples, working capital acts as a bridge between when money goes out and when it comes back in. The stronger that bridge, the easier it is for a business to stay steady through normal ups and downs.

Why Working Capital Is Important for Small Businesses

Working capital might sound like an accounting concept, but for small business owners, it is a daily reality. It influences how confidently you make decisions and how much financial stress you experience. When working capital is strong, business feels manageable and predictable. When it is tight, even routine expenses can create pressure.

Healthy working capital gives you room to operate without constantly worrying about cash timing. It helps ensure that short-term financial needs do not distract from long-term strategy. Instead of reacting to cash shortages, owners can focus on growth, customer relationships, and improving operations.

Covering Routine Expenses

Every business has fixed and recurring costs that do not wait, including payroll, rent, utilities, insurance, and supplier invoices. These expenses often come due before customer payments arrive. Strong working capital ensures these obligations can be met on time without scrambling or delaying critical payments.

Consistently covering routine expenses also supports employee morale and supplier relationships. When payments are predictable, trust grows, and operations run more smoothly. This stability reduces stress and allows owners to concentrate on running the business rather than managing financial emergencies.

Stability During Slow Periods or Unexpected Events

No business operates in a perfectly predictable environment. Sales cycles fluctuate, customers pay late, and unexpected repairs or expenses arise. Strong working capital acts as a financial cushion during these moments, giving the business time to adjust without panic.

This cushion reduces the need for emergency borrowing, which often comes with higher costs and pressure. Instead, the business can make thoughtful adjustments and continue operating without major disruption. Stability during slower periods is one of the biggest benefits of healthy working capital.

Credibility With Lenders and Suppliers

Financial stability builds trust with the partners your business depends on. Suppliers are more willing to offer favorable payment terms when a business pays consistently. Lenders view strong working capital as evidence that the business can manage short-term obligations responsibly.

This credibility can lead to better financing options, stronger partnerships, and more flexibility during busy or challenging periods. Over time, these relationships can significantly improve operational efficiency and financial resilience.

Better Planning and Growth Decisions

Working capital provides a clearer view of what the business can afford. It helps owners plan for hiring, marketing investments, equipment purchases, and tax obligations with confidence. Instead of guessing or reacting, decisions can be based on a realistic understanding of available resources.

When working capital is healthy, growth becomes more sustainable. The business can expand at a pace that matches its financial capacity, reducing the risk of overextending. This balance supports long-term success rather than short-term gains followed by financial strain.

When working capital is strong, the business operates from a position of control rather than survival mode. That foundation makes it much easier to manage cash flow actively over time, which is where working capital management comes into play.

What Is Working Capital Management?

Understanding working capital is an important first step, but keeping it healthy requires ongoing attention. That is where working capital management comes in. Working capital management is the day-to-day process of monitoring and adjusting how money moves through your business. It focuses on timing, balance, and making sure short-term resources line up with short-term obligations.

This is not a one-time calculation you do at tax season. It is an active approach to running your business. Sales, expenses, inventory levels, and customer payment habits are always changing, which means working capital is always moving too. Managing it well helps prevent cash shortages before they happen and creates more control over financial stability.

Some of the most effective working capital management strategies include improving how quickly money comes in and being thoughtful about how and when money goes out.

- Faster invoicing and collections help shorten the gap between delivering a product or service and receiving payment. Clear payment terms, automated reminders, and consistent follow-ups can make a significant difference. Even reducing average payment time by a few days can improve working capital noticeably.

- Smarter inventory management ensures cash is not unnecessarily tied up in stock that moves slowly. Regularly reviewing inventory levels, forecasting demand, and adjusting purchasing patterns helps keep resources available for other needs.

- Negotiating supplier payment terms can create more flexibility. When payment timelines better match your sales cycle, working capital becomes easier to manage. Strong relationships and consistent payment history often make these conversations more productive.

Working capital management connects financial awareness with operational decisions. It turns financial data into practical actions that support stability and growth. Over time, these small improvements add up and make the business more resilient to change.

Common Misunderstandings About Working Capital